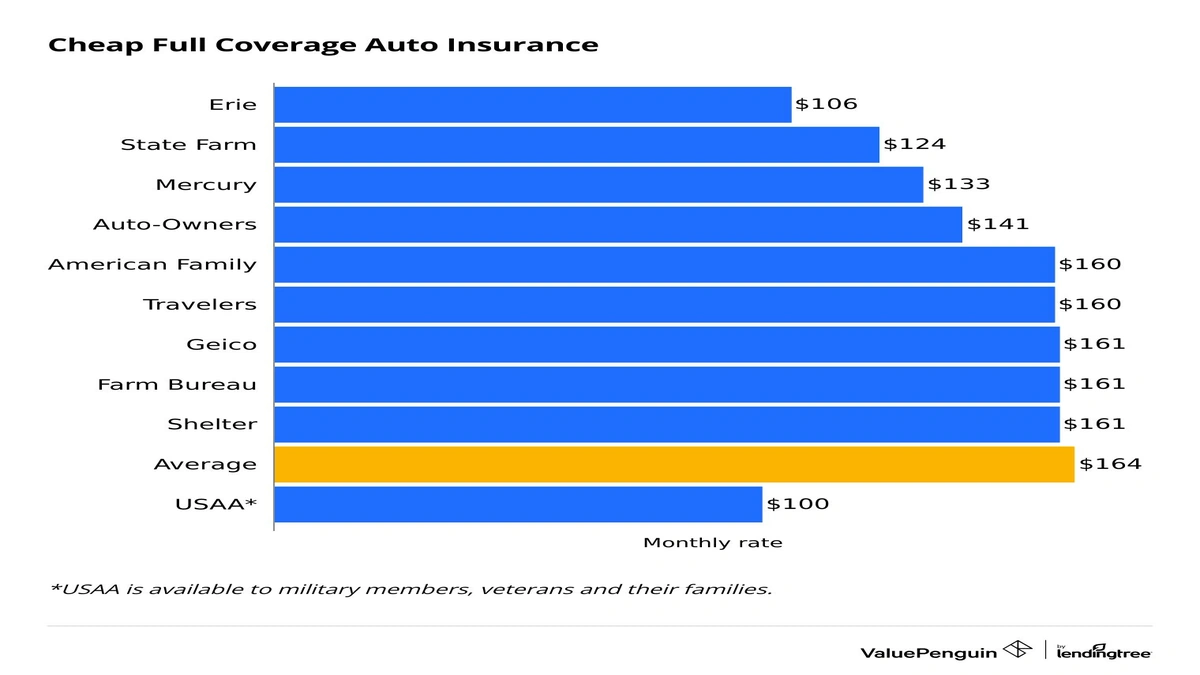

Alright, let’s be honest. The idea of getting full coverage car insurance under $100 USA sounds like finding a unicorn, doesn’t it? In a world where everything seems to be getting pricier, especially anything to do with cars, this figure feels almost too good to be true. And you know what? For many, it is a challenge. But here’s the thing: it’s not an impossible dream. What fascinates me is how often people give up before they even understand the game. My goal today is to pull back the curtain, give you the inside scoop, and equip you with the exact playbook to chase down those elusive, truly affordable car insurance rates. Consider me your co-pilot on this journey to smarter auto insurance. We’re going beyond the surface-level advice to truly understand how some people manage this, and how you might too.

I’ve seen countless drivers frustrated, feeling like they’re stuck paying exorbitant premiums. They assume that robust protection comes with an equally robust price tag. But what if I told you that with the right strategy, a bit of persistence, and knowing exactly where to look, you could significantly reduce your premium costs ? This isn’t about cutting corners on safety; it’s about being an informed consumer in a complex market. So, let’s ditch the guesswork and dive deep into what it takes to secure cheap full coverage without compromising your peace of mind.

The Reality Check | What “Full Coverage” Really Means (and Why it Matters)

First things first: let’s bust a common myth. There’s no single policy called “full coverage.” When people, or even agents, talk about full coverage car insurance , they’re actually referring to a bundle of different protections designed to cover a wide range of scenarios. Think of it as a custom-built suit of armor for your car and your wallet. Typically, this bundle includes:

- Liability Coverage: This is the non-negotiable foundation. It covers damages and injuries you might cause to other people and their property in an at-fault accident. Every state mandates a minimum amount of liability coverage, but let me tell you, those state minimums are often woefully inadequate.

