Alright, let’s be honest. That moment when your homeowners insurance policy renewal lands, and you see that mysterious number next to “deductible”? It often feels like you’ve just stumbled upon a secret code. You probably know it means you pay something if disaster strikes, but beyond that? It can get fuzzy, fast. And in the USA, with its diverse climate and property risks, understanding your home insurance deductible options isn’t just about jargon; it’s about safeguarding your biggest asset and making smart financial planning decisions.

I’ve seen countless homeowners in the USA grapple with this. They often pick a number, any number, without truly understanding the implications for their wallet when a pipe bursts or a storm rolls through. My goal today isn’t just to explain what a deductible is. No, we’re going deeper. We’re going to walk through how to choose the right deductible for your unique situation, ensuring you’re not caught off guard. Think of me as your personal guide, helping you avoid that dreaded moment of “I wish I’d known that earlier.”

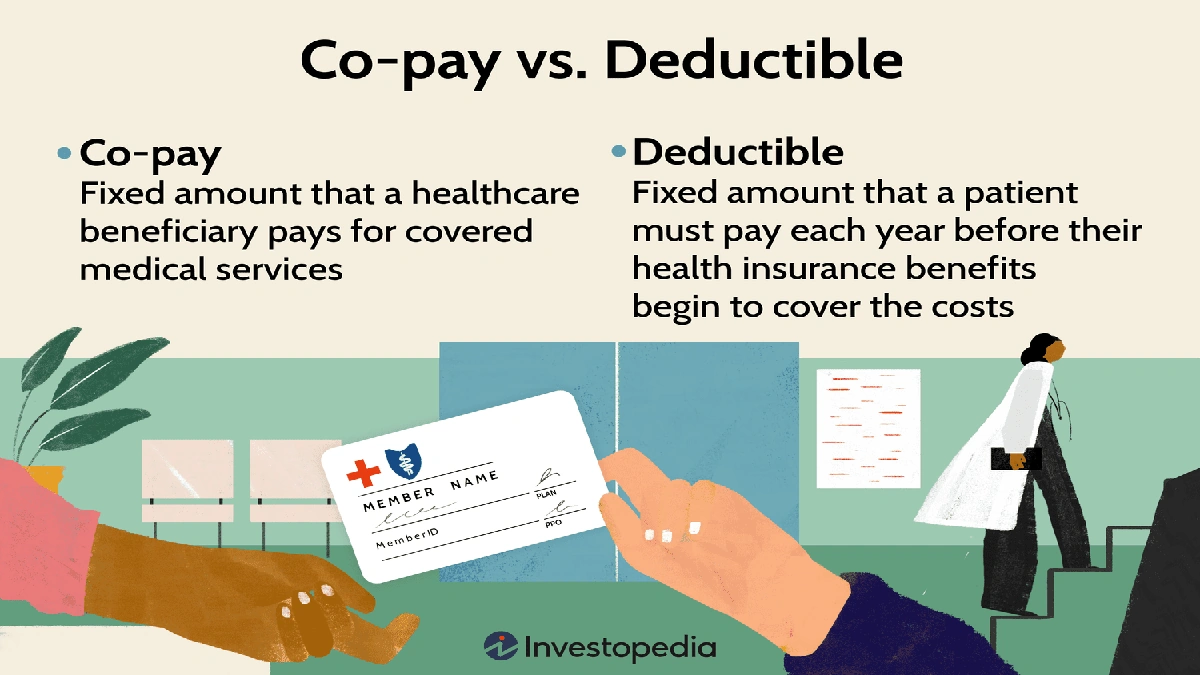

First Things First: What Exactly Is a Deductible? (And Why It Matters)

At its core, a deductible is simply the amount of money you agree to payout of pocketbefore your homeowners insurance policy kicks in to cover a claim. It’s your share of the loss. Imagine your roof gets damaged in a storm, and the repair bill is $10,000. If you have a $1,000 deductible, you pay the first $1,000, and your insurance company pays the remaining $9,000. Simple, right?

