Let’s be honest, the thought of getting life insurance can feel like a trip to the dentist – necessary, but often dreaded. You picture endless paperwork, intrusive medical exams, and waiting weeks for approval. But what if I told you there’s a different path, one where you can secure vital coverage without the needles and the waiting games? We’re talking about finding no medical exam term life insurance USA cheap, and it’s more accessible than you might think.

I get it. Life in the U.S. moves fast. You’ve got a family to protect, a mortgage to cover, and maybe even some dreams you’re building. Time is precious, and frankly, so is your peace of mind. That’s why the idea of an instant, hassle-free insurance policy is so appealing. But can it really be cheap? Can it truly be simple? Let’s dive in and unravel this together, because securing your family’s financial future shouldn’t add more stress to your plate.

Understanding the ‘No Medical Exam’ Advantage | Is It Really for You?

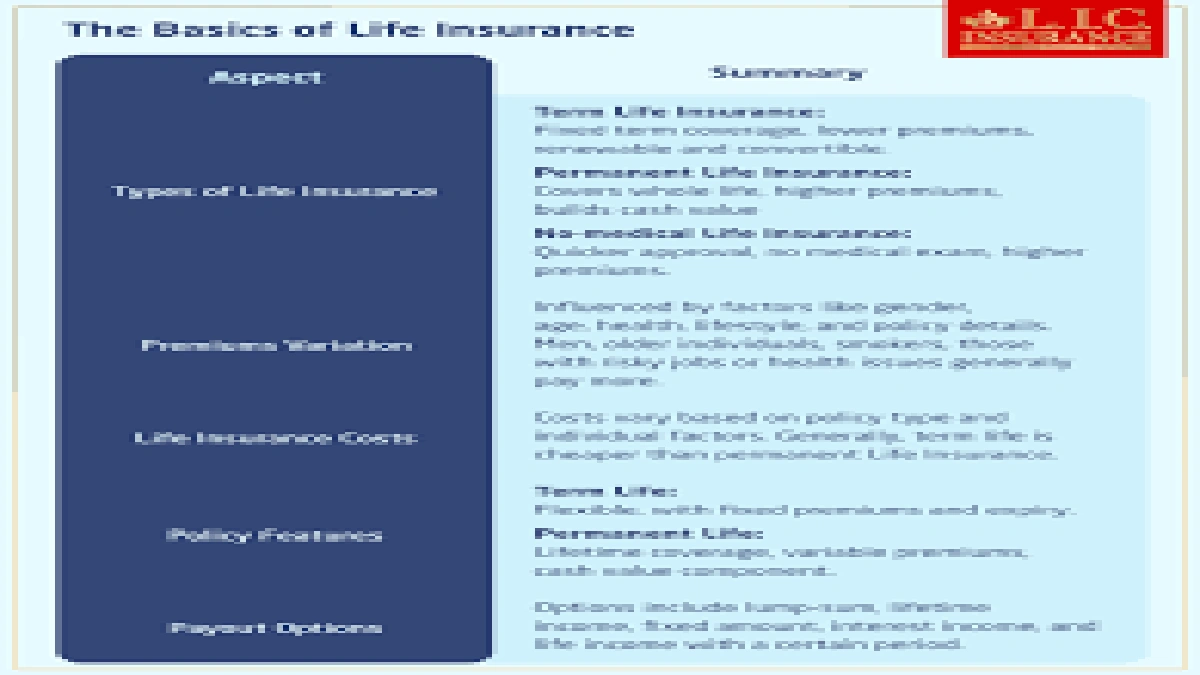

First things first, let’s clear up what ‘no medical exam’ actually means. It doesn’t mean you get a free pass on all health questions. Instead, it means the insurer relies on other data points to assess your risk, effectively streamlining the application process. This typically falls into two main categories: simplified issue life insurance and guaranteed issue life insurance.

