Alright, let’s talk shop. You’ve poured your heart and soul into your online store, right? Sourcing products, building that slick website, nailing your marketing… it’s a grind, but it’s your grind. And honestly, it’s exhilarating! But here’s the thing that often gets pushed to the back burner, the silent worry that can turn into a full-blown nightmare: what happens when things go wrong? I’m not talking about a delayed shipment; I mean a real, business-threatening hiccup. This is where a robust ecommerce business insurance USA policy isn’t just a good idea, it’s non-negotiable. And let me tell you, navigating the world ofonline business insurancecan feel like trying to solve a Rubik’s Cube blindfolded. But don’t worry, I’m here to guide you, step-by-step, through exactly how to secure the protection your digital empire deserves.

Why Your Online Store Isn’t as Safe as You Think | The “Why” Behind Insurance

It’s easy to think that because you don’t have a physical storefront, you’re somehow immune to traditional business risks. Oh, if only that were true! In my experience, online businesses, especially in the US market, face a unique cocktail of vulnerabilities that can be far more complex than their brick-and-mortar counterparts. Think about it: you’re dealing with customer data, potentially shipping products across state lines, and relying heavily on digital infrastructure. Each of these introduces specific risks.

For instance, let’s consider a data breach. It’s not just big corporations that get hit; small and medium-sized e-commerce ventures are increasingly targets. One moment you’re processing orders, the next, your customers’ credit card details or personal information are compromised. The fallout? Legal fees, regulatory fines, customer notification costs, and a crushing blow to your brand’s reputation. This is precisely why a strong ecommerce business insurance USA policy , specifically with a focus on cyber risks, is paramount.

