Let’s be honest, car insurance in the USA can feel like a black hole for your money. You pay month after month, year after year, often feeling like you’re overpaying, especially if your car spends more time in the driveway than on the highway. What if I told you there’s a different way, a potentially revolutionary approach that could genuinely save you significant cash? We’re talking about pay per mile car insurance USA comparison – and trust me, it’s not just another fad.

I initially thought this was straightforward, just paying for what you use, right? But then I realized the deeper implications, the ‘why’ behind its growing popularity, and why it’s becoming a serious contender against traditional policies. This isn’t just about saving a few bucks; it’s about a fundamental shift in how insurance companies view risk and how you, the driver, can leverage that to your advantage. For too long, the system has felt rigged against the casual driver, but that narrative is finally changing.

What Exactly Is Pay-Per-Mile Insurance, Anyway? (And Why It’s Not Just a Gimmick)

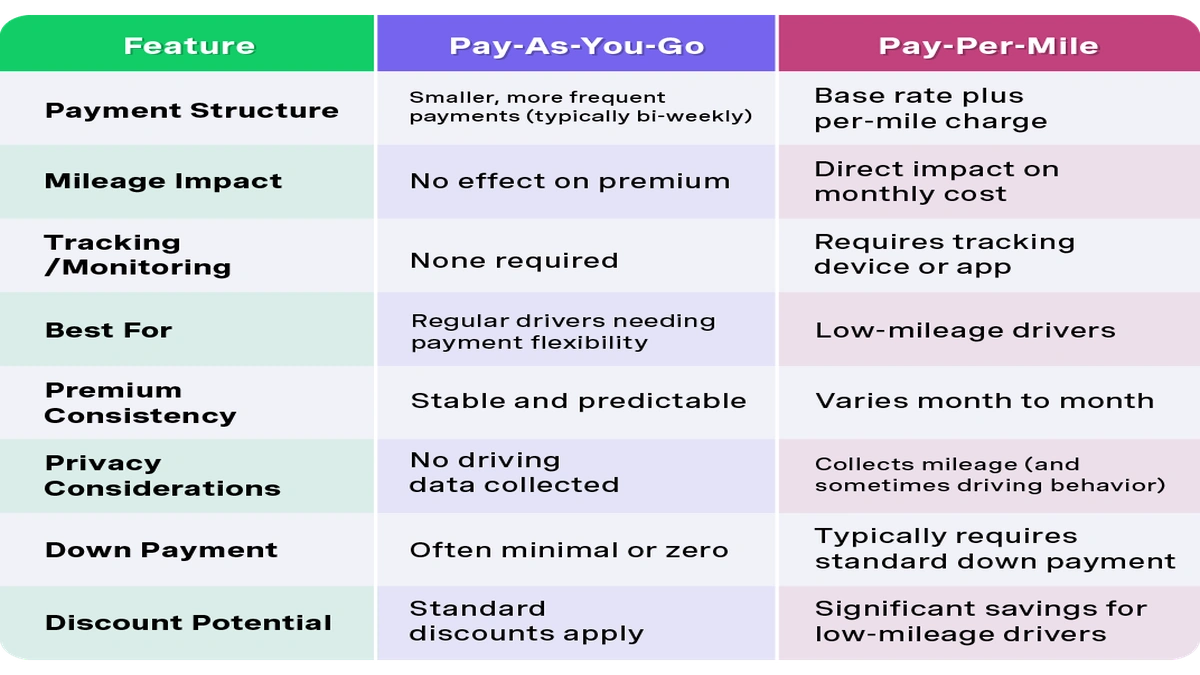

At its core, pay per mile car insurance USA comparison is exactly what it sounds like: you pay a base rate (often a low monthly fee) and then an additional few cents for every mile you drive. Simple, right? But the beauty lies in its departure from traditional car insurance models, which typically charge a flat premium based on a complex cocktail of factors like your age, driving record, vehicle type, location, and even credit score – regardless of how much you actually use your car.

This isn’t just a random idea; it’s part of a broader movement towards `usage-based insurance` (UBI), powered by something called `telematics`. Think of telematics as the tech wizardry that tracks your driving. This usually involves a small device you plug into your car’s OBD-II port, or increasingly, a `mileage tracking app` on your smartphone. These devices don’t just count miles; some can monitor driving behavior like hard braking, rapid acceleration, and even the time of day you drive. What fascinates me is how this data, once the exclusive domain of actuarial tables, is now put directly into the hands of the consumer, offering a clear link between usage and cost.

So, why isn’t it a gimmick? Because it directly addresses a pain point for a massive segment of the driving population: `low mileage drivers`. If you work from home, use public transport often, or have a second car that rarely leaves the garage, why should you pay the same hefty `insurance premiums` as someone who commutes 50 miles daily? This model offers a logical, data-driven solution that reflects your actual exposure to risk on the road. It’s about fairness, plain and simple.