Simplified Issue | The Middle Ground

With simplified issue policies, you’ll answer a series of health questions – usually 10-20 concise queries about your medical history, lifestyle, and current health status. The insurer then uses this information, combined with databases like the Medical Information Bureau (MIB), prescription drug history, and motor vehicle records, to make a quick decision. You won’t face a paramedical exam, blood tests, or urine samples. This is often where you’ll find truly affordable no medical exam policy options, especially if you’re in reasonably good health but just want to skip the exam hassle.

The beauty of simplified issue is its speed. Approvals can happen in days, sometimes even minutes, making it a fantastic option for those who need coverage fast. What fascinates me about this approach is how technology has enabled insurers to make informed decisions without the traditional, time-consuming methods. It’s a testament to how the industry is adapting to modern consumer needs, offering genuine term life insurance without health check benefits.

Guaranteed Issue | When Health Is a Major Concern

Then there’s guaranteed issue. As the name suggests, approval is pretty much guaranteed, regardless of your health. You won’t answer health questions, and there’s no medical exam. This type of policy is typically for individuals with significant health issues who might not qualify for other types of life insurance. However, and this is crucial, these policies usually come with higher premiums, lower coverage amounts, and often a waiting period (typically 2-3 years) before the full death benefit pays out. If death occurs during this waiting period, beneficiaries usually receive a refund of premiums paid plus interest.

So, while it offers a safety net for those who need it most, it’s generally not where you’ll find the absolute cheap no medical exam life insurance options. It’s more about accessibility than affordability in the traditional sense. Understanding this distinction is key to setting realistic expectations when you’re searching for life insurance without medical exam options.

The Price Tag Puzzle | How ‘Cheap’ is ‘Cheap’ for No Exam Policies?

Okay, so you’re interested in the convenience, but what about the cost? Is it possible to get no medical exam term life insurance USA cheap? The answer is a resounding ‘yes,’ but with a few caveats. Generally, because insurers are taking on a slightly higher risk without a full medical picture, no-exam policies can be marginally more expensive than fully underwritten policies for someone in perfect health. However, for many people, the difference is negligible, and the convenience factor often outweighs the slight premium increase.

Several factors influence the cost:

- Age: This is probably the biggest factor. The younger and healthier you are, the lower your premiums will be.

- Coverage Amount: More coverage means higher premiums. Determine how much you truly need to avoid overpaying. A good rule of thumb is 5-10 times your annual income, but everyone’s situation is unique.

- Term Length: Term life insurance, by its nature, is for a specific period (e.g., 10, 20, 30 years). Longer terms generally mean higher premiums.

- Health Questions: For simplified issue, your answers to health questions will directly impact your rates. Being honest is paramount.

- Lifestyle: Smoking, high-risk hobbies, and certain occupations can also increase costs.

My experience tells me that comparing quick life insurance quotes from multiple providers is non-negotiable here. Don’t settle for the first quote you get. Different companies have different underwriting algorithms and target demographics, meaning one insurer might see your profile more favorably than another. You can use tools like an online life insurance premium calculator to get preliminary estimates, which can be a real eye-opener.

Your Step-by-Step Guide to Finding the Best No Exam Term Life Insurance

Ready to get started? Here’s a practical, step-by-step guide to help you find the best no exam life insurance companies and secure an affordable term life insurance policy without the medical hassle:

- Assess Your Needs: Before you even look at a policy, figure out how much coverage you truly need and for how long. Consider your debts (mortgage, loans), future expenses (college tuition), and income replacement needs. This foundational step will prevent you from buying too little or too much.

- Understand Your Health Profile: Be realistic about your health. If you have a clean bill of health, simplified issue is likely your best bet for better rates. If you have serious pre-existing conditions, guaranteed issue might be your only option, but understand its limitations.

- Research Reputable Insurers: Not all insurance companies offer the same range of no-exam products, or at the same competitive rates. Look for providers known for their financial stability (check ratings from agencies like A.M. Best or Standard & Poor’s) and good customer service. Many established insurers now have robust no-exam offerings.