But here’s the thing: this seemingly small number has a massive impact on your monthly insurance premium. Generally speaking, the higher your deductible, the lower your premium. Why? Because you’re taking on more of the initial risk assessment yourself, signaling to the insurer that you’re less likely to file small claims. This is a crucial concept when considering insurance premium savings – a higher deductible can significantly reduce your recurring costs. But, and this is a big ‘but,’ it also means you need to have that deductible amount readily available if you ever need to make a property damage claim. This balance is where the smart choices come in.

The Big Two | Flat vs. Percentage Deductibles (And Which One You’re Likely Facing)

When you’re looking at home insurance deductible options in the USA, you’ll primarily encounter two types:

1. The Flat Deductible (or Dollar Amount Deductible)

This is probably what most people think of. It’s a fixed dollar amount, like $500, $1,000, $2,500, or even $5,000. It’s straightforward: whatever the damage, you pay that specific dollar amount first. These are common for most standard perils covered, such as fire, theft, or liability claims. They’re easy to understand and budget for, making financial planning a bit simpler.

2. The Percentage Deductible

Now, this is where things can get a little trickier, and it’s especially prevalent in regions prone to specific natural disasters. A percentage deductible is calculated as a percentage of your home’s dwelling coverage (Coverage A). So, if your home is insured for $300,000 and you have a 1% percentage deductible, your deductible would be $3,000 (1% of $300,000). If it’s a 2% deductible, that jumps to $6,000.

These are most commonly applied to specific perils covered, such as wind, hail, hurricane, or earthquake damage. States like Florida, Texas, and coastal regions, for example, often mandate or strongly encourage hurricane deductibles. This means you could have a standard flat deductible for a fire claim, but a completely different, higher percentage deductible for a windstorm claim. It’s vital to know if your policy includes these, as they can dramatically increase your out-of-pocket costs during a major event.

Navigating the Trade-Off | High Deductible, Low Premium? Or Vice-Versa?

This is the classic dilemma, isn’t it? Choosing between a higher premium (lower deductible) or a lower premium (higher deductible). There’s no universal right answer; it really boils down to your personal risk tolerance and financial situation.

- Lower Deductible, Higher Premium: This option offers greater peace of mind. If you file a property damage claim, your initial out-of-pocket costs will be smaller. This is often preferred by homeowners who have a smaller emergency fund or are simply uncomfortable with the idea of a large, unexpected expense. It’s a bit like paying a premium for certainty.

- Higher Deductible, Lower Premium: This is where you can see significant insurance premium savings. If you have a robust emergency fund (say, 3-6 months of living expenses saved up), you might be comfortable taking on a higher deductible. You’re betting that you won’t file frequent claims, and if you do, you can comfortably cover that initial cost. This approach can be a smart move for those who are diligent with their savings and have a good understanding of their home’s risks. When considering various financial products and tax benefits, understanding these trade-offs is key to holistic wealth management.

Another factor to consider is your mortgage lender requirements. If you have a mortgage, your lender will almost certainly require you to carry homeowners insurance. They also often have minimum deductible requirements, usually capping how high you can go to protect their investment in your home. Always check with your lender before making drastic changes to your coverage options.

Beyond the Basics | Special Deductibles and What to Watch Out For

While flat and percentage deductibles cover the majority of scenarios, some specialized home insurance deductible options exist:

- Hurricane Deductibles: As mentioned, these are specific to hurricane-related damage (wind, hail, storm surge). They’re usually a percentage (1%, 2%, 5%, or even 10%) of your dwelling coverage. The trigger for these can vary by state and insurer – sometimes it’s when a hurricane is named, sometimes when it makes landfall.

- Wind/Hail Deductibles: Similar to hurricane deductibles but can apply to any wind or hail event, not just named hurricanes. Common in tornado alley states.

- Earthquake Deductibles: Predominantly seen in earthquake-prone areas like California. These are almost always percentage-based and can be quite high (often 10% or 15%).

- All Peril Deductibles: Less common, but some policies might offer a single, higher deductible that applies to all types of claims, simplifying the policy but requiring a significant emergency fund.

