Let’s be honest, diving into the nitty-gritty of UK home insurance can feel like wading through treacle, right? You get your quotes, you pick a policy, and then you see this word: ‘excess’. And suddenly, that clear picture of protecting your home gets a little blurry. What on earth is it? More importantly, how does it actually affect you when you need to make a claim? I’ve seen countless policyholders scratch their heads over this, and frankly, it’s one of those things that can sting you if you don’t quite grasp it.

Here’s the thing: understanding your home insurance excess meaning UK explained isn’t just about ticking a box. It’s about being truly prepared, knowing what to expect, and ultimately, making smarter financial decisions for your most valuable asset. Think of me as your guide through this slightly confusing, but absolutely crucial, part of your insurance policy. We’re going to break down exactly how excess works, why it matters, and how you can manage it like a pro.

What Exactly Is Home Insurance Excess, Anyway?

Alright, let’s get straight to it. In simple terms, the excess is the amount of money you agree to pay towards any claim you make on your insurance policy. It’s your contribution to the cost of the repair or replacement before your insurer pays the rest. Imagine you have a claim for £1,000, and your excess is £250. You pay the £250, and your insurer covers the remaining £750. Simple, right?

But why does it exist? Well, insurers aren’t just trying to make things complicated, I promise. The excess serves a few key purposes. Firstly, it discourages small, frequent claims – because if every tiny scratch resulted in a claim, administrative costs would skyrocket, and premiums would follow suit. Secondly, it means you, the policyholder, have some ‘skin in the game’, encouraging a bit more care with your property. It’s a fundamental part of how what is excess in insurance UK works across the board, not just for homes.

I initially thought it was just a way for insurers to save money, but then I realised it’s also about balancing risk and keeping the overall cost of insurance down for everyone. It’s a mechanism designed to make the system more efficient. Without it, your annual premium would likely be much higher.

The Two Sides of the Coin | Compulsory vs. Voluntary Excess

Now, this is where it gets interesting, because not all excesses are created equal. You’ll typically encounter two main types when looking at UK home insurance:

Compulsory Excess | The Non-Negotiable Part

This is the amount set by your insurer that you must pay towards a claim. It’s non-negotiable, and you’ll see it clearly stated in your policy documents. It can vary depending on the type of claim. For example, claims related to subsidence, storm damage, or flooding often have a higher compulsory excess than, say, a claim for accidental damage. Why? Because these types of claims are generally more complex and costly to resolve. It’s just how the risk is assessed.

Voluntary Excess | Your Strategic Choice

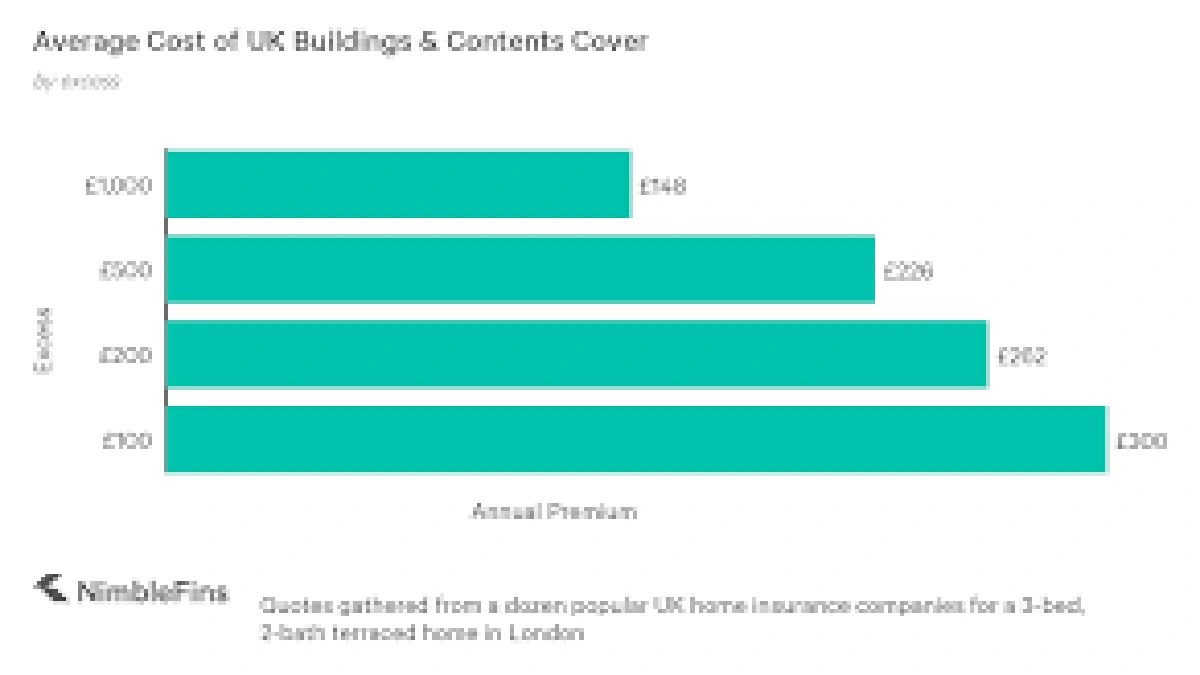

This is where you get a bit of control. The voluntary excess is an additional amount you agree to pay on top of the compulsory excess. So, if your compulsory excess is £100 and you choose a voluntary excess of £150, your total excess for a claim would be £250. The big incentive here? By agreeing to pay a higher voluntary excess, your annual premium typically goes down. It’s a trade-off. You save money upfront, but you commit to paying more if you need to make a claim. For those looking to understand broader insurance concepts, you might find similarities in other policy types, like howterm life insurance for seniors UKpolicies are structured around different coverage options.