The Hidden Costs & Clever Savings | Comparing Pay-Per-Mile vs. Traditional

When we talk about `car insurance rates`, there’s a lot that goes into the calculation. With traditional insurance, the company is essentially betting on your overall risk profile. They assume you’ll drive a certain amount, and they price accordingly. If you drive significantly less than that assumed average, you’re essentially subsidizing higher-mileage drivers. That’s the hidden cost I’m talking about.

With pay-per-mile, that dynamic flips. Your base rate covers your car when it’s parked – think theft, fire, comprehensive coverage – and then your per-mile rate kicks in for liability and collision when you’re actually driving. This structure can lead to clever savings, especially for those driving under 7,500-10,000 miles a year. I’ve seen scenarios where individuals cut their bills by 30-50%, which, let’s be honest, is a substantial chunk of change that could go towards anything from a new gadget to that much-needed vacation.

But here’s the thing: it’s not a magic bullet for everyone. If you’re a road warrior, constantly racking up thousands of miles, a pay-per-mile plan might actually end up being more expensive than a traditional policy. The key is understanding your driving habits and doing a thoroughcar insurance renewal onlinecomparison. Don’t just look at the lowest base rate; project your annual mileage and calculate the total estimated cost. This is where the ‘analyst’ in you needs to come out.

Beyond the Miles | What Else Influences Your Pay-Per-Mile Premium?

While miles driven are the star of the show, it’s crucial to understand that pay-per-mile isn’t just about the odometer. Factors like your age, driving history (speeding tickets, accidents), the type of car you drive (a sports car versus a sedan), and even where you live still play a role in determining your base rate and sometimes even your per-mile rate. These are universal truths in the insurance world, regardless of the model.

The `telematics` device or `mileage tracking app` also introduces a new layer of influence: your actual driving behavior. Some providers will offer discounts for safe driving habits – smooth acceleration, gentle braking, avoiding late-night drives. This data can be a double-edged sword: great for rewarding careful drivers, but potentially punitive for those with a lead foot. It’s an interesting evolution, pushing drivers towards safer habits, which benefits everyone on the road. Many different insurance companies are now offering these plans, each with slightly different algorithms and pricing structures. For more on how telematics is reshaping the industry, you might find thisWikipedia article on Telematicsinsightful.

Navigating the Landscape | A Practical Comparison Guide for the USA

So, how do you actually compare `pay per mile car insurance USA comparison` options? It starts with honest self-assessment. How many miles do you really drive in a typical month or year? Be realistic, not aspirational. Then, gather quotes from several reputable providers. Companies like Metromile, Root, and Allstate (with their Milewise program) are prominent players in this space, but new options are emerging all the time.

When comparing, don’t just eyeball the numbers. Look at:

- The Base Rate: What’s the fixed monthly cost, regardless of miles?

- The Per-Mile Rate: How much per mile? (This is usually just a few cents.)

- Daily Caps: Some policies cap the number of miles you’re charged for in a single day (e.g., you might only pay for the first 150 miles, even if you drive 300). This is HUGE for road trips!

- Coverage Options: Ensure the pay-per-mile policy offers the same level of liability, comprehensive, and collision coverage you need, just like a traditional plan.

- Technology: Is it a plug-in device or an app? How comfortable are you with the data tracking?

- Customer Reviews: What are other users saying about the company’s service and claims process?

It’s also worth checking if your current insurer offers a pay-per-mile option. Sometimes, bundling can lead to additional savings. And remember, exploring options likeinstant approval life insurance USA onlinecan be another way to optimize your overall insurance portfolio, but that’s a story for another day. For now, focus on your wheels!

Frequently Asked Questions About Pay-Per-Mile Car Insurance

Is pay-per-mile insurance right for everyone?

No, it’s particularly beneficial for `low mileage drivers` (typically under 7,500-10,000 miles per year). If you drive a lot, `traditional car insurance` might be more cost-effective.

How do they track my miles?

Most providers use a small `telematics` device that plugs into your car’s OBD-II port, or a smartphone `mileage tracking app` that uses GPS. This data is then used to calculate your per-mile charges.

What if I take a long road trip?

Many `pay per mile car insurance USA comparison` policies include daily mileage caps. For example, you might only be charged for the first 150-250 miles driven in a single day, even if you drive further. Always check the specific terms with your provider.

Can I switch back to traditional insurance easily?

Generally, yes. Switching insurance providers is a common practice. You can usually get quotes for traditional policies and switch if a pay-per-mile plan isn’t working out for you.

Are there privacy concerns with telematics?

Some drivers do have privacy concerns regarding data collection. Insurance companies typically state they only use data for pricing and claims, and it’s protected. It’s important to read the privacy policy of any provider you consider.

So, there you have it. The world of car insurance is evolving, and pay-per-mile isn’t just a niche offering anymore. It’s a legitimate, often superior, option for a significant portion of American drivers. Don’t just accept the status quo of ever-increasing `insurance premiums`. Take the time to understand your options, compare, and potentially unlock substantial savings that you didn’t even know were within reach. Your wallet will thank you.