Alright, let’s talk about something that often feels like navigating a dense jungle: US health insurance. For many, it’s a topic shrouded in jargon and anxiety, something we deal with only when we absolutely have to. But here’s the thing, and what truly fascinates me about the American system: the choice between private health insurance and employer-sponsored plans isn’t just about premiums. It’s about control, flexibility, long-term financial health, and honestly, your peace of mind. And understanding why one might be a vastly better fit for you than the other is crucial, especially when life throws a curveball.

I’ve seen countless people just default to whatever their employer offers, or jump into a private plan without fully grasping the implications. And let me tell you, that can be a costly mistake. We’re going to pull back the curtain today and look beyond the surface-level comparisons, diving deep into the hidden layers that truly differentiate these two major health insurance options USA has to offer. It’s time to get a real handle on this, not just for today, but for your future.

The Lay of the Land | Understanding America’s Health Insurance Maze

So, what exactly are we comparing? On one side, you haveemployer-sponsored health insurance, which is what most Americans are familiar with. It’s often seen as a perk, a benefit that comes with a job. On the other side, there’s private health insurance , which you purchase directly from an insurer or through a marketplace like Healthcare.gov. On the surface, both provide coverage, right? Well, yes, but the devil, as always, is in the details.

I initially thought this was a straightforward comparison of cost and coverage, but then I realized it’s much more nuanced. The underlying structure, the regulatory environment, and even your personal life circumstances can dramatically shift the value proposition of each. For instance, the sheer complexity of healthcare costs America faces means that a seemingly cheaper option might hide massive out-of-pocket expenses later. It’s not just about what you pay monthly; it’s about what you pay when you actually need care, and how much control you have over that entire process.

Employer-Sponsored Health Insurance | The ‘Default’ Option’s Hidden Layers

For many, employer-sponsored health insurance is the golden standard. Why? Because employers typically subsidize a significant portion of the premiums, making it appear more affordable upfront. It’s convenient, too; you enroll, and boom, you’re covered. No need to shop around, compare plans, or understand the intricacies of different carriers. Your HR department usually handles the heavy lifting, which is a huge relief for many.

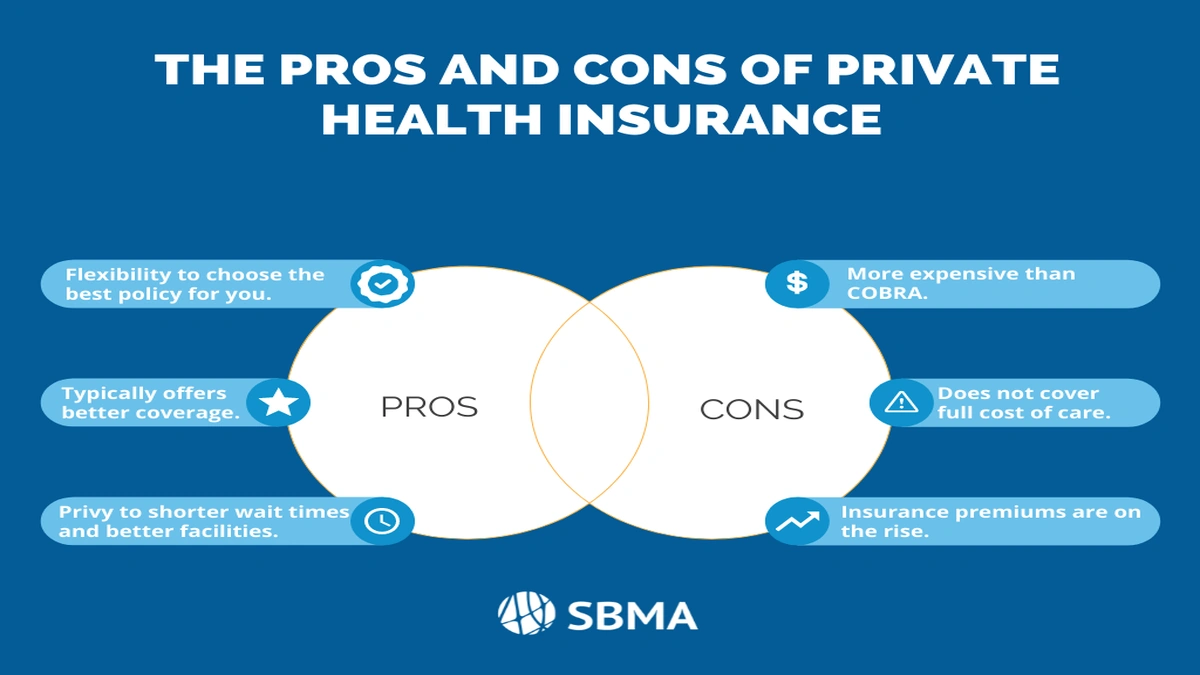

But let’s be honest, this convenience comes with trade-offs. Your choices are limited to what your employer offers, which might not always align with your specific health needs or preferred doctors. What happens if you lose your job? Suddenly, that seemingly stable coverage vanishes, often leaving you with the option of COBRA (which is notoriously expensive) or scrambling for a new plan during a stressful time. This lack of control, and the inherent link to your employment status, is a critical factor often overlooked when people arechoosing health coverage. It’s a fantastic benefit when you have it, but it’s a tether that can become a vulnerability.

