So, you’ve just bought a fantastic used car, or maybe you’re thinking about it. That’s awesome! There’s a thrill in finding a great deal, a pre-loved gem that fits your budget and your lifestyle. But then, a little voice in the back of your head (or maybe a loud one from your significant other) pipes up: “What about the insurance?”

And let’s be honest, trying to figure out car insurance for used cars USA can feel like decoding ancient hieroglyphs. It’s not always as straightforward as insuring a brand-new vehicle, and a lot of folks stumble at this stage. You might think, “It’s an older car, so it must be cheaper to insure, right?” Well, not always. The truth is, there are nuances, hidden costs, and clever ways to save that most people miss. My goal here? To be your knowledgeable friend, sitting across from you with a coffee, breaking down exactly how to navigate this process, step-by-step, so you can drive off with peace of mind and a policy that actually makes sense for your ride.

Why Insuring a Used Car Isn’t Always What You Think

Here’s the thing about used car insurance : it’s a different beast. Many assume that because a car is older, its value is lower, and therefore, its insurance premium will automatically be rock bottom. While that’s often true for collision and comprehensive coverage (which pay out based on the car’s actual cash value), it’s not the whole story. Factors like the car’s safety rating, how expensive it is to repair, its theft rate, and even its engine size can significantly impact your rates, regardless of age.

I’ve seen people make the mistake of assuming a vintage beauty will be cheap to insure, only to be shocked by high premiums due to specialized parts or a higher theft risk for classic models. The insurance industry isn’t just looking at the purchase price; they’re assessing risk from every angle. This is where understanding thefactors affecting used car insurancebecomes crucial. It’s not just about the vehicle itself, but also your driving history, where you live, and even your credit score in many states. It’s a complex algorithm, but knowing the inputs gives you an advantage.

Your Step-by-Step Guide to Smart Used Car Insurance

Ready to get this sorted? Excellent. Let’s walk through exactly how to insure a used car without losing your mind. This isn’t just about getting a quote; it’s about getting the right quote for your car and your needs.

Step 1 | Know Your Car (Beyond the Make and Model)

Before you even think about quotes, dig into the details. What are the specific safety features? Does it have advanced driver-assistance systems (ADAS)? What’s its VIN (Vehicle Identification Number)? The more information you have, the more accurate your quotes will be. Also, consider the car’s reliability ratings. A car known for frequent breakdowns might not directly impact premiums, but it certainly affects your overall cost of ownership, including the likelihood of needing to use your coverage.

Step 2 | Understand Your Coverage Needs

This is probably the most overlooked step. Don’t just click “full coverage” or “minimum liability.” Think about your financial situation. If your used car is older and paid off, do you really need comprehensive and collision? We’ll dive deeper intolow cost term insurance plansconcepts here, but essentially, assess the car’s actual cash value against the cost of the premiums for higher coverage. Sometimes, it makes more financial sense to self-insure for minor damages on an older vehicle.

Step 3 | Gather Multiple Online Car Insurance Quotes

This is where the real work (and potential savings) happens. Don’t settle for the first quote you get. Use online comparison tools or contact several different providers directly. I always recommend getting at least three to five quotes. Why? Because every insurer has a different appetite for risk, and their pricing models vary wildly. What one company considers high risk, another might view as moderate. When you’re looking for auto insurance for used cars , especially in the USA, variety is your friend. Make sure you’re comparing apples to apples – the exact same coverage limits and deductibles.

Step 4 | Be Honest and Thorough with Your Information

It sounds obvious, but I’ve seen people try to fudge details to get a lower quote. Don’t do it. Any discrepancy found later could lead to your policy being voided or a claim denied. Be precise about mileage, garaging address, and any modifications to the vehicle. Transparency builds trust, and trust is what you want with your insurer.

Decoding Coverage | Liability vs. Full for Your Ride

This is where many drivers get confused, especially when it comes to insuring a used car . Let’s break down the core types of coverage you’ll encounter:

- Liability Coverage: This is the bare minimum required by law in almost every U.S. state. It covers damages and injuries you cause to other people and their property. It doesn’t cover your car or your injuries. For an older, lower-value used car, some people opt for just liability to keep costs down. But be warned: if you total your own car, you’re on the hook for repairs or replacement.

