Alright, let’s be honest for a moment. If you’re searching for ” best auto insurance for high risk drivers USA ,” you’re probably feeling a mix of frustration and anxiety. Maybe you’ve had a few too many tickets, an accident that wasn’t your finest moment, or perhaps even a DUI. Whatever the reason, you’re now in that unenviable category that makes insurers see dollar signs but not in your favor. And let me tell you, it’s not a fun club to be in. But here’s the thing: being a high-risk driver doesn’t mean you’re uninsurable. It just means you need a different strategy, a smarter approach. Think of me as your guide, sitting down with you over a cup of coffee, ready to demystify this whole process and show you exactly how to find the coverage you need without emptying your wallet. Because yes, even with a challenging driving record , affordable auto insurance is possible.

Understanding “High-Risk” | Why Are You in This Category?

First, let’s peel back the layers a bit. What exactly makes an insurer label someone “high-risk”? It’s not just a random judgment; it’s based on cold, hard data and actuarial tables. Typically, this label gets slapped on you for a few key reasons. Excessive speeding tickets, at-fault accidents, a lapse in coverage, or serious violations like DUIs or reckless driving are common culprits. Each of these flags you as a higher probability of filing a claim, which, from an insurer’s perspective, means more risk for them. This directly impacts your insurance premiums . What fascinates me is how these factors affecting car insurance rates aren’t just about your past, but about predicting your future behavior behind the wheel. It’s a tough pill to swallow, I know, but understanding the “why” is the first step in figuring out “how” to improve your situation. So, if you’re stuck with what feels like bad driving record insurance, know that there are pathways forward.

Navigating the Non-Standard Market | Where to Look First

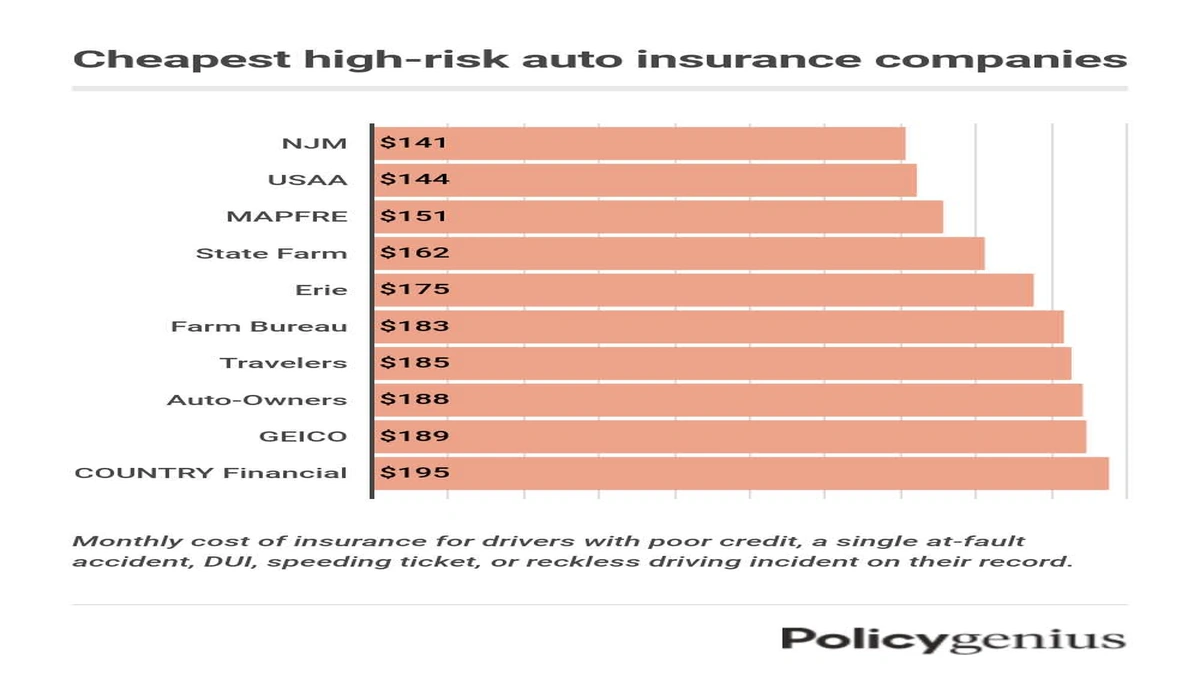

Now, for the practical stuff. The traditional, big-name insurers often shy away from high-risk drivers, or they’ll quote you rates that make your eyes water. This is where the “non-standard” market comes into play. Think of it as a specialized niche, specifically designed for people like us who don’t fit the perfect, low-risk mold. These aren’t shady operations; they’re legitimate companies that have built their business model around insuring drivers with challenging histories. Companies like Progressive, GEICO, and State Farm might have non-standard divisions, or you might find smaller, dedicated high-risk auto insurance companies like National General, Dairyland, or Bristol West. The key here is to not get discouraged by rejections from mainstream providers. These non-standard auto insurance providers understand your situation and are often your best bet for getting covered. It’s all about knowing where to cast your net, right? Don’t just settle for the first quote; you need to compare quotes diligently.

For a deeper dive into how non-standard insurance operates and what to expect, you might find this resource onnon-standard auto insurancehelpful. It explains the mechanics behind these policies, which is crucial for making informed decisions.

