Alright, let’s talk about something that probably keeps you up at night, right after that looming calculus exam and the cost of your next coffee fix: car insurance. Specifically, finding the best car insurance for college students USA . It’s a beast, I know. You’re young, you’re in college, and insurers often look at you like you’re a ticking time bomb on wheels. But here’s the thing: it doesn’t have to be a budget-breaker. In fact, with the right strategy, you can find surprisinglyaffordable car insurancethat protects you without emptying your ramen fund. Think of me as your seasoned guide, navigating the labyrinth of policies and discounts, so you can get back to what really matters – acing your classes (or, you know, surviving them).

I’ve seen countless students grapple with this. They just accept the first sky-high quote, thinking there’s no way around it. But there is! This isn’t just about finding any policy; it’s about finding the smart policy. We’re going to dive deep into the ‘how-to’ of securing great college student car insurance, from understanding why rates are what they are, to uncovering those elusive discounts, and even figuring out if staying on your parents’ policy is the ultimate hack. Ready to become an insurance-savvy student? Let’s roll.

Understanding the Student Driver Landscape | Why It’s Tricky (and How to Navigate It)

First off, let’s address the elephant in the room: why are car insurance for young drivers rates so darn high? It’s simple, really, from an insurer’s perspective. Statistics, unfortunately, show that younger, less experienced drivers (especially those under 25) are statistically more likely to be involved in accidents. More accidents mean higher risk, and higher risk translates directly into higher premiums. It’s not personal, it’s just… data.

This is why student driver insurance rates can feel like a punch to the gut. Insurers use complex algorithms that factor in age, driving experience, vehicle type, location (are you in a bustling city or a quiet town?), and even your academic performance (more on that gem later!). But understanding this baseline helps us strategize. It means our goal isn’t just to find cheap insurance, but to find insurance that accurately reflects your actual risk profile, not just the generalized one for your age group.

A common mistake I see people make is assuming all policies are created equal. They’re not. Some companies are simply more student-friendly than others, offering specific programs or broader interpretations of what constitutes a ‘safe driver’ beyond just years on the road. The trick is knowing where to look and what questions to ask. It’s less about fighting the system and more about finding the system that works for you.

The Discount Deep Dive | Unlocking Hidden Savings for Students

This, my friends, is where the real magic happens. Discounts. They’re not just marketing fluff; they are legitimate ways to chip away at those hefty premiums. And for college students, there are some surprisingly accessible ones. Let’s break down the most impactful discounts for college students car insurance:

- The Good Student Discount: This is probably the most well-known, and for good reason. If you maintain a B average (or a 3.0 GPA), many insurers will give you a break. Why? Because studies suggest responsible students tend to be responsible drivers. So, those late nights studying aren’t just for your grades; they’re for your wallet too! Always ask your insurer about their specific GPA requirements.

- Away-From-Home Student Discount: Are you heading off to a university far from home, leaving your car behind? If you live more than a certain distance (often 100-150 miles) from your parents’ home and don’t regularly drive your car, your insurer might offer a significant discount. You’re still covered when you visit home, but your risk profile drops dramatically while you’re away. This is a huge one for many students.

- Telematics/Usage-Based Insurance: This is the future, folks. Companies like Progressive (Snapshot), State Farm (Drive Safe & Save), and Allstate (Drivewise) offer programs where a device (or an app on your phone) monitors your driving habits – things like braking, acceleration, mileage, and even the time of day you drive. If you’re a safe driver, you get rewarded with lower rates. It’s a fantastic option for students who might not drive much or who know they have excellent habits. It directly counters the ‘young driver = high risk’ stereotype.

- Driver Education/Defensive Driving Course Discount: Many states and insurers offer discounts if you complete an approved driver’s education course or a defensive driving program. It shows you’re committed to safe driving practices, which insurers love.

- Multi-Car/Multi-Policy Discounts: If your family has multiple cars insured with the same company, or if you bundle your car insurance with, say, renters insurance (which you absolutely should consider as a college student!), you can often get a discount. Always ask about bundling options.

- Vehicle Safety Features: Does your car have airbags, anti-lock brakes, anti-theft devices? These can all lead to small but cumulative savings.

Don’t be shy about asking for every single discount you might qualify for. Seriously, make a list and go through it with your agent. You’d be surprised what you can uncover when you’re proactive about student driver discounts.

Crafting Your Perfect Policy | Coverage That Makes Sense (and Saves Cents)

Beyond discounts, the type and amount of coverage you choose significantly impact your premium. This isn’t just about getting the cheapest option; it’s about getting the right coverage for your situation, especially when you’re looking for truly affordable student car insurance.

Let’s quickly review the main types:

- Liability Coverage: This is the bare minimum required by law in most states. It covers damages and injuries you cause to other people and their property. It doesn’t cover your own car or your own medical bills. While going with state minimums might seem like a way to save, it’s often a false economy. If you cause a serious accident, and the damages exceed your coverage limits, you’re personally on the hook for the rest. As a student, a hefty lawsuit is the last thing you need. I generally advise carrying more than the minimum, if your budget allows.

