Let’s be honest, the phrase “ cheap full coverage car insurance USA ” often feels like a cruel joke, doesn’t it? It’s like searching for a unicorn that also bakes artisanal sourdough. We all know we need robust protection on the roads, especially with the sheer number of vehicles out there, but the thought of those soaring premiums can make anyone wince. What if I told you that finding genuinely affordable car insurance isn’t just a pipe dream? It requires a bit of savvy, a dash of strategy, and knowing exactly where to look. And trust me, I’ve seen enough policies and premium breakdowns to tell you that there are real, actionable ways to cut down those costs without sacrificing the peace of mind that full coverage brings.

Here’s the thing: most people just accept the first or second quote they get, or worse, they stick with the same insurer for years, assuming loyalty will pay off. Sometimes it does, but often, you’re leaving money on the table. My goal today is to walk you through the often-overlooked tactics and insider tips that can significantly reduce your auto insurance premiums. We’re going to demystify what “full coverage” really means, explore the hidden discounts, and arm you with the knowledge to confidently negotiate for the best car insurance deals out there. Ready to save some serious cash? Let’s dive in.

Decoding “Full Coverage” | What Are You Really Paying For?

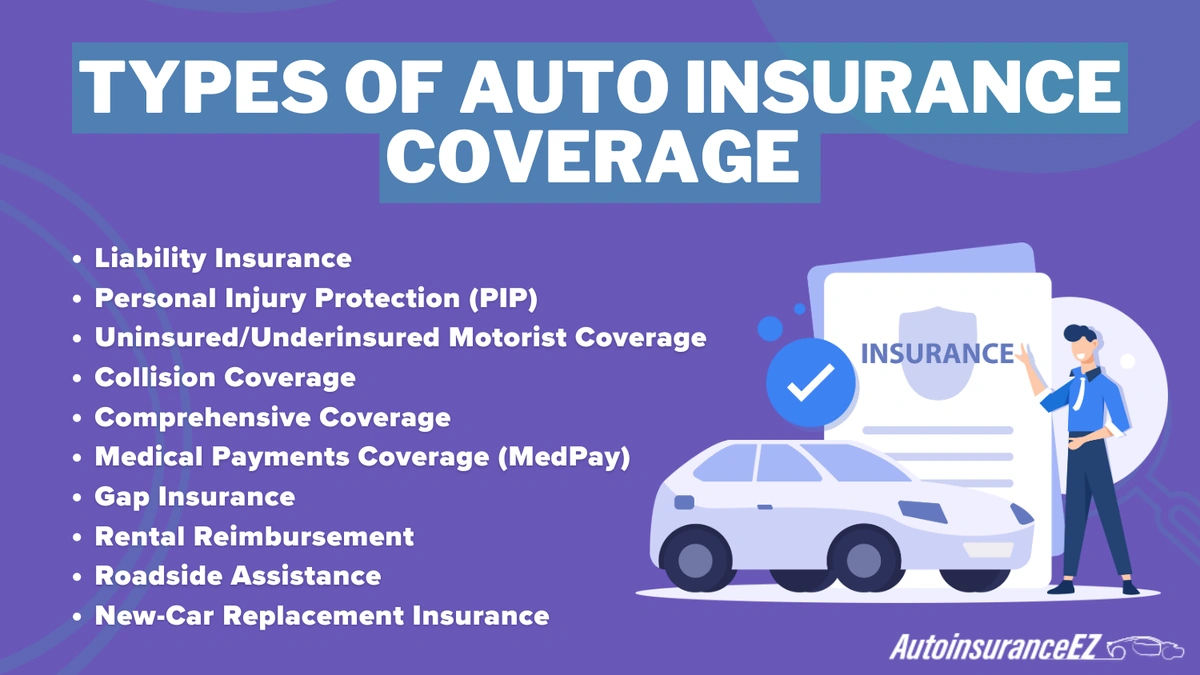

Before we even talk about finding it cheap, let’s get on the same page about what “full coverage” actually entails. Because, surprisingly, it’s not a single policy type you can just tick a box for. When people say full coverage, they’re generally referring to a combination of several key components:

- Liability Coverage: This is the bare minimum, legally required in almost every state. It covers damages (both bodily injury and property damage) you might cause to other drivers, passengers, or property in an at-fault accident. It doesn’t cover your own car or injuries.

