Let’s be honest, when you think about your home, you probably imagine comfort, safety, and a place where memories are made. You definitely don’t want to think about it being swept away by a flood, shaken by an earthquake, or engulfed by a wildfire. But here’s the thing: in the USA, natural disasters aren’t just headlines anymore; they’re a growing reality for millions of homeowners. And what truly fascinates me (and frankly, keeps me up at night sometimes) is how many people assume their standard home insurance for natural disasters USA coverage has them totally protected. The stark reality? It often doesn’t. And understanding why that is, what those hidden gaps are, and what it means for your financial peace of mind, is absolutely crucial.

We’re not just talking about minor inconveniences here. We’re discussing life-altering events that can wipe out your biggest asset in an instant. So, let’s pull back the curtain and dive deep into the nuances of what your policy truly covers, what it definitely doesn’t, and why a little foresight now can save you a world of heartache later. This isn’t just about reading the fine print; it’s about understanding the evolving landscape of risk and how to navigate it smartly.

Beyond the Basics: What Standard Home Insurance Doesn’t Cover

Okay, so you’ve got a standard homeowners insurance policy – maybe an HO-3, which is pretty common. It covers things like fire, theft, liability, and usually damage from windstorms, hail, and even some snow. That feels comprehensive, right? Well, yes, for certain perils. But here’s where the plot thickens: most standard policies have specific, glaring `standard home insurance exclusions` when it comes to natural disasters. It’s not just an oversight; it’s a fundamental structural aspect of how these policies are designed.

The biggest exclusion? Floods. That’s right. If your basement fills with water because of a torrential downpour, or if a nearby river overflows its banks, your standard policy will likely offer zero protection. This is a common mistake I see people make, believing that because they have ‘water damage’ coverage, they’re safe from floods. Nope. It’s usually for things like a burst pipe, not rising outdoor water. Similarly, earthquakes are almost universally excluded. And in many regions, even damages from landslides or mudslides that aren’t directly linked to a covered peril (like a preceding wildfire) can be left out in the cold. It’s almost like the insurance companies are saying, “We’ll cover the usual suspects, but for the really big, catastrophic ones, you’ll need a special ticket.”

The Big Three | Flood, Earthquake, and Wildfire Insurance Explained

Since standard policies wave goodbye to many major natural disasters, let’s talk about the specific coverages you might need. These are often purchased as separate policies or endorsements, and they’re tailored to tackle the specific risks that keep people up at night.

Flood Insurance USA | More Than Just Rivers

If you live anywhere near water, or even in an area prone to heavy rainfall, you absolutely need to consider `flood insurance USA`. Most flood policies are backed by the National Flood Insurance Program (NFIP), managed by FEMA. You can buy it through private insurers, but the underlying coverage is often federal. What’s crucial to understand is that flood zones are constantly being updated, and even if you’re not in a ‘high-risk’ zone, a significant percentage of flood claims come from moderate-to-low risk areas. It’s not just about coastal surges or overflowing rivers; flash floods can happen anywhere. Learn more about flood risks and preparedness atFEMA’s official website.

Earthquake Insurance Coverage | Shaking Up Your Assumptions

For those in seismic zones – think California, but also parts of the Pacific Northwest, New Madrid fault line in the Midwest, and even some East Coast areas – `earthquake insurance coverage` is a non-negotiable conversation. This is almost always a separate policy or an endorsement. It often comes with a higher deductible, sometimes a percentage of your home’s value, which means you’ll pay a significant amount out-of-pocket before coverage kicks in. But when you consider the potential structural damage an earthquake can inflict, it’s a small price to pay for peace of mind.

Wildfire Insurance Plans | A Blazing Hot Topic

In states like California, Oregon, and Colorado, `wildfire insurance plans` have become incredibly difficult and expensive to secure. As wildfires intensify and spread, some insurers are pulling out of high-risk areas entirely. If you live in a wildland-urban interface (WUI), you’re likely facing higher premiums, stricter underwriting, or even needing to resort to state-backed ‘insurers of last resort.’ This isn’t just about your home burning; it’s about smoke damage, ash contamination, and even the cost of rebuilding in a post-disaster zone. It’s a stark reminder that climate change isn’t just an abstract concept; it’s directly impacting your ability to protect your home.