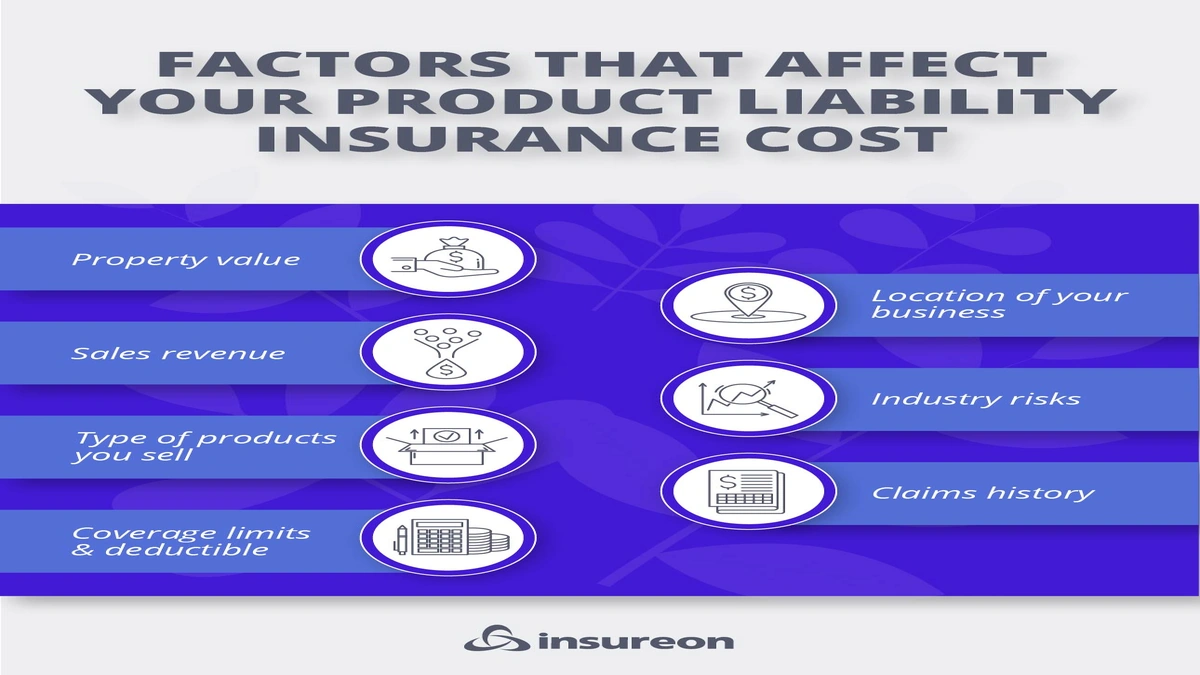

Then there’s theproduct liability insuranceaspect. You sell a fantastic widget, but what if, through no fault of your own, it causes injury or property damage to a customer? Suddenly, you’re facing a lawsuit. Or what about shipping? A package goes missing, arrives damaged, or worse, someone claims they never received it. Without the right coverage, these aren’t just inconveniences; they’re direct hits to your bottom line, potentially wiping out months, or even years, of hard work. It’s not about being pessimistic; it’s about being prepared, because the digital landscape, while full of opportunity, is also full of potential pitfalls.

Decoding the Jargon | Key Ecommerce Business Insurance USA Policy Types You Need

When you start looking into insurance, you’ll encounter a dizzying array of terms. Let me break down the essentials you absolutely need to consider for your online store insurance :

- Commercial General Liability (CGL): This is your foundational protection. It covers claims of bodily injury or property damage caused by your business operations, products, or services. Even if you don’t have a physical store, a customer could slip and fall picking up an order from your home office, or a product you sell could damage their property. This is your first line of defense against general e-commerce liability.

- Product Liability Insurance: Crucial for any business selling physical goods. As discussed, if a product you sell causes injury or damage, this policy steps in to cover legal fees, settlements, and judgments. It’s a must-have, especially if you’re importing goods or selling items where safety could be a concern.

- Cyber Liability Insurance: This is arguably the most critical for an online business. It covers costs associated with data breaches, cyberattacks, network security failures, and privacy violations. Think forensic investigations, credit monitoring for affected customers, legal defense, and regulatory fines. It’s your ultimate cyber security insurance for online stores.

- Business Interruption Insurance: What if your website crashes for an extended period, or your payment processor goes down, halting sales? This policy can help replace lost income and cover ongoing expenses while your business recovers from a covered event. It’s vital for maintaining cash flow when the unexpected hits.

- Shipping Insurance: While often an add-on or available through carriers, specific policies can protect against lost, stolen, or damaged goods during transit. For businesses with high-value or high-volume shipments, this can be a lifesaver, especially with the rise of porch piracy.

Understanding these core types is the first step in building comprehensive digital business protection . Don’t just pick a generic policy; make sure it’s tailored to the specific risks of your online operations.

Crafting Your Protection Plan | A Step-by-Step Guide to Getting Covered

So, how do you actually get this done? It might seem overwhelming, but I promise, it’s manageable. Here’s how I’d approach it:

- Assess Your Risks Thoroughly: Sit down and honestly evaluate your business. What do you sell? Where do you store data? What’s your average order value? Do you handle sensitive information? The more specific you are, the better you can articulate your needs to an insurer. Think about your supply chain, your customer base, and your operational vulnerabilities.

- Research Reputable Providers: Not all insurance companies are created equal, especially when it comes to the nuances of e-commerce. Look for providers with experience in covering online businesses or those specializing in small business insurance. Read reviews, check their financial stability, and see if they offer specific e-commerce packages. While finding cheap homeowners insurance might be straightforward, tailoring an e-commerce policy requires more specialized attention.

- Get Multiple Quotes: Never settle for the first quote. Reach out to at least three different providers. This isn’t just about finding the best small business e-commerce insurance cost; it’s about comparing coverage details, deductibles, and exclusions. What one policy covers, another might not, or might cover differently.

- Understand the Fine Print (Seriously!): This is where many people stumble. Policies are dense, but you must understand what’s covered, what’s excluded, and what your responsibilities are. Ask questions. If something isn’t clear, get clarification in writing. An insurance broker specializing in e-commerce can be invaluable here, helping you decipher the legalese.