- Collision Coverage: This pays for damage to your own vehicle resulting from a collision with another car or object, regardless of who is at fault. If your used car still has significant value to you, or if you couldn’t easily afford to replace it out-of-pocket, this is a wise addition.

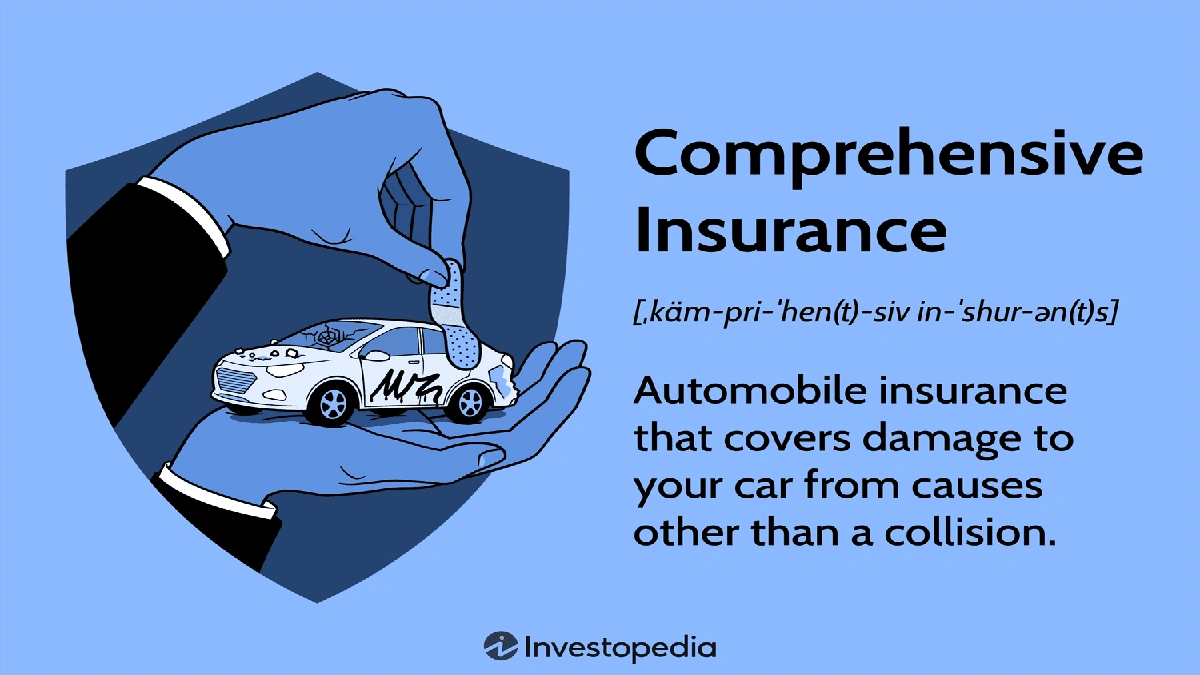

- Comprehensive Coverage: This covers damage to your car from non-collision events, like theft, vandalism, fire, natural disasters (hail, floods), or hitting an animal. For best insurance for older cars, especially if you live in an area prone to severe weather or have concerns about theft, comprehensive can be invaluable.

- Medical Payments/Personal Injury Protection (PIP): These cover medical expenses for you and your passengers after an accident, regardless of fault. State requirements vary, but it’s a smart consideration.

- Uninsured/Underinsured Motorist (UM/UIM): Sadly, not everyone on the road is adequately insured. This coverage protects you if you’re hit by someone who has no insurance or not enough to cover your damages. I consider this almost non-negotiable, especially given the number of uninsured drivers out there.

When deciding betweenliability vs full coverage used car, ask yourself: What’s the actual cash value (ACV) of my car? How much would it cost to repair or replace it? Can I comfortably cover that cost out of pocket? If the answers lean towards “no,” then opting for more comprehensive coverage might be worth the extra premium. It’s about balancing risk and affordability.