And let’s not forget `hurricane damage home insurance` for our friends along the Gulf and Atlantic coasts. This often involves separate windstorm deductibles, which can be a percentage of your dwelling coverage, leading to substantial out-of-pocket costs after a major storm. The complexity here underscores why understanding your specific regional risks is paramount.

Navigating Deductibles and Payouts | The Fine Print That Matters

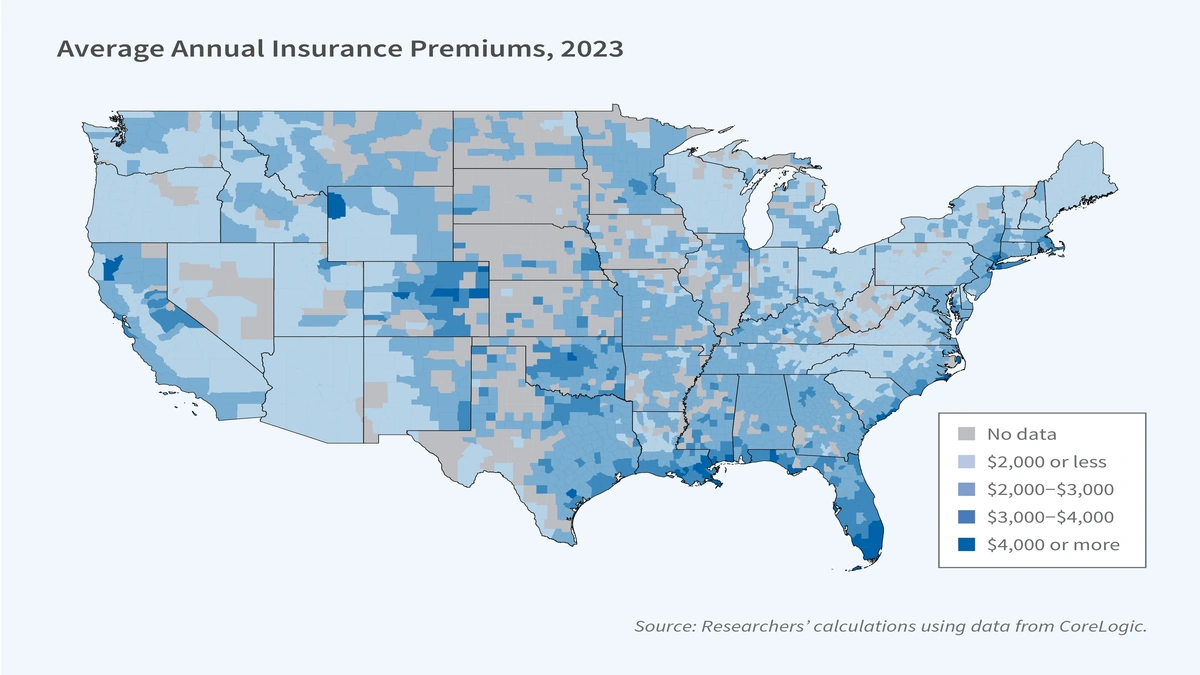

So, you’ve got your specialized policies. Great! But now we need to talk about the actual mechanics of when they kick in: `deductibles for natural disaster claims`. Unlike your standard $500 or $1,000 deductible for a minor claim, natural disaster deductibles can be much higher. For flood and earthquake insurance, they are often a percentage of your dwelling coverage, say 5% or 10%. On a $400,000 home, a 5% deductible is $20,000. That’s a significant chunk of change to have readily available during an emergency.

Understanding these `understanding deductibles` is critical. It impacts your out-of-pocket exposure and should influence how much you save in your emergency fund. Moreover, the `insurance claims process` after a widespread disaster can be slow and arduous. Insurers are swamped, adjusters are stretched thin, and getting your claim processed can take months. This is where meticulous documentation of your property and possessions (before disaster strikes) becomes invaluable. The `cost of natural disaster insurance` isn’t just the premium; it’s also the potential deductible you’ll pay and the time/effort involved in the recovery.