- Collision Coverage: This is where your own vehicle gets protection. If you hit another car, a pole, or even roll your car, collision coverage helps pay for the repairs to your vehicle, regardless of who was at fault. This is a big one for peace of mind.

- Comprehensive Coverage: Think of this as protection against everything but a collision. We’re talking theft, vandalism, fire, natural disasters (like hail or floods), and even hitting an animal. If a tree branch falls on your car while it’s parked, comprehensive has your back.

Often, people also include Uninsured/Underinsured Motorist Coverage and Medical Payments/Personal Injury Protection (PIP) in their definition of “full coverage,” and for good reason. These add crucial layers of protection against drivers who don’t have enough insurance (or any at all) or help cover medical bills after an accident. Understanding these components is your first step to getting a customized insurance plan that fits your needs without overpaying for what you don’t require.

The Under-the-Radar Strategies to Slash Your Premiums

Alright, now for the fun part: how to actually lower those numbers. I’ve seen countless folks miss out on significant savings because they simply weren’t aware of the myriad of discounts available. This isn’t just about finding cheap full coverage car insurance USA; it’s about smart financial planning.

- Bundle Up: This is probably the easiest win. Most insurers offer substantial discounts if you combine your auto policy with home, renters, or even health insurance for your family . It’s a win-win: the company gets more of your business, and you get a break on your premiums.

- Drive Smart, Save More: Good driver discounts are common, but many companies now offer telematics programs. You install a device or use an app that monitors your driving habits (speed, braking, mileage). Drive safely, and you could see a noticeable drop in your rates.

- Low Mileage Discount: Not commuting much? Working from home? If you drive fewer miles than the average person, make sure your insurer knows. Less time on the road generally means less risk.

- Good Student Discount: Got a young driver in the family with good grades? Many insurers reward academic excellence with discounts, especially for those under 25.

- Credit Score Matters (Mostly): In many states, your credit score plays a significant role in determining your vehicle insurance rates. Insurers see a correlation between creditworthiness and claims history. Improving your credit can genuinely lead to lower premiums over time. (Note: California, Hawaii, and Massachusetts prohibit the use of credit scores in setting insurance rates.)

- Vehicle Choice: The type of car you drive makes a huge difference. High-performance sports cars or vehicles with a high theft rate will naturally cost more to insure. Opting for a car with excellent safety ratings and lower repair costs can be a wise long-term strategy for reducing car insurance costs.

These aren’t just minor adjustments; implementing a few of these can make a dramatic impact on your annual outlay. It’s about being proactive and understanding the levers you can pull.

Your Step-by-Step Guide to Comparing and Saving

This is where the rubber meets the road. Simply knowing about discounts isn’t enough; you need to actively seek out the best deals. The internet has made this incredibly easy, and ignoring these tools is like leaving money on the table. When you’re ready to compare car insurance quotes, here’s how to approach it:

- Gather Your Information: Have your current policy details, vehicle information (VIN, make, model, year), driving history, and personal details (address, age, occupation) ready. The more accurate your info, the more accurate your quotes will be.

- Leverage Online Comparison Tools: Websites like Policygenius, The Zebra, or even direct insurer sites allow you to input your information once and get multiple quotes from different providers. This is a game-changer for finding online insurance comparison tools that save you time and effort. Don’t be afraid to try a couple of different ones to cast a wide net.

- Don’t Just Look at the Bottom Line: While a low premium is great, always compare apples to apples. Check the coverage limits, deductibles, and any exclusions. A super cheap policy with high deductibles might not be the best deal if a small fender bender costs you a fortune out of pocket.

- Call an Independent Agent: Sometimes, the best deals aren’t found solely online. Independent insurance agents work with multiple companies and can often find insurance policy options and discounts you might miss. They can be invaluable for personalized advice, especially if your situation is unique.

- Review Annually (or When Life Changes): Your life isn’t static, and neither should your policy be. Get new quotes at least once a year. Also, significant life events – buying a new car, moving, getting married, improving your credit score, or even a child getting their license – are prime opportunities to revisit your policy and potentially find better rates.