- Collision Coverage: This pays for damages to your own vehicle if you hit another car, an object (like a tree or a pole), or if your car rolls over. It’s a lifesaver if you have a newer car or one you couldn’t afford to replace out-of-pocket.

- Comprehensive Coverage: This is your “Acts of God and other weird stuff” coverage. It protects your car from things like theft, vandalism, fire, natural disasters (hail, floods), and even hitting an animal.

Beyond these core three, many drivers also add things like uninsured/underinsured motorist coverage (highly recommended, honestly), medical payments, or personal injury protection. So, when we talk about getting full coverage car insurance under $100 USA , we’re talking about finding a sweet spot where this robust combination of protections fits your budget. It’s about more than just meeting the bare minimum; it’s about smart, comprehensive protection for your valuable vehicle insurance asset.

Decoding the Dollar Sign | Factors That Pump Up (or Shrink) Your Premium

Before we get to the “how-to,” we need to understand the “why.” Insurance companies aren’t just pulling numbers out of a hat. They use a sophisticated algorithm to assess risk, and that assessment directly translates into your premium. Understanding these factors affecting premiums is your first step toward gaining control:

- Your Driving Record: This is probably the biggest one. A clean record with no accidents or tickets for several years signals lower risk. Conversely, a recent at-fault accident or a string of speeding tickets will undoubtedly hike your rates. It’s just how it is.

- Your Vehicle: What you drive matters. A high-performance sports car is more expensive to insure than a modest sedan. Why? Higher repair costs, higher theft rates, and often, higher risk-taking associated with the driver profile. Safety features can help, but a brand-new luxury SUV will always cost more to insure than a ten-year-old Honda Civic.

- Your Location: Where you live and park your car makes a huge difference. High-crime areas, urban centers with more traffic and accidents, or regions prone to natural disasters (think hail in Texas or hurricanes in Florida) will see higher rates. A quiet suburban street generally means lower risk.

- Your Age and Experience: Younger, less experienced drivers (especially those under 25) typically face the highest premiums because statistically, they’re involved in more accidents. As you gain experience and maintain a clean record, your rates tend to decrease.

- Your Credit Score (in most states): Yes, your credit score can influence your insurance rates. Insurers use what’s called an “insurance score,” which is derived from your credit history, as a predictor of how likely you are to file a claim. A higher score often means lower premiums.

- Your Annual Mileage: The less you drive, the less risk you pose. Some insurers offer discounts for low-mileage drivers.

See? It’s a complex web. But recognizing these variables is crucial because it helps you understand where you might have leverage to influence your auto insurance policy costs.

Your Blueprint for Savings | Actionable Steps to Hit That Sub-$100 Mark

Okay, this is where the rubber meets the road. If you’re serious about finding full coverage car insurance under $100 USA , you need a proactive strategy. Here are my top auto insurance tips :

1. Be a Comparison Shopping Ninja

This is non-negotiable. Never, ever settle for the first quote you get or blindly renew with your current provider year after year. Insurance rates vary wildly between companies for the exact same coverage. Use online insurance comparison tools, call independent agents who work with multiple carriers, and get at least 3-5 car insurance quotes every 6-12 months. I’ve seen people save hundreds, sometimes thousands, just by doing this one thing. It’s the simplest way to find the best car insurance deals out there.

2. Optimize Your Deductibles

Your deductible is the amount you pay out-of-pocket before your insurance kicks in for a claim. Generally, the higher your insurance deductibles , the lower your premium. If you have a healthy emergency fund, consider raising your deductibles from, say, $500 to $1,000 or even $1,500. Just make sure you can comfortably afford that deductible if you ever need to file a claim. It’s a calculated risk, but often a smart one to save on car insurance .

3. Stack Those Discounts!

This is where the real magic can happen. Most insurance companies offer a plethora of discounts, but they won’t always volunteer them. You need to ask! Common discounts include:

- Bundling: Combine your auto insurance with other policies, like health insurance or home insurance, and you can often snag a significant discount.

- Good Driver/Safe Driver: If you have a clean record for a certain number of years, you likely qualify.

- Good Student: For younger drivers, maintaining a B average or higher can lead to savings.

- Multi-Car: Insuring more than one vehicle with the same provider.

- Anti-Theft Devices: Alarms, tracking systems, VIN etching.