Why Location is Everything | Regional Risks and Your Policy

It sounds obvious, but your geographic location dictates almost everything about your `home insurance for natural disasters USA coverage`. A homeowner in Kansas is worried about tornadoes; someone in Florida about hurricanes; Californians about earthquakes and wildfires. This isn’t just about what you should buy, but what’s available and at what price.

In high-risk areas, insurers are conducting more intensive `risk assessment for homeowners`. They’re looking at everything from your home’s proximity to brush in wildfire zones, to its elevation in flood plains, to its construction materials in earthquake-prone regions. This means premiums can vary wildly, and sometimes, coverage can be hard to get or prohibitively expensive. This is why comparing options isn’t just smart; it’s essential. Just like you mightcompare car insurance prices, you should apply the same diligence to your home coverage, especially for catastrophic events.

Preparing for the Unthinkable | Beyond Just Insurance

While insurance is a cornerstone of `natural disaster preparedness`, it’s not the only piece of the puzzle. Beyond the financial safety net, there are tangible steps you can take to mitigate risk and ensure your family’s safety. This includes creating a family emergency plan, having an evacuation kit ready, reinforcing your home against specific local threats (e.g., hurricane shutters, defensible space for wildfires), and keeping vital documents secure and accessible.

Also, understand that if a disaster is truly catastrophic and widespread, `federal disaster assistance` might become available. However, this is usually a last resort, often in the form of low-interest loans, and it’s not a substitute for robust insurance coverage. It’s a safety net, not a primary solution. Think of it like this: just as you’d plan for your long-term financial security withterm life insurance plans, you need to proactively plan for your home’s immediate future against natural threats.

Frequently Asked Questions About Natural Disaster Home Insurance

What exactly is considered a ‘natural disaster’ by insurance companies?

Generally, insurance companies define natural disasters as events caused by natural forces, like floods, earthquakes, hurricanes, tornadoes, and wildfires. However, what’s covered under your standard policy versus requiring separate coverage (like flood or earthquake insurance) varies significantly. It’s crucial to check your specific policy’s exclusions.

Can I get home insurance if I live in a very high-risk area?

It can be challenging, but often yes. Insurers might offer coverage at higher premiums, or with higher deductibles. In some states, ‘insurers of last resort’ or state-backed programs exist to ensure homeowners in high-risk zones can still get coverage, albeit often with more limited options.

How do I know if my area is prone to specific natural disasters?

You can check resources like FEMA’s flood maps, USGS for seismic activity, and local government websites for wildfire risk assessments. Your insurance agent can also provide valuable insights into regional risks and recommended coverages.

Is federal disaster assistance the same as flood insurance?

No, they are very different. Flood insurance is a policy you purchase that pays out directly for covered damages. Federal disaster assistance, often from FEMA, is typically activated after a major disaster declaration and usually comes in the form of low-interest loans or grants for specific needs, not a full replacement of your home’s value.

What’s the difference between a deductible and a percentage deductible?

A standard deductible is a fixed dollar amount (e.g., $1,000) you pay before your insurance covers the rest. A percentage deductible (common for natural disasters like hurricanes or earthquakes) is a percentage of your home’s insured value (e.g., 5% of a $300,000 home means a $15,000 deductible).

The Bottom Line | Don’t Get Caught Unprepared

The bottom line here is simple, yet profound: assuming your standard `home insurance for natural disasters USA coverage` is all you need is a dangerous gamble. The landscape of natural disasters is changing, and with it, the complexities of protecting your most valuable asset. Take the time to understand your risks, scrutinize your current policies, and explore supplemental coverages like flood, earthquake, or specialized wildfire plans. It might seem like a hassle now, but when the unthinkable happens, being prepared isn’t just about money; it’s about rebuilding your life with dignity and peace of mind. Don’t wait for disaster to strike to realize you had a hidden gap. Be proactive, be informed, and protect what truly matters.