Remember, the goal isn’t just to find any cheap policy, but the right cheap full coverage car insurance USA policy that offers robust protection at a price you can comfortably afford. This proactive approach is key to consistently saving money on auto insurance.

Beyond the Obvious | Long-Term Habits for Affordable Car Insurance

Finding a great rate now is fantastic, but maintaining it (or even lowering it further) requires some consistent effort. Think of it as cultivating good financial health for your vehicle. What fascinates me is how many people overlook the cumulative effect of small, consistent actions.

- Maintain a Spotless Driving Record: This is, without a doubt, the most impactful long-term strategy. Accidents and moving violations directly translate to higher premiums. Drive defensively, avoid distractions, and those vehicle insurance rates will thank you.

- Regular Policy Reviews: As I mentioned, life changes. So do insurance market rates. A brief chat with your agent or a quick online comparison every year ensures you’re not paying for outdated risks or missing new discounts. This is particularly important for insurance coverage types as your needs evolve.

- Adjust Your Deductibles Wisely: A higher deductible (the amount you pay out of pocket before insurance kicks in) generally means a lower premium. But here’s the caveat: make sure you can comfortably afford that deductible if you ever need to make a claim. There’s no point in saving $100 a year if a $2,500 deductible puts you in a financial bind.

- Consider Usage-Based Insurance: If you’re a safe, low-mileage driver, usage-based insurance programs (like the telematics ones mentioned earlier) can be a fantastic way to prove your low risk and secure better rates. It’s like personalized pricing based on your actual driving habits.

- Invest in Car Safety Features: Modern cars with advanced safety features (e.g., automatic emergency braking, lane departure warning) often qualify for discounts because they reduce the likelihood of accidents and theft. Even aftermarket alarms can sometimes earn you a small break.

It’s not just about the initial hunt for cheap full coverage car insurance USA; it’s about building habits that keep your premiums low for the long haul. And speaking of long-term financial planning, have you ever considered the benefits of a cashless mediclaim policy for your family ? It’s another area where smart choices can lead to significant savings and peace of mind.

So, there you have it. The idea that cheap full coverage car insurance USA is an oxymoron? It’s simply not true. It requires a bit of research, a willingness to compare, and an understanding of the factors that influence your rates. By being a proactive and informed consumer, you absolutely can secure comprehensive protection for your vehicle without breaking the bank. Don’t settle for the status quo; empower yourself to find the best deal.

Your Burning Questions About Cheap Full Coverage Car Insurance, Answered

Is cheap full coverage car insurance USA even possible?

Yes, absolutely! While “full coverage” isn’t a single product, combining liability, collision, and comprehensive coverage at an affordable rate is achievable. The key is to actively compare quotes from multiple providers, leverage all eligible discounts, and understand how factors like your driving record and vehicle type impact your premiums. It requires some effort, but the savings can be substantial.

What’s the difference between minimum vs full coverage?

Minimum coverage typically refers to the state-mandated liability insurance, which only covers damages you cause to other people or their property. It does not cover repairs to your own vehicle or your medical expenses. Full coverage, on the other hand, adds collision (for damage to your car in an accident) and comprehensive (for non-collision damage like theft, fire, or natural disasters), providing much broader protection for your own vehicle.

How often should I compare car insurance quotes?

It’s highly recommended to compare car insurance quotes at least once a year. Additionally, any major life event like buying a new car, moving to a different zip code, getting married, or even improving your credit score is an excellent opportunity to shop around for better rates. Insurers frequently update their algorithms and discount offerings, so staying vigilant can lead to significant savings.

Can my credit score affect my auto insurance premiums?

In most U.S. states, yes, your credit score can significantly influence your auto insurance premiums. Insurers use what’s called a “credit-based insurance score” to assess risk, as studies suggest a correlation between creditworthiness and the likelihood of filing claims. A higher credit score often leads to lower premiums. However, states like California, Hawaii, and Massachusetts have banned the use of credit scores for this purpose.

What car insurance discounts should I look for?

You should actively inquire about a wide range of car insurance discounts. Common ones include bundling policies (auto + home), good driver/safe driver programs (often with telematics), low mileage discounts, good student discounts, multi-car discounts, anti-theft device discounts, and even discounts for paying your premium in full or setting up automatic payments. Always ask your agent or check online what discounts you qualify for.