Alright, let’s be honest. Being a young driver in the UK is exhilarating, right? Freedom, independence, hitting the open road… and then you get that first car insurance quote. Ouch. It feels like a punch to the gut, doesn’t it? Suddenly, that dream car feels like a financial black hole, especially when you’re staring down premiums that could rival a small mortgage payment. You’re not alone in feeling this way; it’s a universal rite of passage for new drivers.

But here’s the thing: while it might feel like the system is rigged against you, it’s not entirely hopeless. As someone who’s navigated these waters (and seen countless others do the same), I can tell you there are genuinely smart, actionable strategies to bring those sky-high car insurance premiums down to earth. This isn’t about magic; it’s about understanding the game and playing it smartly. Think of me as your guide, sitting here with a cuppa, ready to walk you through the real talk on how to secure the cheapest car insurance UK for young drivers without compromising on essential cover. Let’s dive in.

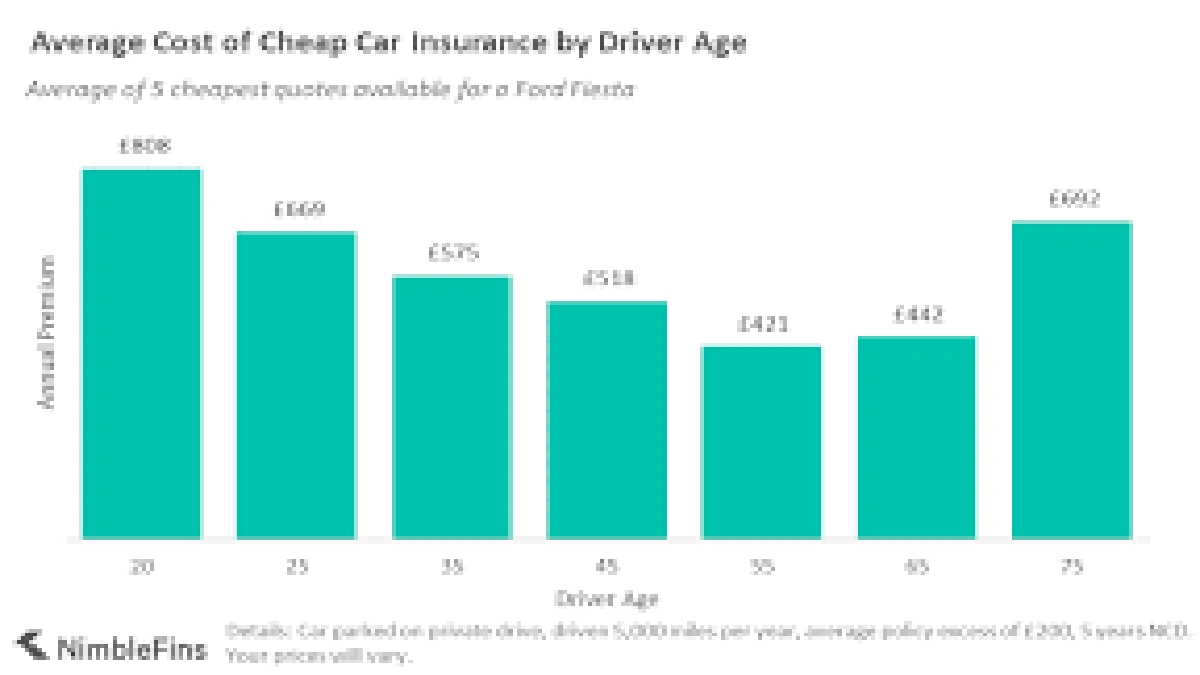

Why Are Young Drivers Hit So Hard? (Understanding the Landscape)

Before we can fix the problem, we need to understand why it exists. Insurers aren’t just arbitrarily hiking prices for younger drivers. The cold, hard data, unfortunately, paints a stark picture: statistically, young and inexperienced drivers (especially those under 25) are at a significantly higher risk of being involved in accidents. It’s not a judgment on your driving skills, but rather a reflection of less road experience, and sometimes, a higher propensity for risk-taking.

