Let’s be honest, the phrase “affordable home insurance with high coverage USA” often feels like an oxymoron, doesn’t it? Like finding a unicorn that also bakes perfect sourdough. You want to protect your biggest asset – your home – with robust coverage, but you dread the premium sticker shock. I get it. The sheer volume of options, the confusing jargon, and the nagging fear of either overpaying or, worse, being underinsured when disaster strikes, can be paralyzing. But what if I told you it doesn’t have to be that way? What if there’s a clear, actionable path to securing a policy that genuinely protects your sanctuary without emptying your wallet?

My goal here isn’t just to throw information at you. Instead, I want to be your guide, the knowledgeable friend who’s navigated these waters before and can help you avoid the common pitfalls. We’re going to break down the process, step by step, showing you how to secure that elusive sweet spot: affordable home insurance with high coverage USA. This isn’t about cutting corners; it’s about smart strategies, understanding the game, and making informed decisions that truly pay off.

Decoding the “Affordable” and “High Coverage” Myth

First things first, let’s redefine what these terms actually mean in the context of your home. When we talk about “affordable,” we’re not just chasing the absolute lowest premium. No, sir. That’s a trap. True affordability in insurance means getting exceptional value for your money – a policy that fits your budget and provides comprehensive protection when you need it most. It’s about finding that equilibrium where cost meets robust security, ensuring you’re not left high and dry after a major event.

And “high coverage”? This isn’t just about having a big number on your policy. It’s about having the right kind of coverage for your specific situation. This typically includes dwelling coverage (for the structure of your home), personal property coverage (for everything inside), liability protection (if someone gets hurt on your property), and additional living expenses (if you can’t live in your home during repairs). Understanding these core `types of home insurance coverage` is crucial. Many policies also include specific protections like water backup or extended replacement cost, which can be game-changers.

The trick, then, is balancing these two. It’s easy to find cheap insurance with minimal coverage, or high coverage at an exorbitant price. The real challenge, and where we’ll focus our energy, is finding `best homeowners insurance` that offers robust protection without breaking the bank. It’s entirely possible, and frankly, it’s what every homeowner deserves.

Your Step-by-Step Blueprint to Finding the Sweet Spot

Let’s get practical. Here’s how you can systematically approach finding the ideal affordable home insurance with high coverage USA.

Step 1 | Assess Your Needs (and Ditch the Guesswork)

Before you even think about getting `home insurance quotes`, you need to understand what you’re actually protecting. This isn’t just about your home’s market value, which can be misleading. Instead, focus on its rebuilding cost. What would it cost to reconstruct your home from the ground up today? This includes materials, labor, and debris removal. Tools from insurance companies or independent appraisers can help with this.

Next, take stock of your personal belongings. I know, it sounds tedious, but trust me, a detailed inventory (with photos or videos!) can be a lifesaver if you ever need to file a claim. This helps you determine your required personal property coverage. Don’t forget about specific high-value items like jewelry, art, or collectibles, which often require special endorsements beyond standard limits. This foundational work goes beyond just basichome insurance quotes; it’s about understanding your true exposure.