This is a crucial decision point for homeowner responsibilities. Do you prefer lower monthly payments and are confident you won’t claim often? Or would you rather pay a bit more each month to have a lower payout if disaster strikes? It’s a personal financial choice, and there’s no universally ‘right’ answer. It depends entirely on your financial situation and your appetite for risk.

How Excess Impacts Your Home Insurance Claims (and Your Wallet)

Let’s talk about the moment of truth: making a claim. You’ve had a burst pipe, water damage to your ceiling – a nightmare, I know. You call your insurer, they assess the damage, and let’s say it comes to £3,000. If your total excess (compulsory + voluntary) is £350, you’ll pay that £350, and your insurer will pay the remaining £2,650. This is the essence of how home insurance claim excess works in practice.

But here’s a critical point many people overlook: what if your damage is only, say, £300, and your total excess is £350? In this scenario, it doesn’t make financial sense to make a claim. Why? Because the cost of the damage is less than your excess, meaning you’d pay for it all yourself anyway. Plus, even if no money is paid out by the insurer, simply making a claim can sometimes affect your future premiums and your no-claims discount.

This is where experience comes in. A common mistake I see people make is reflexively claiming for every small incident. Pause, assess the damage, and compare it to your total excess. Sometimes, it’s better to absorb the smaller costs yourself to protect your no-claims discount and keep future premiums down. It’s about strategic thinking, not just immediate relief. For more detailed insights into how excesses generally operate across various insurance products, MoneyHelper provides a fantastic resource onhow insurance excesses work.

Smart Strategies for Managing Your Excess

So, how do you find that sweet spot for your home insurance excess? It’s all about balance and understanding your own circumstances.

- Assess Your Risk Profile: Do you live in an area prone to flooding or subsidence? Is your home older and more susceptible to certain types of property damage? If your risk of claiming is higher, a lower voluntary excess (and thus a slightly higher premium) might give you more peace of mind.

- Review Your Finances: How much could you comfortably afford to pay out-of-pocket if you had to make a sudden claim? If a £500 excess would stretch your budget, then opting for a lower one, even with a higher premium, is probably the wiser choice. Don’t overcommit to a high voluntary excess just to save a few quid on your premium if you can’t actually afford it when it matters.

- Shop Around Annually: Don’t just auto-renew! Every year, compare quotes from different providers. Their compulsory excesses can vary, and you might find a better deal that aligns perfectly with your preferred voluntary excess. This is crucial for all types of insurance, much like understanding car insurance for bad credit drivers USA requires careful comparison.

- Understand Your Policy: Read the fine print! Seriously. Your insurance policy document will clearly lay out all excesses. Knowing this upfront will prevent nasty surprises down the line.

- Consider Your No-Claims Discount: If you’ve built up a significant no-claims discount, think twice before making a claim for minor property damage that’s only slightly above your excess. Sometimes, paying for smaller repairs yourself is the smarter long-term play.

Ultimately, managing your excess effectively means making an informed decision that balances your upfront costs (premium) with your potential costs at the time of a claim (excess). It’s not just about saving money today; it’s about financial resilience tomorrow.

FAQs | Your Burning Questions About Home Insurance Excess Answered

Can I choose not to pay excess?

No, not entirely. There will always be a compulsory excess set by your insurer. You can, however, choose your voluntary excess amount. If you opt for £0 voluntary excess, you’ll only pay the compulsory amount.

What if my claim is for less than my excess?

If the cost of the damage is less than your total excess, your insurer won’t pay anything, and you’ll cover the full cost yourself. In such cases, it’s often better not to officially make a claim to protect your no-claims discount.

Does excess apply to all types of claims?

Generally, yes, excess applies to most home insurance claims. However, the amount can vary significantly depending on the type of damage (e.g., standard accidental damage vs. flood or subsidence claims which often have higher compulsory excesses).

Will my excess change over time?

Your insurer might adjust the compulsory excess when your policy renews, especially if there have been changes in risk assessments or market conditions. Your chosen voluntary excess will remain as you set it unless you proactively change it.

What’s the best way to compare excess amounts?

When getting quotes, always look at the total excess (compulsory + voluntary) rather than just the voluntary amount. Use comparison websites and check the policy documents of direct insurers to get a clear picture.

So, there you have it. The home insurance excess meaning UK explained in a way that, I hope, feels a bit less like a mystery and more like a tool you can use. Don’t let the jargon intimidate you. By understanding these core principles, you’re not just buying insurance; you’re investing in peace of mind with open eyes. And that, my friend, is a powerful position to be in.