- Payment Method: Paying in full, opting for autopay, or going paperless.

- Telematics/Usage-Based Insurance: Some insurers offer devices or apps that monitor your driving habits (speed, braking, mileage). Drive safely, and you get a discount. This is a fantastic way for good drivers to get discount auto insurance.

Don’t be shy; ask your agent for a full list of every single discount they offer. This is a critical step in figuring out how to lower insurance costs .

4. Choose Your Vehicle Wisely

If you’re in the market for a new (or new-to-you) car, research its insurance costs before you buy. Cars with high safety ratings, lower theft rates, and less expensive parts generally cost less to insure. A family sedan will almost always be cheaper to insure than a sports coupe or a high-end luxury SUV. This might seem obvious, but it’s often overlooked in the excitement of a new purchase.

5. Maintain a Stellar Driving Record

This goes without saying, but it bears repeating. Every accident, every ticket, can stay on your record for years and directly impact your rates. Drive defensively, obey traffic laws, and avoid distractions. It’s not just about safety; it’s about keeping your premiums low.

Navigating the Nuances | State Minimums vs. Smart Coverage

We touched on state minimums earlier, but let’s delve a bit deeper. While they’re legally sufficient, they rarely offer adequate protection. Imagine causing an accident that totals another person’s luxury car and sends them to the hospital. If your liability coverage is only $25,000, and the damages are $100,000, you’re on the hook for the remaining $75,000. That’s a financial nightmare.

The trick to getting full coverage car insurance under $100 USA isn’t just about finding the lowest possible number; it’s about finding the lowest possible number for smart coverage. This means balancing affordability with sufficient protection for your assets. You might opt for slightly higher liability limits (e.g., $100,000/$300,000/$50,000) while still keeping your overall premium low by diligently applying all the savings strategies we’ve discussed. It’s about being strategic, not just cheap.

The Bottom Line | Is It Truly Possible for YOU?

So, after all this, can you actually get full coverage car insurance under $100 USA ? The answer, like most things in life, is: it depends. It’s challenging, but absolutely possible for many drivers, especially if you:

- Have a clean driving record.

- Drive a modest, older, or highly-rated safe vehicle.

- Live in an area with lower insurance costs.

- Have a good credit score.

- Are diligent about comparing quotes and maximizing discounts.

- Are willing to take a slightly higher deductible.

I’ve seen it happen. People come to me convinced it’s impossible, and after a few strategic adjustments and some dedicated comparison shopping, they find themselves with robust protection at a price they didn’t think was achievable. It requires effort, but the payoff hundreds of dollars saved annually is more than worth it. Don’t let the complexity deter you; empower yourself with knowledge and persistence. Your wallet will thank you.

Frequently Asked Questions About Affordable Full Coverage

What exactly is considered “full coverage” car insurance?

“Full coverage” isn’t a single policy but a combination of several, typically including liability, collision, and comprehensive insurance. It’s designed to protect you against a wide range of financial losses from accidents, theft, and other damages to your vehicle.

Can my driving record really impact my premium that much?

Absolutely, yes! Your driving record is one of the most significant factors. A clean record with no accidents or violations signals lower risk to insurers, leading to lower premiums. Conversely, a history of tickets or at-fault accidents will almost certainly increase your costs.

Are there specific discounts I should always ask about?

Yes, definitely! Always inquire about multi-policy (bundling), multi-car, good driver, good student, anti-theft device, and telematics (usage-based) discounts. Many insurers offer these, but you often have to ask to ensure you’re getting all the savings you qualify for.

Is it better to pay my premium monthly or annually?

Generally, paying your premium annually (in one lump sum) is cheaper. Many insurance companies offer a discount for paying in full, as it reduces their administrative costs and the risk of missed payments compared to monthly installments.

What if I can’t find full coverage under $100 in my state?

If you’re struggling to find rates under $100, don’t despair. Re-evaluate your deductibles, ensure you’ve applied for every possible discount, and broaden your search to more insurance providers. Consider increasing liability slightly if it offers more options. While $100 is a target, getting close to it with solid coverage is still a huge win.

How often should I compare car insurance quotes?

You should compare car insurance quotes at least once a year, or whenever significant life events occur. These include buying a new car, getting married, moving to a new address, adding a new driver to your policy, or if you’ve recently improved your credit score. Being proactive ensures you’re always getting the best possible rate.