Understanding these specific deductibles is crucial, especially if you live in an area prone to such events. A standard $1,000 deductible might look great until a hurricane hits, and you discover your actual deductible is 2% of your $400,000 home, meaning you’re on the hook for $8,000. That’s a massive difference when considering out-of-pocket costs for property damage!

Making Your Choice | A Step-by-Step Approach to Choosing a Deductible

So, how do you decide what’s right for you? It’s not just about picking the lowest premium. It’s about smart, informed decision-making. Here’s my personal framework for choosing a deductible:

- Assess Your Emergency Fund: Seriously, this is step one. How much liquid cash do you have readily available for an unexpected home repair? Can you comfortably cover a $1,000, $2,500, or even a $5,000 deductible without dipping into your retirement savings or going into debt? Be brutally honest here. If your emergency fund is thin, a lower deductible might be a wiser, albeit more expensive, choice in terms of premium.

- Evaluate Your Home’s Vulnerability and History: Do you live in an area known for severe weather (tornadoes, hurricanes, heavy snow)? Has your home had property damage claims in the past? A newer home with a strong roof in a low-risk area might warrant a higher deductible. An older home in a storm-prone region might benefit from a lower one. Consider the specific perils covered by your policy and their likelihood.

- Review Your Budget and Cash Flow: Can you comfortably afford a slightly higher monthly insurance premium for the peace of mind a lower deductible offers? Or would those insurance premium savings be better allocated elsewhere, assuming you have the deductible amount saved? This is where your overall financial planning comes into play.

- Consider Small vs. Large Claims: Remember, insurance is for catastrophic losses, not minor repairs. If you have a very low deductible ($500), you might be tempted to file claims for smaller issues. However, filing multiple small claims can lead to your insurer increasing your rates or even declining to renew your policy. A higher deductible naturally discourages small claims, which can be a good thing for maintaining a favorable claims process history.

- Consult Your Mortgage Lender: As mentioned, always double-check any mortgage lender requirements regarding minimum coverage options and maximum deductibles.

- Shop Around and Compare: Don’t just stick with your current insurer. Different companies have different pricing models and coverage options. Use online comparison tools – much like you would for pay-per-mile car insurance comparison – to see what other providers offer for similar coverage and various deductible levels. This can reveal significant insurance premium savings.

FAQs | Your Burning Questions About Home Insurance Deductibles Answered

Can I change my deductible anytime?

Yes, usually you can. Most insurers allow you to adjust your deductible at any time, though it’s most common to do so at your policy’s renewal. Be aware that changing it mid-term might involve a pro-rated adjustment to your insurance premium.

What happens if I file a claim with a high deductible?

If you file a claim, you’ll be responsible for paying your deductible amount directly to the contractor or service provider, or it will be subtracted from the total settlement amount paid by your insurer. For example, if repairs cost $10,000 and your deductible is $5,000, the insurer will pay you $5,000. It’s your initial out-of-pocket costs.

Are deductibles tax-deductible?

Generally, no. Homeowners insurance premiums and deductibles are typically not tax-deductible for personal residences. However, if you use a portion of your home for a home-based business, some expenses, including a portion of your insurance, might be deductible. Always consult a tax professional for personalized advice.

Does my mortgage lender care about my deductible?

Absolutely. Your mortgage lender has a vested interest in your home’s value, so they’ll require you to carry homeowners insurance and often set limits on how high your deductible can be. This protects their investment in case of significant property damage.

How often should I review my deductible?

I recommend reviewing your home insurance deductible options annually at renewal time, or whenever there’s a significant life change (e.g., getting a raise, building up your emergency fund, major home renovations, or changes in local weather patterns). Your risk assessment isn’t static, and neither should your insurance choices be.

Choosing the right deductible for your homeowners insurance policy in the USA is more than just picking a number; it’s a strategic decision that impacts your financial security. By understanding the nuances of flat deductible versus percentage deductible, assessing your risk tolerance, and making informed choices about your coverage options, you empower yourself. Don’t just let the insurance company dictate your terms. Take control, ask questions, and ensure your home is protected in a way that truly fits your life and your wallet. It’s your home, your money, and your peace of mind we’re talking about.