The SR-22 Conundrum | What You Need to Know (If Applicable)

If you’ve had a serious violation, like a DUI or reckless driving, you might have heard the term “SR-22.” And if you haven’t, prepare yourself, because it’s a big one. An SR-22 isn’t an insurance policy itself; it’s a certificate of financial responsibility that your insurance company files with your state’s Department of Motor Vehicles (DMV). It’s essentially proof that you have the minimum required car insurance coverage. Without it, you often can’t reinstate your driving privileges. Getting SR-22 insurance can feel like another hurdle, but many high-risk auto insurance companies specialize in filing these for you. It’s a non-negotiable step for many, and navigating the process correctly is vital. Don’t try to cut corners here; it will only lead to bigger headaches down the road. If you need DUI insurance , an SR-22 will almost certainly be part of the package. It’s a temporary requirement, usually lasting 3-5 years, but during that time, it’s non-negotiable.

Strategies to Lower Your Premiums (Even When High-Risk)

Okay, so you’re covered, but the premiums are still making you wince. I get it. The good news is, there are proactive steps you can take to chip away at those costs. This isn’t just about finding the best auto insurance for high risk drivers USA right now; it’s about setting yourself up for lower rates in the future.

1. Drive Safely (Obvious, but Critical)

This goes without saying, but a clean driving record for a period (usually 3-5 years) is your best friend. Every ticket-free, accident-free month brings you closer to shedding that “high-risk” label. It’s a marathon, not a sprint, but consistency pays off.

2. Increase Your Deductible

If you can afford to pay more out-of-pocket in the event of a claim, raising your deductible can significantly lower your monthly premiums. Just make sure it’s an amount you can comfortably cover without financial strain. It’s a classic trade-off, but one that can make a big difference in your immediate costs. Speaking of managing costs, understanding how different deductible levels impact your overall financial planning can be insightful, much like considering your options withlow deductible health insurance plans USA.

3. Look for Discounts

Even high-risk drivers can qualify for discounts! Ask about defensive driving course discounts, good student discounts (if applicable to a young driver on your policy), bundling discounts (homeowners/renters insurance), or even discounts for paying your premium in full. Telematics programs, where a device monitors your driving habits, can also offer significant savings if you prove you’re a safe driver. These are excellent ways on how to get cheaper car insurance after an accident.

4. Re-evaluate Your Coverage

Do you really need full coverage on an older car? Consider dropping collision and comprehensive if the car’s value doesn’t justify the cost. Minimum liability is often the cheapest option, but be aware of the financial risks if you’re at fault in a serious accident. It’s a balance, and one you should assess regularly.

5. Shop Around, Constantly

Don’t get complacent. Every 6-12 months, get new high risk auto insurance quotes. As time passes and your driving record improves, different insurers might offer you better rates. This is arguably the single most important strategy for how to get cheap car insurance with bad record.

Beyond the Basics | Insurers That Understand

When you’re a high-risk driver, it can feel like you’re speaking a different language than the standard insurance world. That’s why it’s crucial to find insurers who are fluent in “non-standard.” These companies often have more flexible underwriting guidelines and a deeper understanding of the nuances involved in insuring drivers with DUIs, multiple accidents, or lapses in coverage. They’re not just looking at your past mistakes; they’re often more willing to look at your present efforts to improve your driving habits.

While comparing options, remember that insurance isn’t a one-size-fits-all product. Just like exploring different facets of financial protection, such as ajoint life insurance UK comparisonmight involve understanding unique policy structures, finding the right car insurance for a challenging driving history requires a detailed look at various provider offerings. Always get multiple high risk auto insurance quotes to ensure you’re getting the best possible rate for your specific situation.

Frequently Asked Questions About High-Risk Auto Insurance

What exactly makes a driver “high-risk”?

Generally, a driver is considered high-risk if they have a history of multiple accidents, numerous traffic violations (like speeding tickets), a DUI/DWI conviction, a lapse in insurance coverage, or are a new, inexperienced driver, especially a young one.

Can I get car insurance with a DUI?

Yes, absolutely. While a DUI will significantly increase your premiums and often require an SR-22 filing, many non-standard auto insurance companies specialize in providing DUI insurance . It’s crucial to shop around and disclose your full driving history.

How long will I be considered a high-risk driver?

This varies by state and insurer, but typically, major violations like DUIs or reckless driving stay on your record for 3-5 years, sometimes longer. As these incidents age, your rates should gradually decrease, provided you maintain a clean driving record.

Is SR-22 insurance expensive?

The SR-22 itself is just a filing fee, usually quite small. However, the underlying insurance policy required for the SR-22 is often more expensive because it’s for a driver with a serious violation. The cost increase comes from your high-risk driver status, not the SR-22 form itself.

Should I compare quotes from different companies?

Yes, absolutely! This is perhaps the most important piece of advice for high-risk drivers. Different insurers assess risk differently, leading to potentially significant price variations. Always compare quotes from at least 3-5 companies, especially those specializing in non-standard auto insurance .

So, there you have it. Being labeled a high-risk driver isn’t the end of the road; it’s just a detour. With the right knowledge, a bit of persistence, and a willingness to explore the non-standard market, you absolutely can find the best auto insurance for high risk drivers USA that fits your needs and your budget. Remember, every day you drive safely is another step towards shedding that label and getting back to more standard rates. It’s a journey, but you’re not alone, and with these strategies, you’re well-equipped to navigate it. Stay safe out there!