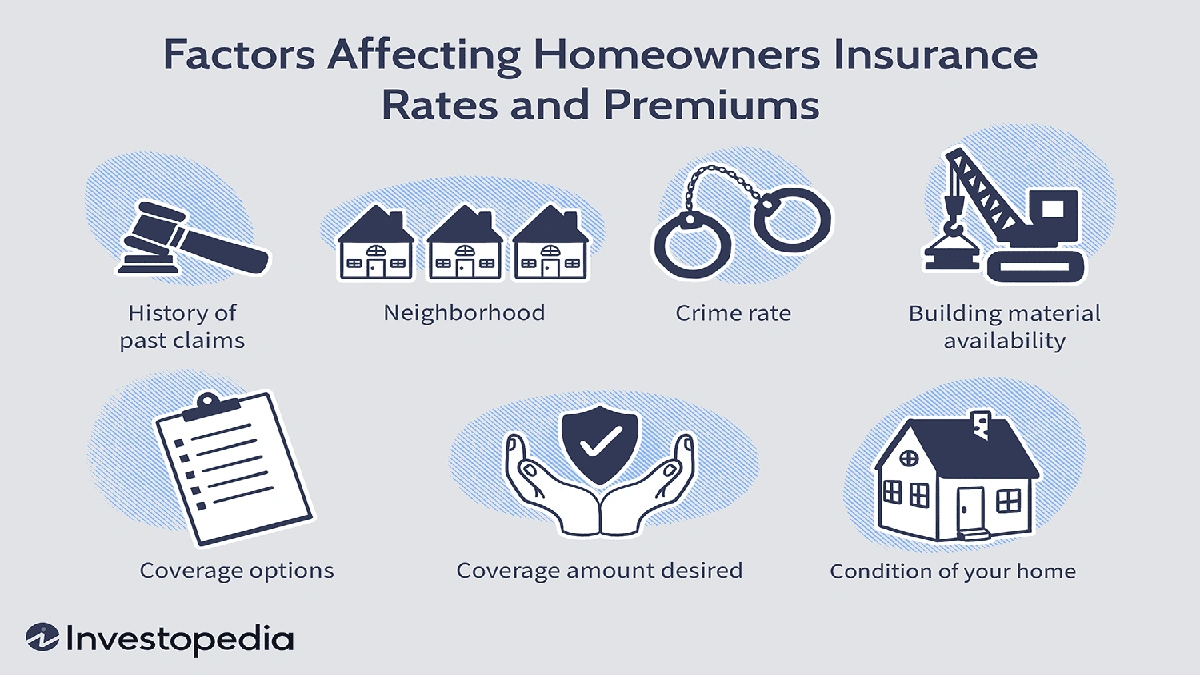

Step 2 | Understand the Factors That Drive Premiums

This is where the “why” behind the `cost of home insurance` comes into play. I initially thought location was everything, but then I realized there’s a whole constellation of `factors affecting home insurance premiums` that insurers consider. Knowing these can help you anticipate costs and even make changes to lower them:

- Location: Proximity to fire hydrants, crime rates, and natural disaster zones (hurricanes, earthquakes, floods) are huge.

- Age and Construction of Your Home: Older homes might have outdated systems (plumbing, electrical) that are riskier. Certain construction materials are more resilient.

- Claims History: Your past claims, and even the claims history of previous owners, can influence your rates.

- Credit Score: In many states, a higher credit-based insurance score can lead to lower premiums.

- Deductibles: The amount you pay out-of-pocket before your insurance kicks in. (More on this in Step 3!)

- Security Features: Alarms, deadbolts, sprinkler systems, and even smart home tech can earn you discounts.

Understanding these drivers empowers you to ask the right questions and, in some cases, take proactive steps to reduce your risk profile, ultimately leading to more affordable home insurance with high coverage USA.

Step 3 | Leverage Deductibles and Discounts Like a Pro

This is where you can significantly impact your `cheap home insurance policies` premium without sacrificing crucial coverage. It’s all about smart adjustments.

Deductibles: Choosing a higher deductible is one of the quickest ways to lower your annual premium. If you can comfortably cover a $1,000 or $2,500 deductible out of pocket for a claim, you’ll see substantial savings compared to a $500 deductible. Just make sure it’s an amount you can afford to pay without financial strain.

Discounts: Insurers offer a surprising array of `deductibles and discounts`. Always ask about:

- Bundling: Combining your home and auto insurance with the same carrier often leads to significant savings on both policies. If you’re looking for best car insurance college students USA, you might find a great deal bundling with your home policy.

- Home Safety & Security: Smoke detectors, carbon monoxide detectors, alarm systems, deadbolts, and even smart home security devices can qualify.

- New Roof/Renovation: A recently updated roof or major system upgrades can reduce risk and premiums.

- No Claims History: Being claim-free for several years often earns a loyalty discount.

- Mature Homeowner: Many companies offer discounts for policyholders over a certain age.

- Payment Method: Setting up automatic payments or paying your premium annually can sometimes lead to small reductions.

Don’t just assume; always ask your agent what `deductibles and discounts` you qualify for. It’s literally money back in your pocket.

Step 4 | Shop Smart, Compare Widely

This might seem obvious, but it’s astonishing how many people stick with their current provider year after year without exploring alternatives. To find the truly affordable home insurance with high coverage USA, you must shop around. Don’t just take the first offer, or even the second. Aim to get at least three to five `home insurance quotes` from different carriers.