Venturing Out | The World of Private Health Insurance Plans

Now, let’s talk about private health insurance . This is where you, the individual, take the reins. You can purchase plans directly from insurance companies or through the Health Insurance Marketplace established by the Affordable Care Act (ACA). The biggest advantage here? Choice and flexibility. You can scour various individual health plans America offers, picking one that perfectly matches your budget, health needs, preferred doctors, and even your risk tolerance. If you’re self-employed, a freelancer, or simply prefer to decouple your health coverage from your job, this is your path.

However, this freedom often comes with a higher sticker price, especially if you don’t qualify for subsidies under the ACA. WhileACA planshave made private insurance more accessible and comprehensive, guaranteeing coverage regardless of pre-existing conditions, the premium costs can still be substantial. You’ll need to pay close attention to deductibles , co-pays, and out-of-pocket maximums, as these can vary wildly. It requires more homework, more active participation, but it grants you a level of independence that employer plans simply can’t.

The Great Showdown | When Does One Outshine the Other?

So, when does one option truly stand out? It’s not a simple one-size-fits-all answer, which is why this comparison is so vital. If you have a stable job with excellent benefits, and your employer covers a large chunk of the premiums, then an employer-sponsored plan is often the most cost-effective and convenient choice. This is especially true if you have a family, as group rates can be very competitive.

However, consider life changes. If you’re contemplating a career change, thinking of starting your own business, or if your employer’s plan simply doesn’t meet your specific needs (maybe you need a very specific specialist not in their network), then private insurance starts to look very appealing. The flexibility to choose your own plan, regardless of your employment status, offers invaluable peace of mind. This is where the debate of COBRA vs private insurance really heats up; often, a private plan through the marketplace, especially with subsidies, can be significantly cheaper than continuing your old employer plan via COBRA after a job loss. Understanding your various coverage options before you need them is part of being prepared.

Beyond the Premiums | What Really Drives Your Decision

Let me rephrase that for clarity: the monthly premium is just one piece of the puzzle. When evaluating health insurance USA , you absolutely must dig into the deductibles , co-insurance, co-pays, and the out-of-pocket maximum . A plan with a low premium might have a sky-high deductible, meaning you pay a lot out of pocket before insurance kicks in. Conversely, a higher premium might come with a lower deductible and more predictable costs.

Also, consider the network of providers. Employer plans often have tightly managed networks, which can limit your choice of doctors and hospitals. Private plans can offer more flexibility, but you still need to check if your preferred providers are in-network. The goal here isn’t just to have insurance, but to have useful insurance that works for your life. And trust me, having a plan that covers your needs is far more valuable than the cheapest option that leaves you stranded when you need care most. This is about understanding the intricacies of the American healthcare system and making an informed decision, not just a quick one. Always be mindful of enrollment periods too; both types of plans have specific windows for signing up or making changes, so don’t miss them! Knowing the difference between these plans can even impact your business decisions, especially if you’re a small business owner consideringprofessional indemnity insurance businessneeds alongside your personal health coverage.

Frequently Asked Questions About US Health Insurance

Is private health insurance always more expensive than employer plans?

Not necessarily. While employer plans often have subsidized premiums, private plans can be more affordable if you qualify for tax credits through the Affordable Care Act marketplace. It heavily depends on your income, family size, and the specific plan chosen.

What happens to my employer health insurance if I lose my job?

Typically, you’ll have the option to continue your employer plan through COBRA for a limited time, but you’ll pay the full premium plus an administrative fee, making it very expensive. Alternatively, you can seek a private plan through the Health Insurance Marketplace, which might be more affordable.

Can I switch from an employer plan to a private plan anytime?

Generally, no. You can usually only switch during an open enrollment period (for either type of plan) or if you experience a qualifying life event, such as losing job-based coverage, getting married, or having a baby.

What are the key things to compare when looking at health insurance options USA?

Beyond the monthly premium, compare the deductible, co-pays, co-insurance, out-of-pocket maximum, and the provider network. These factors significantly impact your total costs and access to care.

Is the Affordable Care Act still relevant for individual health plans America?

Absolutely. The ACA remains the foundation for the individual health insurance market, providing consumer protections, subsidies for eligible individuals, and the Health Insurance Marketplace where many private plans are sold.

So, there you have it. The choice between private health insurance vs employer USA comparison isn’t just a technicality; it’s a deeply personal decision with significant financial and health implications. Don’t let the complexity deter you from making an informed choice. Take the time to understand your options, assess your needs, and then pick the path that truly empowers you. Because in the end, it’s your health, your money, and your future we’re talking about. And that, my friend, is something worth investing your time in.