Let’s be honest, if you’re a smoker in the USA, the phrase “affordable life insurance” probably sounds like a cruel joke, right? Most people assume that once you light up, you’re automatically condemned to sky-high premiums, making crucial financial protection feel utterly out of reach. But here’s the thing: that’s not always the full picture. While yes, smoking does impact your rates, it doesn’t automatically mean you’re locked out of findinggreat coverageat a manageable cost. My goal today is to guide you through the maze, showing you exactly how to navigate the system and uncover the best life insurance for smokers USA low cost options that genuinely exist.

I’ve seen countless individuals, just like you, feel frustrated and defeated before even starting their search. The good news? With the right strategy and a bit of insider knowledge, securing affordable life insurance for smokers is more achievable than you might think. We’re going to dig deep into the nuances, look at the specific options, and equip you with the know-how to make an informed decision. Forget the generic advice; we’re talking about actionable steps to save you money and give you peace of mind.

Understanding Smoker Classifications | It’s Not Always Black and White

One of the biggest misconceptions I encounter is that all smokers are painted with the same broad brush. Insurers, surprisingly, are a bit more nuanced than that. While smoking undoubtedly increases health risks, leading to higher smoker life insurance rates, the way they classify you can significantly impact your premium. This is where understandingsmoker classificationsbecomes your secret weapon.

Typically, insurers categorize applicants into various health classes, and smoking status is a major factor. You might hear terms like ‘Preferred Smoker,’ ‘Standard Smoker,’ or even ‘Table-Rated Smoker.’ A ‘Preferred Smoker’ might be someone who smokes occasionally but is otherwise in excellent health, with no other risk factors. A ‘Standard Smoker,’ on the other hand, might smoke regularly and have a few minor health issues. The key takeaway? Even within the ‘smoker’ category, there’s a spectrum, and your overall health, age, and even the type of tobacco product you use (cigarettes vs. occasional cigar) can play a role.

But what if you’ve recently quit? This is where things get really interesting. Many policies offer better rates for ‘former smokers,’ but there’s usually a waiting period, often 12 months or even 2-5 years, where you must be completely tobacco-free to qualify for non-smoker rates. So, if you’re considering quitting, know that it could significantly reduce your life insurance for smokers costs down the line. It’s a powerful incentive, isn’t it?

The Smart Shopper’s Guide to Lowering Your Smoker Life Insurance Rates

Alright, so you’re a smoker, and you need life insurance. How do you find those elusive low-cost life insurance for smokers options? It’s less about magic and more about methodical shopping. Think of it like this: you wouldn’t buy the first car you see, right? The same principle applies here.

- Shop Around, Seriously: This is the absolute golden rule. Every insurer has its own underwriting guidelines and risk assessments. What one company considers a high risk, another might view more favorably. Getting multiple quotes (at least 5-7) from different providers is non-negotiable. Don’t just settle for the first offer you receive; there’s often a better deal out there.