- Collision Coverage: This covers damage to your own car if you hit another vehicle or object (like a tree or pole). If you have an older car that isn’t worth much, you might consider dropping this to save money. But if you have a newer, more valuable car, it’s usually a must-have.

- Comprehensive Coverage: This covers damage to your car from things other than collisions – think theft, vandalism, fire, natural disasters (hail, floods), or hitting an animal. Again, for a newer car, it’s wise to have.

- Uninsured/Underinsured Motorist (UM/UIM): This is incredibly important. It protects you if you’re hit by a driver who either has no insurance or not enough insurance to cover your damages. Given the number of uninsured drivers out there, this is a coverage I highly recommend, especially for students who might not have a huge financial safety net.

When thinking about how to go about saving on car insurance, consider your deductible. This is the amount you pay out-of-pocket before your insurance kicks in. A higher deductible usually means a lower premium. Just make sure you can realistically afford to pay that deductible if you ever need to file a claim. It’s a balancing act: what can you comfortably pay now versus what can you comfortably pay if something goes wrong?

The Shopping Strategy | Comparing Quotes Like a Pro

Okay, you’ve armed yourself with knowledge about discounts and coverage. Now for the crucial step: actually getting quotes. This isn’t a one-and-done deal. You need to shop around, and you need to compare apples to apples.

Here’s my step-by-step guide:

- Gather Your Info: Have your driver’s license, vehicle information (make, model, VIN), academic transcripts (for that good student discount!), and current policy details (if you have one) handy. This makes the quoting process much faster.

- Check with Your Current Insurer (or Your Parents’): If you’re currently on your parents’ policy, start there. Ask them to get a quote for you as an individual, and also explore options for you remaining on their policy (especially if you’re an away-from-home student). Often, staying on a family policy is the most cost-effective route for insurance rates for college students.

- Get Multiple Quotes: Don’t just get one or two. Aim for at least 3-5 quotes from different types of insurers:

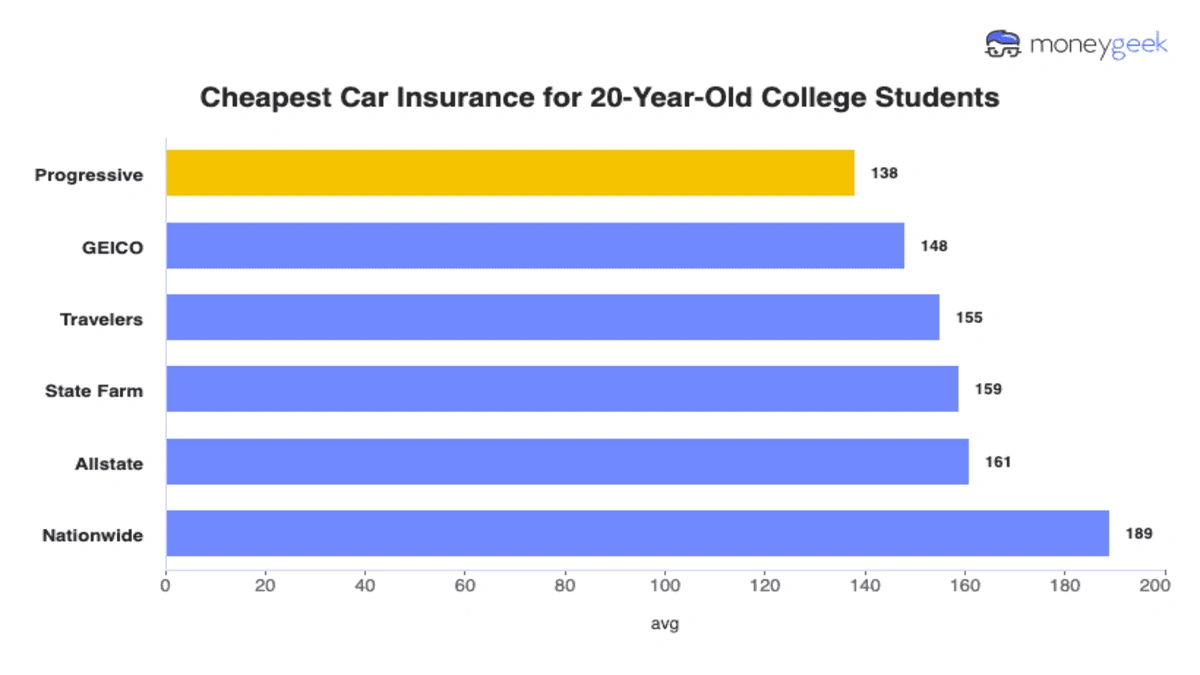

- Large National Carriers: Think State Farm, GEICO, Progressive, Allstate, Farmers, Liberty Mutual. They often have robust student programs and discounts.

