Alright, let’s grab a virtual coffee and talk about something that trips up so many people when they’re trying to make smart financial decisions: the phrase ” term life insurance with cash value USA explained .” Sounds appealing, doesn’t it? Like you get the best of both worlds – temporary coverage with a savings component. But here’s the thing, and I’m going to be blunt: that phrase, as a standalone product, is largely a marketing myth. And understanding why it’s a myth is absolutely crucial for yourfinancial planningin the USA.

I’ve seen this confusion play out countless times. People come in, eyes glazed over with jargon, asking for a policy that simply doesn’t exist in the way they imagine. My goal here isn’t just to tell you what’s what, but to explain why this misconception is so pervasive, what the underlying truths are, and what your actual options look like. Because, let’s be honest, navigating the world of life insurance in the USA can feel like trying to solve a Rubik’s Cube blindfolded.

The Great Misconception | Term vs. Permanent Life Insurance

At its core, the confusion around “term life with cash value” stems from a fundamental misunderstanding of the two main types of life insurance: term and permanent. Think of them as two distinct paths, not a blended super-highway.

Pure Term Life Insurance | The Stopwatch of Protection

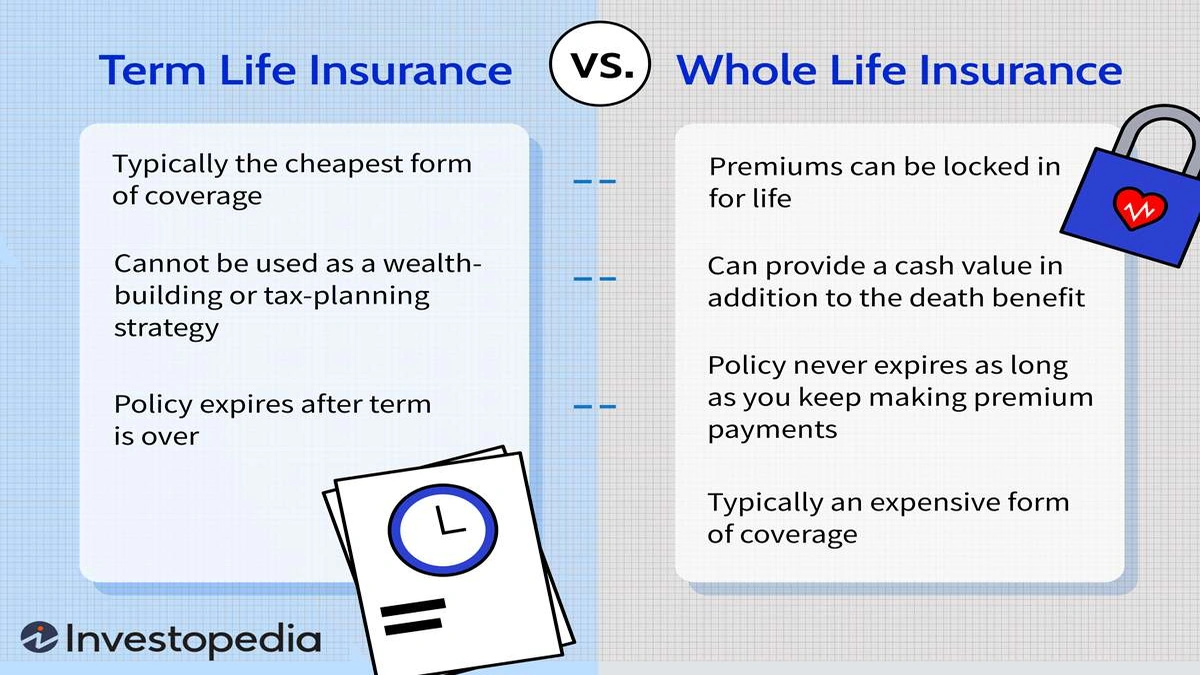

Term life insurance is straightforward. It’s like renting an apartment. You pay a premium for a specific period – say, 10, 20, or 30 years – and if you pass away during that term, your beneficiaries receive a tax-free death benefit . If the term ends and you’re still kicking, the coverage simply expires, and there’s no payout. Crucially, pure term life insurance has no cash value component. None. Zero. It’s pure protection, nothing more, nothing less. It’s typically the most affordable option because it doesn’t build any savings.

Permanent Life Insurance | The House You Own (with a Savings Account)

Then you have permanent life insurance . This is where the cash value enters the picture. Think of permanent life as owning a house. It lasts your entire life (as long as premiums are paid), and a portion of each premium goes into a separate account that grows over time – this is your cash value. This cash value grows on a tax-deferred basis and can be accessed during your lifetime through withdrawals or policy loans . The most common types of permanent life insurance are whole life insurance and universal life insurance .

So, why the confusion? It’s because some agents or articles might loosely refer to certain features of permanent policies in a way that sounds like term with cash value. Perhaps they’re talking about a term policy that can be converted into a permanent one (which then would build cash value), or they’re discussing a hybrid life insurance policies that combine elements, but isn’t a pure “term with cash value” product.

Deconstructing “Cash Value” | How It Actually Works (or Doesn’t)

Let’s really dig into what cash value means and why it’s tied to permanent policies, not term. When you hear about cash value growth , it’s generally referring to the internal savings component of a permanent policy.