You can do this in a few ways: using online comparison tools, contacting individual insurance companies directly, or working with an independent insurance agent. Independent agents are particularly useful because they work with multiple carriers and can do the comparison shopping for you, often finding policies that you might miss on your own. They can also help you with `understanding policy limits` and ensure you’re comparing apples to apples when looking at different offers.

Beyond the Price Tag: What to Look For in a Best Homeowners Insurance Policy

While price is important, it’s not the only metric. When evaluating `best homeowners insurance` policies, consider these critical elements:

- Insurer Reputation & Financial Strength: Look for companies with strong financial ratings (e.g., A.M. Best) and positive customer service reviews. You want an insurer that will be there and pay claims promptly when you need them.

- Customer Service: How easy is it to reach a human? Do they have a user-friendly online portal for managing your policy and claims? This matters immensely during stressful times.

- Policy Exclusions: Understand what’s not covered. Standard policies, for instance, typically exclude flood and earthquake damage. If you live in an at-risk area, you’ll need separate policies or endorsements for these.

- Endorsements & Riders: These are additions to your standard policy that provide extra coverage. Think about things like water backup, identity theft protection, or extended replacement cost for your dwelling. This is key to truly `finding high coverage insurance`.

- Replacement Cost vs. Actual Cash Value: Always aim for replacement cost coverage for both your dwelling and personal property. Actual cash value policies pay out based on depreciated value, which means you’ll get less money to replace items than they cost new.

Common Pitfalls to Avoid When Securing Your Home

Even with the best intentions, it’s easy to stumble. Here are a few `homeowners policy tips` to keep in mind:

- Underinsuring Your Home: This is a massive mistake. As we discussed, focus on rebuilding cost, not market value. Inflation and rising construction costs mean you should review your coverage annually to ensure it keeps pace.

- Ignoring Endorsements: Don’t assume everything is covered. If you have a home office, a trampoline, or a valuable art collection, make sure you have the right endorsements.

- Not Reviewing Annually: Your life changes, and so should your policy. Did you renovate? Buy new expensive electronics? Improve your home’s security? These changes can affect your coverage needs and potential discounts.

- Failing to Ask About Discounts: Seriously, ask! You might be surprised by what you qualify for.

- Not Documenting Your Belongings: A home inventory is tedious but invaluable. In the chaos after a loss, remembering every item you own is nearly impossible.

Your Burning Questions About Home Insurance, Answered

How can I genuinely find affordable home insurance with high coverage USA?

The key is a multi-pronged approach: accurately assess your needs, understand `factors affecting home insurance premiums`, leverage all available `deductibles and discounts`, and compare `home insurance quotes` from multiple providers. Don’t just look for the cheapest premium; seek the best value for robust protection.

What are the main `types of home insurance coverage` I should consider?

Typically, you’ll want dwelling coverage (structure), personal property (contents), liability (injuries on your property), and additional living expenses. Depending on your location and assets, consider endorsements for things like water backup, identity theft, or scheduled personal property for high-value items.

Does my credit score really impact my `home insurance quotes`?

Yes, in most states, insurers use a credit-based insurance score as one of the `factors affecting home insurance premiums`. A higher score generally indicates a lower risk, potentially leading to more favorable rates. Maintaining good credit can help you secure more affordable home insurance with high coverage USA.

Is it always better to choose a higher deductible for `cheap home insurance policies`?

Not always, but often. A higher deductible will lower your premium, making your policy more “affordable.” However, you must be comfortable paying that deductible out of pocket if you file a claim. If a higher deductible creates financial strain, it’s not the right choice for you.

How often should I review my homeowners policy tips?

You should aim to review your policy at least once a year, or whenever significant life events occur. This includes major renovations, purchasing expensive new items, changes in your family structure, or even changes in local building codes. An annual review ensures your `understanding policy limits` and coverage remains appropriate for your current situation.

Final Thoughts | Empowering Your Home’s Protection

Navigating the world of affordable home insurance with high coverage USA might seem daunting, but it’s entirely manageable with the right approach. By understanding your needs, knowing what drives costs, and diligently comparing options, you’re not just buying a policy – you’re investing in peace of mind. Your home is your sanctuary, and protecting it shouldn’t be a source of anxiety. It should be a strategic decision, empowering you to face whatever comes your way, knowing you’re well-covered. Go forth, compare wisely, and secure the protection your home truly deserves!