- Regularly Review and Update Your Policy: Your business isn’t static, so your insurance shouldn’t be either. As you grow, add new products, expand into new markets, or change your operating procedures, your risks evolve. Make it a habit to review your business insurance for online sellers annually with your provider to ensure you’re still adequately protected.

Common Pitfalls and How to Avoid Them | My Experience-Backed Advice

I’ve seen plenty of online businesses make avoidable mistakes when it comes to insurance. Here are a couple of big ones, and how you can steer clear:

One common pitfall is underinsurance . Many entrepreneurs, trying to save a buck, opt for the bare minimum coverage. But what happens when a claim far exceeds your policy limits? You’re on the hook for the rest. It’s like buying acheapest car insurance for new driversbut then getting into an accident that totals a luxury vehicle – your basic policy might not cut it. Don’t let a small saving now lead to catastrophic losses later. Work with an expert to determine realistic coverage amounts for potential scenarios.

Another mistake is assuming all your risks are covered. Just because you have a general policy doesn’t mean it covers everything. For example, many standard CGL policies might have exclusions for cyber-related incidents. Or, if you’re dropshipping, the liability might fall on the manufacturer, but your business could still be named in a lawsuit, requiring defense. Always, always confirm that specific risks unique to your e-commerce model, like potential shipping damage insurance needs or specific product liabilities, are explicitly addressed.

And finally, not updating your policy. Your business is dynamic. Are you suddenly selling internationally? Have you started collecting more customer data? Did you launch a new product line with higher inherent risks? Each of these changes warrants a conversation with your insurer to adjust your ecommerce business insurance USA policy . Proactive management is key to truly protect your online business .

FAQs | Your Burning Questions About Ecommerce Business Insurance USA Policy Answered

What exactly does product liability insurance cover for an online store?

Product liability insurance covers legal fees, settlements, and judgments if a product you sell causes bodily injury or property damage to a third party. This is critical for e-commerce businesses, especially those selling physical goods, as it protects against claims related to manufacturing defects, design flaws, or inadequate warnings.

Is cyber liability insurance truly necessary for a small e-commerce business?

Absolutely. Small e-commerce businesses are increasingly targeted by cyberattacks. Cyber liability insurance covers costs associated with data breaches, ransomware attacks, and other cyber incidents, including forensic investigations, legal fees, customer notification, and sometimes even business interruption due to the attack. It’s a vital component of any modern ecommerce business insurance USA policy .

How can I find the best small business e-commerce insurance cost?

To find the best cost, start by thoroughly assessing your specific risks and needs. Then, get quotes from multiple insurance providers who specialize in e-commerce or small business. Compare not just the price, but also the coverage limits, deductibles, and exclusions. Working with an independent broker can also help you compare options efficiently and find competitive rates without sacrificing essential coverage.

What if I sell digital products or services, do I still need an ecommerce business insurance USA policy?

Yes, even if you sell digital products or services, you likely need insurance. While product liability might be less of a concern, you still face risks like cyber liability (for data breaches), professional liability (if your service causes financial harm to a client), and general liability. Your specific needs will vary, so consult with an insurer to tailor a policy.

Does my home insurance cover my home-based online business?

In most cases, no. Standard homeowners insurance policies offer very limited, if any, coverage for business-related losses or liabilities. It’s designed for personal property and liabilities. Running an e-commerce business from home typically requires a separate ecommerce business insurance USA policy to adequately protect your inventory, equipment, and especially against business-specific liabilities like product claims or data breaches.

So, there you have it. The world of ecommerce business insurance USA policy might seem complex, but with the right approach and a clear understanding of your needs, you can build a formidable shield around your online venture. Don’t wait for a crisis to realize you’re exposed. Take these steps, protect your passion, and keep building that amazing business you’ve worked so hard for. Because at the end of the day, peace of mind is priceless.