The Mechanics of Cash Value Growth

With whole life insurance , the cash value grows at a guaranteed rate, making it predictable and stable. With universal life insurance , the growth is often tied to market indexes or a declared interest rate, offering more flexibility but also potentially more volatility. The key takeaway? This growth takes time, and it’s a feature of policies designed for lifelong coverage and long-term savings, not a temporary protection product.

Accessing Your Cash Value | Loans and Withdrawals

One of the appealing aspects of policies with cash value is the ability to access it while you’re alive. You can take out policy loans against your cash value. These loans don’t typically require credit checks and don’t affect your credit score, but they do accrue interest. If you die with an outstanding loan, the death benefit paid to your beneficiaries will be reduced by the loan amount plus any unpaid interest.

Alternatively, you can make withdrawals. However, withdrawals reduce both the cash value and the death benefit. If you decide you no longer want the policy, you can surrender it and receive the surrender value – which is your cash value minus any fees or charges. This is where the permanent nature becomes clear; it’s designed to be a long-term asset, not a short-term fix like a term policy.

For a deeper dive into how cash value works, especially itscash surrender value, financial resources like Investopedia offer excellent explanations. The point is, if a policy truly has cash value, it’s not a pure term policy.

The Real Reasons People Seek “Cash Value” in Life Insurance

So, if “term life with cash value” isn’t a thing, why do people keep asking for it? It usually comes down to a desire for more than just a death benefit. People are looking for:

- A Savings Component: They want their premiums to do more than just provide coverage; they want them to build wealth.

- Tax Advantages: The tax-deferred growth of cash value and the tax-free access via loans are very attractive.

- Flexibility: The idea of being able to tap into funds for emergencies or opportunities later in life.

- Legacy Planning: A way to leave a substantial, tax-free inheritance beyond just the death benefit itself.

These are all valid goals! The mistake isn’t in wanting these features, but in trying to force them into a product (term life) that isn’t designed for them. It’s like wanting a sports car to also be a heavy-duty pickup truck. You need to pick the right vehicle for the job.

Navigating Your Options | What Should You Consider?

Given that pure “term life with cash value” is a chimera, what are your actual, tangible options for protecting your loved ones and building wealth in the USA?

1. Pure Term Life Insurance | Protection First

If your primary goal is to provide a safety net for your family during your working years, when your financial obligations are highest (mortgage, raising kids, etc.), then term life insurance is likely your best bet. It offers maximum coverage for the lowest premium, allowing you to invest the difference in other vehicles. This is often part of the “buy term and invest the difference” strategy.

2. Permanent Life Insurance | Long-Term Security & Savings

If you’re looking for lifelong coverage, a guaranteed death benefit, and a savings component that grows tax-deferred, then a permanent policy might be for you. Decide between:

- Whole Life: Offers guaranteed premiums, guaranteed cash value growth, and guaranteed death benefit. It’s less flexible but very predictable.

- Universal Life: Offers more flexibility in premiums and death benefits, and cash value growth can be tied to market performance (like Indexed UL) or a declared interest rate (like Guaranteed UL).

These policies are often used for estate planning, business succession, or as a component of a diversified portfolio. They are more complex and generally more expensive than term policies, which is why understanding their true value proposition is key. You might also encounterhybrid life insurance policiesthat blend features, but they are still fundamentally permanent insurance products, not term.

3. Separate Your Insurance from Your Investments

For many, the most effective strategy is to buy pure term life insurance for protection and then invest separately in vehicles like 401(k)s, IRAs, mutual funds, or real estate. This allows you to maximize your investment returns without the fees and complexities often associated with the investment components of permanent life insurance. The tax implications life insurance can be favorable, but always consult a financial advisor to ensure your strategy aligns with your overall goals.

Frequently Asked Questions About Life Insurance Cash Value

Can term life insurance ever have cash value?

No, pure term life insurance does not have cash value . It’s designed solely for temporary death benefit protection. Any policy that builds cash value is, by definition, a form of permanent life insurance, or a hybrid product that is fundamentally permanent.

What’s the main difference between whole life insurance and universal life insurance?

Whole life insurance offers guaranteed premiums, guaranteed cash value growth, and a guaranteed death benefit, making it very predictable. Universal life insurance , on the other hand, offers more flexibility with premiums and death benefits, and its cash value growth can vary based on interest rates or market performance, depending on the specific type of UL policy.

Are policy loans a good idea?

Policy loans can be a valuable way to access funds without affecting your credit score, but they do accrue interest and reduce your death benefit if not repaid. They should be used strategically and with a clear repayment plan, not as a primary source of emergency funds without careful consideration.

What is the surrender value of a life insurance policy?

The surrender value is the amount of cash value you receive if you cancel (surrender) a permanent life insurance policy. It’s typically the cash value minus any surrender charges that apply, especially in the early years of the policy.

How do I choose the right life insurance in the USA?

Choosing the right policy depends on your specific needs, financial goals, and budget. Consider your dependents, debts, income replacement needs, and whether you want pure protection or a savings component. Consulting with a qualified financial advisor is highly recommended to assess your situation and explore suitable options for your financial planning .

So, there you have it. The idea of ” term life insurance with cash value USA explained ” is less about a specific product and more about understanding the distinct roles that different types of life insurance play. Don’t fall for marketing that blurs these lines. Instead, empower yourself with clear knowledge. Decide whether you need pure, temporary protection, or if you’re looking for lifelong coverage with a savings component, and then choose the right tool for your unique financial journey. Clarity, my friend, is your most valuable asset when it comes to insurance.