- Gather Multiple Quotes: This is where the magic happens for finding a truly cheap no medical exam life insurance policy. Use online comparison sites or work with an independent agent who can shop around for you. Don’t just look at the premium; compare policy features, riders, and the insurer’s reputation.

- Read the Fine Print (Seriously!): I can’t stress this enough. Understand the policy’s terms, conditions, exclusions, and any waiting periods (especially for guaranteed issue). Are there accelerated death benefit riders? What happens if you miss a payment? A good consumer guide from the NAIC can help you understand common policy terms.

- Apply Online or with an Agent: Once you’ve chosen a policy, the application process for no-exam policies is usually straightforward. Many can be completed entirely online in under an hour, leading to instant approval life insurance in some cases.

Beyond the Basics | What to Watch Out For

While the convenience of no medical exam term life insurance USA is undeniable, there are a few things to keep in mind:

- Coverage Limits: No-exam policies often have lower maximum coverage limits compared to fully underwritten policies. If you need a very large death benefit (e.g., over $1 million), a traditional exam policy might be your only route.

- Potential for Higher Premiums: As mentioned, without a full medical exam, insurers take on a bit more risk. This can translate to slightly higher premiums, especially if you’re in excellent health and would easily pass a medical exam. However, for many, the time saved and simplicity gained are worth the small difference.

- The ‘Instant’ Misconception: While many policies boast instant approval life insurance, it’s important to differentiate between instant decision and instant coverage. An instant decision means you know if you’re approved quickly, but the policy might not be fully active until the first premium is paid and all administrative checks are complete.

- Understanding Riders: Explore available riders (add-ons) like accelerated death benefit riders (allowing you to access a portion of the death benefit if you become terminally ill) or waiver of premium riders (waiving premiums if you become disabled). These can add significant value.

Ultimately, the goal is to find a policy that fits your budget and provides adequate protection without unnecessary hurdles. It’s about smart choices, not just quick ones. Don’t let the allure of speed overshadow the need for comprehensive coverage.

Frequently Asked Questions About No Medical Exam Term Life Insurance

Are no medical exam policies always more expensive than traditional ones?

Not always. While some can be slightly higher, the difference might be minimal, especially if you’re generally healthy. For some, the cost of convenience is negligible, and they still find cheap no medical exam life insurance that suits their budget. It really depends on your individual health profile and the specific insurer.

How quickly can I get approved for no medical exam life insurance?

Often, very quickly! Many simplified issue policies offer approvals in minutes to a few days. Guaranteed issue policies are almost instant. The speed is one of the main advantages, helping you secure coverage faster than traditional methods.

What’s the difference between simplified issue and guaranteed issue?

Simplified issue involves answering a few health questions but no medical exam, and is for generally healthier individuals. Guaranteed issue requires no health questions or exam, and is for those with significant health concerns, often with higher premiums, lower coverage, and a waiting period before full benefits pay out.

Can I still get cheap no medical exam life insurance if I have health issues?

It depends on the severity of your health issues. If they’re minor, you might still qualify for simplified issue with competitive rates. For more serious conditions, guaranteed issue is an option, but it will generally be more expensive and offer less coverage. Speaking with an independent agent can help you navigate these nuances.

Where can I compare no medical exam term life insurance USA options?

You can compare options through online insurance marketplaces, directly on individual insurer websites, or by working with an independent insurance agent. Shopping around is crucial to finding the best rates and features for your specific needs, particularly when seeking no medical exam term life insurance USA cheap options.

So, there you have it. The world of no medical exam term life insurance USA cheap isn’t a myth; it’s a growing segment of the market designed for convenience and speed. By understanding your options, asking the right questions, and doing a bit of smart shopping, you can secure the vital protection your loved ones deserve without the usual hoops and hurdles. Take that first step towards peace of mind today. Your future self, and your family, will thank you for it. For more general insurance insights, feel free to explore our main insurance hub .