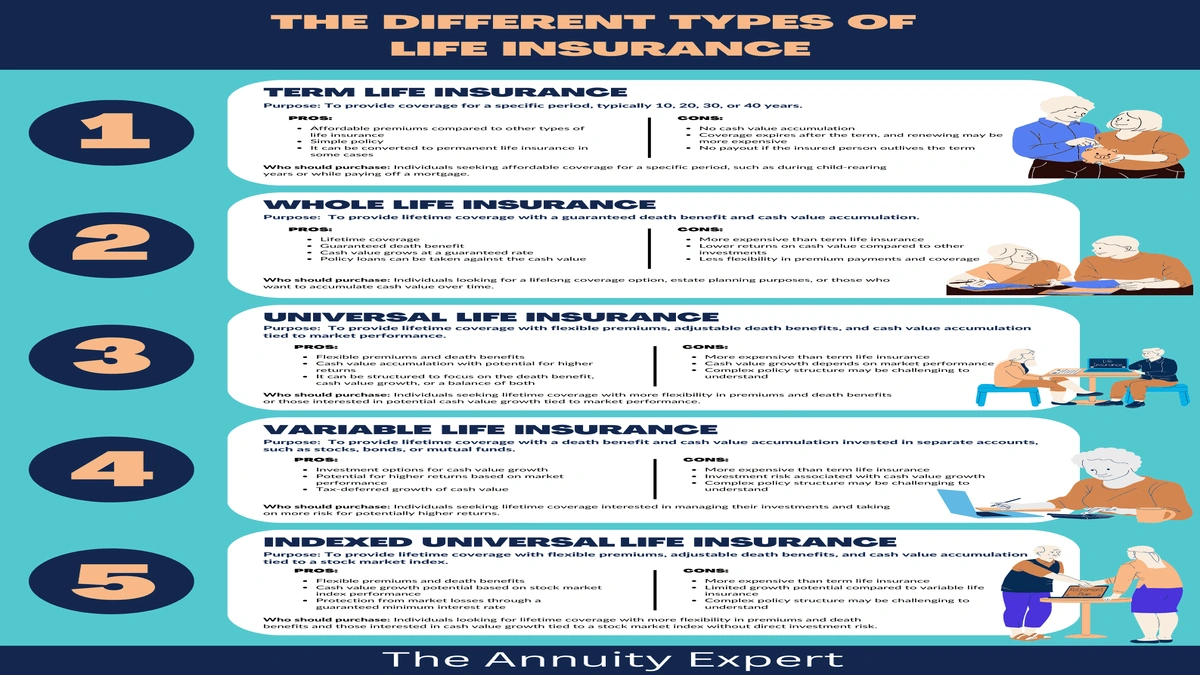

- Consider Term Life Insurance for Smokers: For many, term life insurance for smokers is the most cost-effective solution. Unlike whole life insurance, which covers you for your entire life and builds cash value, term life covers you for a specific period (e.g., 10, 20, or 30 years). This focus on a defined period often translates to significantly lower premiums, making it a popular choice for those seeking the best life insurance for smokers USA low cost options. It’s a straightforward way to protect your dependents during your prime earning years.

- Be Honest, Always: It might be tempting to downplay your smoking habits, but don’t. Misrepresenting your smoking status on an application is considered fraud and can lead to your policy being canceled or a claim being denied when your family needs it most. Honesty is not just the best policy; it’s the only policy.

- The Power of Quitting: As mentioned, becoming a ‘former smoker’ is a game-changer. Even if you’ve only recently quit, some insurers might offer a ‘smoker plus’ rate, which is better than a full smoker rate, with the promise of a re-evaluation for non-smoker rates after a specific period of being tobacco-free. This is a real pathway to dramatically reducing your smoker life insurance rates.

- Improve Overall Health: Beyond smoking, your general health matters. Losing weight, managing blood pressure, and controlling cholesterol can all contribute to a better health classification, even as a smoker. Every little bit helps in the insurer’s eyes.

Exploring “No Medical Exam” and “Guaranteed Issue” Options for Smokers

When the standard underwriting process seems daunting, or if you have significant health concerns alongside smoking, you might stumble upon “no medical exam” or “guaranteed issue” life insurance. These sound appealing, especially for finding best life insurance for smokers USA low cost, but let me rephrase that for clarity: they come with trade-offs you absolutely need to understand.

No Medical Exam Life Insurance Smokers: These policies allow you to skip the physical exam, often relying on a health questionnaire and database checks. While convenient, they usually come with higher premiums than fully underwritten policies, even for non-smokers. For smokers, the rates can be significantly elevated, and the coverage amounts are often lower. They can be a good option if you need coverage quickly or if you have minor health issues that might complicate a traditional exam, but they are rarely the lowest cost option available.

Guaranteed Issue Life Insurance for Smokers: This is exactly what it sounds like: guaranteed acceptance, regardless of your health history or smoking status. No medical questions, no exam. This sounds like a dream for those who struggle to get coverage elsewhere. However, these policies typically have the highest premiums, very limited coverage amounts (often $5,000-$25,000), and a waiting period (usually 2-3 years) before the full death benefit pays out. If you die during this waiting period, your beneficiaries might only receive a refund of premiums paid plus interest. They are truly a last resort, designed for individuals who cannot qualify for any other type of policy for smokers due to severe health issues.

