Alright, let’s talk about something incredibly important yet often overlooked: joint life insurance policy UK comparison . If you’re a couple, whether married, in a civil partnership, or just building a life together, this isn’t just another financial product; it’s a bedrock of security for your shared future. But here’s the thing, and let’s be honest, the UK insurance market can feel like a labyrinth, especially when you’re trying to figure out the best joint life insurance UK for your unique situation. It’s not just about getting any policy; it’s about getting the right one.

I’ve seen countless couples make common mistakes when trying to compare joint life policies – from overlooking crucial clauses to misunderstanding the fundamental differences between policy types. My goal today isn’t just to explain what joint life insurance is, but to guide you, step-by-step, through the process of comparing policies so you can avoid those pitfalls and secure the peace of mind you deserve. Think of me as your personal guide, helping you cut through the jargon and make truly informed decisions.

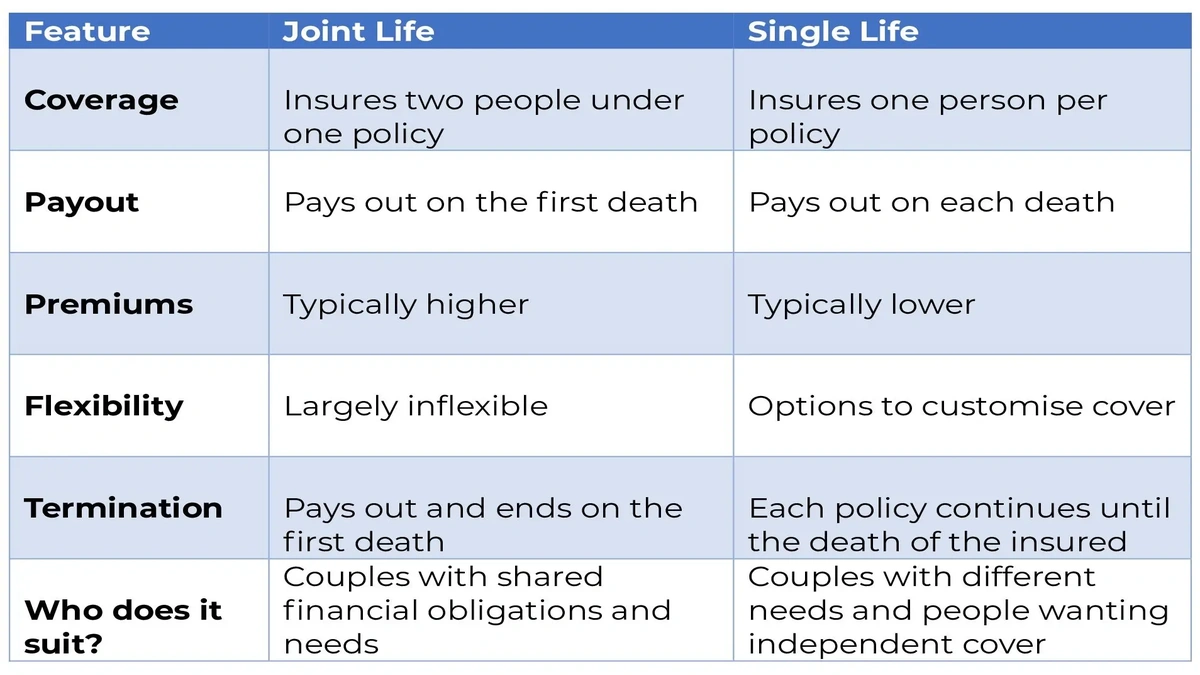

Understanding the Basics | First-Death vs. Second-Death Policies

Before we dive deep into the comparison, we need to clarify a foundational concept that trips up many: the difference between first-death policy and second-death policy . This isn’t just semantics; it fundamentally changes how and when a payout occurs, and therefore, what kind of financial protection it offers. It’s a key element in any effective joint life insurance policy UK comparison .

First-Death Policies (Joint Life, First Event): This is the most common type of joint policy. It pays out a lump sum upon the death of the first person on the policy. Once the payout is made, the policy ends. The remaining partner receives the funds, which can be crucial for covering immediate expenses like outstanding mortgage payments, debts, or daily living costs. It’s designed to protect the surviving partner financially. For many couples, especially those with a shared mortgage or young children, this is the go-to option.

Second-Death Policies (Joint Life, Second Event): Far less common for general family protection, a second-death policy only pays out upon the death of the second person on the policy. This means there’s no payout when the first partner passes away. So, who is this for? Typically, it’s used for inheritance tax planning. If you want to ensure your beneficiaries receive a tax-efficient lump sum after both partners have passed, this could be an option. However, for immediate financial support for a surviving partner, it offers no benefit.

When you’re looking at various providers, always, always clarify which type of policy they are quoting. A simple misunderstanding here can have significant implications for your financial planning. Remember, the core purpose of a life insurance for couples is to provide a safety net, and knowing when that net deploys is paramount.

Decoding Policy Types | Level Term vs. Decreasing Term Joint Cover

Once you’ve got your head around first-death versus second-death, the next big decision in your joint life insurance policy UK comparison journey is choosing between level term joint cover and decreasing term joint cover . These terms might sound a bit dry, but they describe policies designed for very different financial needs.

Level Term Joint Cover: With a level term policy, the payout amount remains the same throughout the entire policy term. So, if you take out a £200,000 policy for 20 years, it will pay out £200,000 whether you claim in year 1 or year 19. This type of cover is ideal if you have financial commitments that won’t reduce over time, such as providing for your children’s upbringing, covering living expenses, or leaving a specific inheritance. The consistency offers a straightforward sense of security.