This higher risk directly translates into higher premiums. Insurers look at factors like your age, driving experience, location, the type of car you drive (which ties into insurance groups explained – more on that later), and even your job. For a young driver, many of these factors lean towards the ‘higher risk’ category, hence the eye-watering quotes. It’s a bitter pill to swallow, but acknowledging this reality is the first step towards finding solutions.

Your Toolkit for Taming Premiums | Practical Strategies That Work

Okay, enough about the ‘why.’ Let’s get to the ‘how.’ This is where you can genuinely make a difference to your insurance costs. These aren’t just theoretical tips; these are the strategies I’ve seen work time and time again for young drivers.

Telematics (Black Box) Insurance | Your Secret Weapon

If there’s one piece of advice I could shout from the rooftops, it’s this: seriously consider telematics insurance (black box). This is often the single most effective way for young drivers to reduce their premiums. A small device (the ‘black box’) is fitted to your car (or sometimes it’s an app on your phone), which monitors your driving habits – things like speed, acceleration, braking, cornering, and the time of day you drive. The better and safer you drive, the lower your premiums can become, often at renewal.

It’s essentially a way for you to prove to insurers that you’re a responsible driver, even if you don’t have years of no-claims history. While some people find the idea of being ‘monitored’ a bit unsettling, the savings can be truly substantial. For many, especially when looking for black box insurance UK, it’s a game-changer. It empowers you to directly influence your costs, which is a rare and valuable thing in the insurance world.

Beyond the Black Box | Other Smart Moves

Even if a black box isn’t for you (or you want to stack the odds even more in your favour), there are plenty of other tactics to employ:

- Drive Less, Pay Less: It sounds obvious, but fewer miles generally mean lower risk. If you can limit your annual mileage, make sure to give an accurate estimate when getting quotes. Don’t underestimate, though – accuracy is key!

- Increase Your Voluntary Excess: This is the amount you agree to pay towards a claim before your insurer pays out. A higher voluntary excess signals to insurers that you’re less likely to make small claims, which can reduce your premium. Just make sure it’s an amount you could realistically afford if you did need to claim.

- Add an Experienced Named Driver: If you live with an older, experienced driver (like a parent), adding them to your policy as a named driver can sometimes bring down your costs. Insurers see that the car will also be driven by someone with a lower risk profile. Crucially, do NOT commit ‘fronting’ – this is illegal and involves falsely claiming an experienced driver is the main user when they are not. The main driver must always be accurately declared.

- Consider a Pass Plus Course: This advanced driving course, taken after passing your practical test, can sometimes qualify you for discounts with certain insurers. It demonstrates a commitment to safer driving and enhances your skills. Many young drivers find the Pass Plus course pays for itself in reduced premiums over time.

- Choose Your Car Wisely: This is a big one. Cars are assigned to different insurance groups explained by insurers. Generally, cars in lower groups are cheaper to insure because they are less powerful, less expensive to repair, and less likely to be stolen. A smaller engine and fewer modifications can make a huge difference to your new driver insurance costs.

- Boost Your Car’s Security: An alarm, immobiliser, or even a tracking device can reduce the risk of theft, which in turn can lead to lower premiums. Always declare any security features when getting a quote.

The Hunt for the Best Deal | Where and How to Compare

Once you’ve done everything you can to make yourself a lower-risk candidate, it’s time to shop around. This is where the digital age truly shines. Using insurance comparison sites is non-negotiable. Don’t just get one quote; get several. These sites allow you to input your details once and receive multiple quotes from various insurers, making the process incredibly efficient.

However, a word of caution: while comparison sites are fantastic for finding initial quotes, not all insurers are on every platform. Some, like Direct Line, don’t appear on comparison sites at all, so it can be worth checking them directly too. When using comparison sites, be meticulously accurate with your information. Even small discrepancies can invalidate your policy or lead to issues down the line. Remember, the goal is the cheapest car insurance UK for young drivers, but also the right insurance for you. For more insights into how these platforms operate and what to look for, you might find general consumer advice on insurance comparison insightful, such as resources from organisations likeMoneyHelper.