Finding the Sweet Spot | Cost-Saving Tips & Tricks

Nobody wants to overpay, right? When it comes to finding cheap used car insurance , there are genuine strategies that can make a difference. It’s not about cutting corners on necessary coverage, but about being smart with your choices.

- Increase Your Deductible: This is a classic for a reason. A higher deductible (the amount you pay out-of-pocket before insurance kicks in) almost always lowers your premium. Just make sure you can comfortably afford your chosen deductible if you need to make a claim.

- Bundle Your Policies: Do you have home insurance, renters insurance, or even life insurance? Many companies offer significant discounts if you bundle multiple policies with them. It’s a simple way to shave off some dollars, and it often simplifies your financial management. Think about how a home insurance premium calculator might show you savings by bundling!

- Ask About Discounts: Seriously, ask! Insurers have a plethora of discounts: good student, multi-car, safe driver, anti-theft devices, low mileage, professional affiliations, payment in full, paperless billing… the list goes on. Don’t assume they’ll offer them; you often have to inquire.

- Improve Your Driving Record: This is a long-term strategy, but it’s the most impactful. A clean driving record with no accidents or tickets is gold to insurers.

- Review Your Policy Annually: Your life changes, and so do insurance rates. What was the best deal last year might not be this year. Shop around periodically, especially at renewal time, to ensure you’re still getting competitive rates for your buying used car insurance needs.

- Consider Usage-Based Insurance: Some insurers offer programs where a device in your car (or an app on your phone) monitors your driving habits. If you’re a safe driver, this can lead to substantial discounts.

FAQs | Your Burning Questions Answered

What if I just bought the used car and don’t have insurance yet?

Most states require proof of insurance before you can legally drive a vehicle off the lot or register it. If you already have an existing policy, many insurers offer a grace period (often 7-30 days) to add a new vehicle, but it’s always best to contact your provider before you drive the car home to ensure continuous coverage. Don’t risk driving uninsured!

Does the age of the used car affect insurance costs significantly?

Yes, but it’s not always a simple inverse relationship. Older cars generally have lower actual cash values, which can reduce the cost of collision and comprehensive coverage. However, if an older car is a classic, a high-performance model, or has expensive-to-repair parts, its premiums could still be high. It’s all about the specific risk factors an insurer assesses.

Can I get temporary car insurance for a used car purchase?

While some providers offer short-term policies, they are less common in the U.S. for standard purchases. It’s more typical to add the new used car to an existing policy or secure a new annual policy immediately. Always check with your current insurer first; they might cover it automatically for a short period.

Is full coverage worth it for an older used car?

This depends entirely on your financial situation and the car’s value. If the cost of comprehensive and collision coverage over a year or two approaches or exceeds the car’s actual cash value, it might not be worth it. However, if you couldn’t afford to replace the car if it were totaled, even if it’s older, then full coverage provides essential financial protection. It’s a personal risk assessment.

Will modifying my used car affect my insurance rates?

Absolutely. Performance modifications (engine tuning, exhaust systems) or aesthetic changes (custom paint, body kits) can increase your premiums because they can increase the car’s value, its risk of theft, or the cost of repairs. Always inform your insurer about modifications; otherwise, a claim might be denied or underpaid.

How does mileage affect car insurance for used cars USA?

Lower annual mileage can often lead to lower premiums. Insurers view less time on the road as less risk of an accident. If you drive your used car sparingly, ask your insurer about low-mileage discounts or consider usage-based insurance programs.

Ultimately, getting the right used vehicle insurance for your pre-loved ride in the USA isn’t about finding the absolute cheapest option, but the smartest one. It’s about understanding the unique considerations of used cars, knowing your own financial comfort level, and diligently comparing your options. With this guide, you’re not just getting insurance; you’re making an informed decision that protects your investment and gives you confidence on the road. So go on, enjoy that used car – you’ve earned the peace of mind that comes with smart coverage!