Decreasing Term Joint Cover: As the name suggests, the payout amount with a decreasing term policy reduces over the policy term. This type of insurance is most commonly linked to a repayment mortgage, hence its other common name: joint mortgage protection insurance . As your mortgage balance decreases, so does the amount of cover. It’s usually the most cost-effective option if your primary concern is ensuring your mortgage is paid off if one of you passes away. If you want to understand more about securing your home, you might find insights onhomeowners insurancehelpful, though the UK market has its own specifics.

The choice between these two largely depends on what you’re trying to protect. Are you looking to cover a static financial need, or a debt that diminishes over time? This choice will significantly impact the quotes you receive and the suitability of the policy.

Beyond the Basics | Critical Illness Cover Joint and Single vs. Joint Decisions

When you’re deep into a joint life insurance policy UK comparison , it’s easy to get tunnel vision on just the life cover aspect. But many providers offer additional benefits, and one that absolutely deserves your attention is critical illness cover joint . This add-on pays out a lump sum if either policyholder is diagnosed with a specified critical illness (like cancer, heart attack, or stroke) during the policy term. This money can be invaluable for covering medical costs, adapting your home, or simply providing financial breathing room if you can’t work.

Now, let’s tackle a question that often pops up: is it better to get a single vs joint life insurance policy? This isn’t a one-size-fits-all answer. While a joint policy is often cheaper than two separate single policies, it typically only pays out once (on first death). If both partners were to pass away in a short period, a single first-death policy would only pay out once, leaving potentially less for beneficiaries than if you had two separate single policies. The trade-off is cost versus multiple payouts. For some, the simplicity and lower premiums of a joint policy are appealing. For others, particularly those with complex financial situations or higher desired payouts, two separate policies might offer more flexibility and comprehensive cover.

It’s worth considering your long-term needs. Do you anticipate needing separate cover down the line for different reasons, or is the shared protection of a joint policy sufficient? This decision should be made with a clear understanding of your financial goals and potential future scenarios. For broader family protection, you might also consider how this fits into your overallfamily health insurance plans, ensuring a holistic approach to your family’s well-being.

Key Factors in Your Joint Life Insurance Policy UK Comparison

So, you’ve got the types down. Now, how do you actually compare? Here’s my practical guide:

- Your Needs First: Before you even look at a quote, sit down with your partner and list what you want the insurance to cover. Is it just the mortgage? Protecting your children’s future? Covering funeral costs? This clarity is your compass.

- Policy Term: How long do you need the cover for? Until your mortgage is paid off? Until your children are financially independent?

- Sum Assured: How much cover do you need? A common rule of thumb is 10-15 times the main income, but this needs to be tailored to your specific debts, income, and dependents.

- Cost of Joint Life Insurance: Naturally, premiums are a huge factor. These are influenced by your age, health, lifestyle (smoking, drinking), occupation, the policy type, and the sum assured. Don’t just go for the cheapest; ensure it meets your needs. According to MoneyHelper, it’s vital to compare multiple quotes to find value. MoneyHelper provides excellent, unbiased guidance on this.

- Underwriting Process: Some insurers are more stringent than others, especially if one partner has pre-existing health conditions. Be honest and thorough in your application; non-disclosure can invalidate a claim.

- Reviews and Reputation: Look at what existing customers say about the insurer’s claims process and customer service. A policy is only as good as its ability to pay out when you need it most.

Remember, this isn’t a race. Take your time, ask questions, and don’t feel pressured. The goal is to find the best joint life insurance UK that fits your family’s blueprint.

Frequently Asked Questions About Joint Life Insurance

FAQs on Joint Life Insurance in the UK

What happens to a joint life insurance policy if we separate?

If you separate, you generally have a few options. You can often assign the policy to one person, or you may be able to split it into two single policies (though this might depend on the insurer and the original terms). It’s crucial to contact your insurer immediately to discuss your options, as simply cancelling could leave you both unprotected.

Is joint life insurance cheaper than two single policies?

Typically, yes, a joint life insurance policy is often cheaper than buying two separate single policies because it usually only pays out once (on the first death). However, as discussed, two single policies offer the potential for two separate payouts, which might be preferable for some couples depending on their financial planning.

Can we add critical illness cover to an existing joint life policy?

It depends on your existing policy and insurer. Some policies allow you to add critical illness cover joint later, while others might require you to take out a new policy or a separate critical illness plan. It’s always best to check directly with your current provider.

What factors affect the cost of joint life insurance?

The cost of joint life insurance is influenced by several factors, including the age and health of both applicants, whether they smoke or drink, their occupation, the amount of cover requested (sum assured), and the length of the policy term. The type of policy (level term vs. decreasing term) also plays a significant role.

Do I need life insurance if I don’t have a mortgage?

Absolutely! While joint mortgage protection insurance is a common use, life insurance isn’t solely for mortgages. If you have dependents, other debts, or simply want to ensure your partner and family are financially secure if you’re no longer around, life insurance is vital. It covers everything from living expenses to children’s education and funeral costs.

How do I compare joint life policies effectively?

To effectively compare joint life policies, first, clearly define your needs (e.g., covering mortgage, family income). Then, compare quotes from multiple providers, paying close attention to the sum assured, policy term, whether it’s first-death or second-death, and any optional extras like critical illness cover. Don’t just focus on price; consider the insurer’s reputation and claims history too.

The Bottom Line | Securing Your Shared Future

Choosing the right joint life insurance policy UK comparison isn’t just a financial decision; it’s a profound act of love and responsibility. It’s about protecting the dreams you’re building together and ensuring that if the unthinkable happens, the surviving partner isn’t left in financial distress. By understanding the nuances of first-death vs. second-death, level vs. decreasing term, and carefully considering your individual circumstances, you’re not just buying a policy; you’re investing in peace of mind. Take the time, ask the hard questions, and choose wisely. Your shared future depends on it.