- Regional Insurers: Depending on your state, there might be excellent local or regional companies that offer competitive car insurance for students.

- Independent Agents: These agents work with multiple insurance companies and can shop around for you, potentially finding deals you wouldn’t on your own. They’re like your personal insurance detective.

- Compare Policies Side-by-Side: This is critical. Don’t just look at the bottom-line price. Make sure you’re comparing policies with identical (or very similar) coverage limits, deductibles, and endorsements. A lower premium might mean significantly less coverage, which isn’t a smart saving in the long run. If you’re looking for more general insurance guidance, you can always check out resources like this site for various insurance tips.

- Ask About Payment Plans: Some insurers offer discounts if you pay your premium in full, or if you opt for automatic payments. Every little bit helps!

Remember, your goal is to find the best car insurance for college students USA that balances cost and adequate protection. It’s not just about the cheapest policy; it’s about the one that gives you peace of mind without breaking the bank.

Keeping Your Rates Low | Post-Purchase Pointers

Getting your policy is just the beginning! Maintaining low young drivers insurance rates requires ongoing effort. Here are some pro tips:

- Maintain a Clean Driving Record: This is paramount. Accidents and tickets will almost certainly raise your premiums. Drive safely, avoid distractions, and always follow traffic laws. It sounds obvious, but it’s the single biggest factor in long-term savings.

- Update Your Policy Annually (or Sooner): Life changes, especially in college. Did you move to a new dorm? Get better grades? Stop driving as much? These changes can impact your rates. Inform your insurer about significant life events.

- Re-evaluate Annually: Don’t just auto-renew without checking. Your circumstances change, and so do insurance companies’ offerings. Get new quotes every year or two, especially around renewal time. You might find a better deal with a different provider.

- Consider Your Vehicle: When it’s time for a new car (eventually!), remember that the type of car you drive affects your insurance. Generally, older, safer, less powerful, and less expensive-to-repair vehicles will have lower premiums.

- Build Good Credit: Believe it or not, your credit score can influence your insurance rates in many states. Start building good credit now (responsibly!) with a student credit card or by paying bills on time.

For more detailed information on car insurance regulations and consumer advice, you can always refer to official government resources, like theUSA.gov car insurance guide, which offers a wealth of impartial information.

Common Questions About Student Car Insurance

Can I stay on my parents’ policy?

Often, yes! In many cases, it’s actually cheaper for a college student to remain on their parents’ policy, especially if they are attending school away from home and not regularly driving the insured vehicle. Insurers often view a family policy as lower risk. Make sure your parents inform their insurer about your student status and location to explore applicable discounts like the ‘away-from-home student’ discount.

What if I don’t have a perfect GPA for the good student discount?

Don’t despair! While a 3.0 GPA or B average is common for a good student discount, some insurers might accept a slightly lower GPA or have other criteria. Always ask your specific insurer about their requirements. Even if you don’t qualify for this one, remember there are many other discounts available, like safe driver, multi-policy, or telematics programs, that can still significantly reduce your car insurance for college students costs.

Is it cheaper to get my own policy or stay on my parents’?

Generally, staying on your parents’ policy is more cost-effective. Insurers often offer better rates to multi-car, multi-driver households. However, there are exceptions. If you own your own car and live completely independently, or if your parents’ policy is exceptionally expensive, getting your own policy and leveraging all available student discounts might sometimes be competitive. It’s crucial to get quotes both ways and compare them directly, ensuring similar coverage levels.

What’s telematics and how can it help?

Telematics (or usage-based insurance) involves installing a small device in your car or using a smartphone app that monitors your driving habits – how fast you drive, how hard you brake, how quickly you accelerate, and how much you drive. If you demonstrate safe driving behaviors, the insurer rewards you with lower premiums. It’s a fantastic way for students who are responsible drivers to prove their low-risk status and get personalized, often significantly reduced, rates on their best car insurance deals.

And speaking of navigating complex financial landscapes, while we’re focused on car insurance, understanding various insurance options is a smart move for any student. For instance, if you’re ever curious about other insurance types, likeprivate health insurance UK cost per month, it highlights how diverse and specific insurance needs can be across different contexts and countries. It’s all part of becoming financially literate!

The Road Ahead | Drive Smart, Save Big

Finding the best car insurance for college students USA isn’t about luck; it’s about being informed, proactive, and a little bit savvy. You now have the blueprint: understand the landscape, aggressively seek out discounts, choose smart coverage, shop around diligently, and maintain excellent driving habits. This isn’t just about saving money now; it’s about setting yourself up for a lifetime of lower insurance rates for college students by building a responsible driving and financial history.

So, take a deep breath. You’ve got this. Go forth, compare those quotes, ask those questions, and drive safely. Your wallet (and your peace of mind) will thank you. Now, about that calculus homework…