What fascinates me about these options is how they fill a critical gap, even if they aren’t the cheapest. They ensure that even the highest-risk individuals can secure some form of protection, emphasizing that some coverage is always better than none. But if you’re specifically targeting low-cost life insurance for smokers, these are generally not your primary hunting ground.

Beyond the Premium | What Else to Consider When Buying Life Insurance

While finding the best life insurance for smokers USA low cost is your main goal, remember that the lowest premium isn’t always the best value. There are other crucial factors to weigh in your decision-making process. I initially thought this was straightforward, but then I realized how many people overlook these critical details.

- Company Reputation and Financial Strength: This is paramount. A life insurance policy is a long-term commitment. You want to ensure the company will be around and able to pay out claims decades from now. Check ratings from independent agencies like A.M. Best, Standard & Poor’s, and Moody’s.

- Policy Features and Riders: Does the policy offer any valuable riders? These are add-ons that can enhance your coverage. For example, an accelerated death benefit rider allows you to access a portion of your death benefit early if you become terminally ill. A conversion rider on a term policy lets you convert it to a permanent policy later without a new medical exam, which could be invaluable if you quit smoking and want to lock in better rates.

- Customer Service: You might need to interact with your insurer over the years. Good customer service can make a world of difference when you have questions or need to make changes.

- Review and Re-evaluate: Your life changes, and so should your insurance. If you quit smoking, get healthier, or even if your financial needs shift, don’t be afraid to revisit your policy. You might qualify for better rates or need more or less coverage. It’s part of smart financial planning, just like you’d periodically assess your property insurance needs.

Frequently Asked Questions About Life Insurance for Smokers

Can I get affordable life insurance if I smoke?

Yes, absolutely! While smoking generally leads to higher premiums, it’s entirely possible to find affordable life insurance for smokers in the USA. The key is to shop around extensively, compare quotes from multiple providers, and understand the nuances of smoker classifications. Don’t assume it’s out of reach.

What if I quit smoking after getting a policy?

This is great news! If you quit smoking after your policy is issued, you can typically request a re-evaluation of your rates after a certain period (often 12 months, but check with your insurer). Many companies will reduce your premiums to non-smoker rates once you meet their criteria for being tobacco-free. This is a significant incentive for quit smoking life insurance seekers.

Is “no medical exam” life insurance always more expensive for smokers?

Generally, yes. While convenient, no medical exam life insurance smokers policies tend to have higher premiums than fully underwritten policies, where you undergo a medical exam. This is because the insurer takes on more risk without a full health assessment. They might be a good option if you need quick coverage or have minor health issues, but they’re usually not the cheapest route.

How long do I have to be smoke-free to get non-smoker rates?

The required period varies by insurer, but it’s typically between 12 months and 5 years. Most commonly, you’ll need to be tobacco-free for at least 12 consecutive months to qualify for preferred non-smoker rates, with some companies requiring longer periods for the absolute best rates. Always confirm the specific requirements with your chosen insurer.

What types of life insurance are best for smokers?

For most smokers seeking low-cost life insurance, term life insurance is often the most suitable option due to its affordability and straightforward nature. It provides coverage for a specific period, making it ideal for protecting your family during critical years. If traditional policies are difficult to obtain due to severe health issues, guaranteed issue policies might be considered as a last resort, though they come with higher costs and lower coverage.

So, there you have it. The notion that finding best life insurance for smokers USA low cost is impossible is, frankly, outdated. It takes a little more legwork, a deeper understanding of how insurers operate, and a willingness to explore all your options. But with this guide in hand, you’re now equipped to approach the market with confidence, armed with the knowledge to secure the protection your family deserves without feeling like you’re being penalized for your habits. Go forth, compare, and protect your future!