What About Learner Drivers and Provisional Insurance?

Before you even get your full licence, you’ll need to think about learner driver insurance. This is crucial if you’re practicing in a private car (not a driving school’s vehicle). You have a few options here:

- Adding Yourself to a Parent’s Policy: This can be an option, but be aware that it will likely increase their premium significantly.

- Dedicated Provisional Driver Insurance: Many specialist insurers offer short-term or annual policies specifically for provisional licence holders. This is often a more cost-effective solution as it protects the main driver’s no-claims bonus and is designed for learners.

When it comes to learner driver insurance tips, always prioritize being adequately covered. Practicing regularly is essential, but doing so legally and safely is paramount. While you’re focused on your first car, it’s also good to broaden your financial literacy. You might one day need to explore other insurance options, like finding anonline quote for cheap small business insurance in the USA, should your career path lead you to entrepreneurship.

Long-Term Savings | Building Your No Claims Bonus

Once you’re on the road with your full licence, your focus should shift to building a no claims bonus (NCB), also known as a no claims discount (NCD). This is arguably the most powerful long-term tool for reducing your insurance costs. For every year you drive without making a claim, you earn a year of NCB, which can lead to significant discounts on your premium. After five years, you could be looking at a discount of 60% or more!

Protecting your NCB is vital. Some insurers offer NCB protection, often for an additional fee, which allows you to make one or two claims without losing your accumulated discount. Consider this carefully, especially as your NCB grows. Even as a new driver, every year you drive safely and claim-free is a building block towards much more affordable insurance in the future. Thinking ahead, as you grow and potentially embark on your own ventures, understanding different facets of financial protection becomes crucial. For instance, knowing aboutcommercial liability insurance for small businessescould be vital down the line.

Frequently Asked Questions (FAQ)

Q1 | Can I really get cheap car insurance as a young driver in the UK?

Yes, absolutely! While it’s generally more expensive, by implementing strategies like telematics insurance, choosing a lower insurance group car, increasing your voluntary excess, and shopping around diligently using car insurance comparison young drivers tools, you can significantly reduce your premiums. It requires effort, but it’s definitely achievable.

Q2 | What is a black box, and how does it help lower premiums?

A black box (or telematics device) is a small unit fitted to your car that monitors your driving behaviour, including speed, acceleration, braking, and time of day you drive. Insurers use this data to assess your individual risk. If you demonstrate safe driving habits, they reward you with lower premiums, making it a key tool for how to lower car insurance for young drivers.

Q3 | Should I add my parents to my insurance policy?

Adding an experienced parent or guardian as a named driver can sometimes reduce your premium, as insurers perceive less risk. However, you must be the main driver if you are the primary user of the car. Falsely stating someone else is the main driver (known as ‘fronting’) is illegal and can lead to your policy being cancelled and potential prosecution.

Q4 | What’s the difference between Third Party, Fire & Theft, and Comprehensive cover?

Third Party, Fire & Theft covers damage to other people’s cars/property, and also covers your car if it’s stolen or catches fire. Comprehensive cover includes all of the above, plus damage to your own car in an accident, regardless of fault. While Third Party might seem cheaper upfront, sometimes Comprehensive policies can be more competitive for young drivers due to ‘risk loading’ on basic policies.

Q5 | How often should I compare car insurance quotes?

You should compare quotes every year before your renewal date. Don’t just automatically renew with your current insurer, as they rarely offer the best deal. Many experts recommend looking for quotes around 3-4 weeks before your renewal date, as this often yields the most competitive prices.

So, there you have it. Navigating the world of cheapest car insurance UK for young drivers might seem daunting at first, but with a bit of savvy and the right strategies, you absolutely can find a policy that doesn’t break the bank. Remember, every year you drive safely and accumulate that precious no claims bonus is another step towards even more affordable insurance. Drive smart, compare wisely, and enjoy the freedom of the open road!