Alright, let’s be honest. When you’re looking for professional indemnity insurance UK cost , your first instinct is probably to Google ‘cheapest PI insurance UK’ and compare a few numbers. I get it. We all want to save a few quid, especially when running a business in the UK. But here’s the thing, and this is crucial: focusing solely on the lowest number can be a massive misstep. It’s like buying the cheapest parachute without checking if it actually opens. What fascinates me about insurance, particularly something as vital as professional indemnity, is how often people miss the ‘why’ behind the numbers.

This isn’t just about getting a policy; it’s about safeguarding your livelihood, your reputation, and frankly, your peace of mind. The true professional indemnity insurance UK cost isn’t just the annual premium you pay; it’s the value it delivers when things inevitably go sideways. So, let’s dive deeper than just the quotes and truly understand what influences these prices and, more importantly, why you absolutely need to.

Unpacking the “Why” | What Really Drives Your PI Premium?

You might think your profession is the only factor, but trust me, it’s far more nuanced. When insurers calculate your professional indemnity insurance UK cost , they’re looking at a complex tapestry of risk. It’s not just a dart throw; it’s an intricate calculation. Let me rephrase that for clarity: they’re assessing the likelihood of you making a mistake and the potential financial fallout if you do.

Here are the primary indemnity insurance cost factors that dictate your premium:

- Your Profession and Services: This is probably the most significant. An architect, for example, faces different risks than a marketing consultant. The potential for catastrophic error (think structural collapse versus a poorly worded ad campaign) directly impacts the premium. High-risk professions, like legal or financial advice, will naturally see higher costs for their professional liability insurance UK.

- Your Annual Turnover: Generally, the higher your revenue, the more projects you’re undertaking, and the larger the potential claims against you could be. It’s a pretty straightforward correlation.

- Your Claims History: Have you made claims in the past? This is a huge red flag for insurers. A clean record can significantly reduce your annual premium. It’s basic risk assessment, isn’t it?

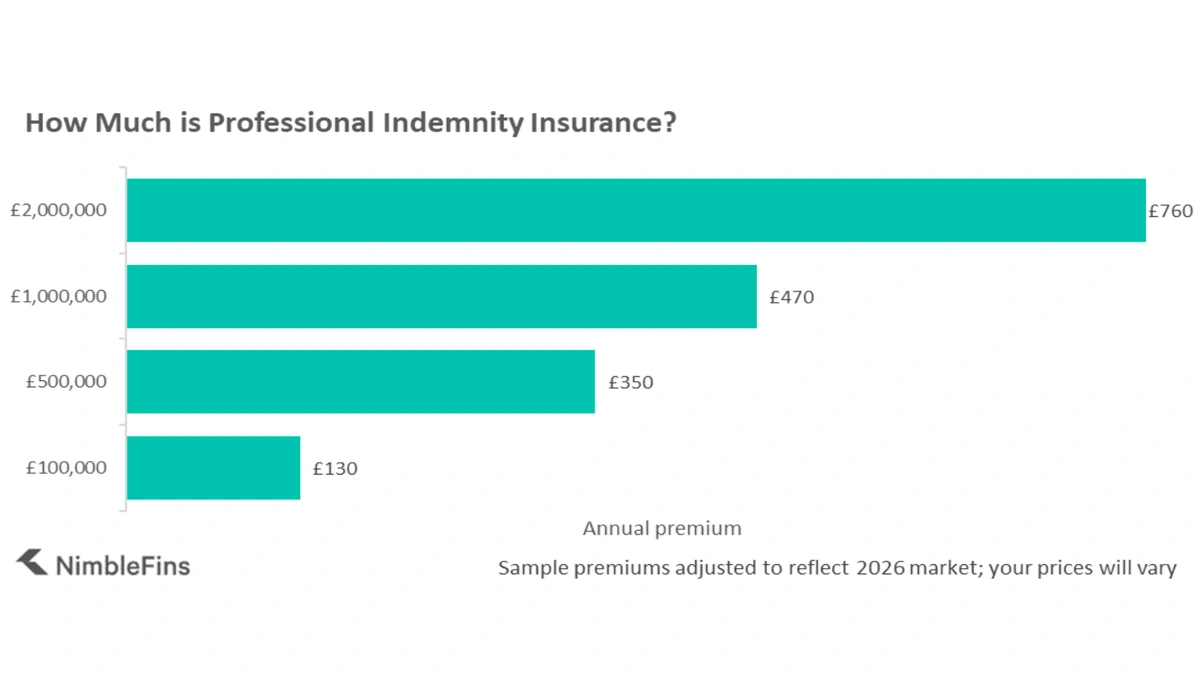

- The Level of Coverage (Sum Insured): This is the maximum amount your policy will pay out. Opting for higher coverage limits will, of course, increase your premium. But the question you should be asking isn’t ‘how low can I go?’, but ‘what’s the realistic worst-case scenario?’

- The Excess (or Deductible): This is the amount you agree to pay towards a claim before your insurer steps in. A higher excess usually means a lower premium, but be careful not to choose an amount you couldn’t comfortably afford in a crisis.

- Contractual Requirements: Sometimes, clients or professional bodies mandate a minimum level of PI insurance UK. This isn’t optional; it’s a prerequisite for doing business.

- Business Structure and Number of Employees: A sole trader generally faces different risks and therefore different premiums than a large consultancy firm with multiple employees.

So, you see, it’s not just a single number. It’s a reflection of your specific risk profile. Understanding these drivers is the first step in getting a policy that actually fits, rather than just one that’s cheap.

The Hidden Value | Why Skimping on PI Insurance Can Cost You More

I initially thought this was straightforward, but then I realized how many people underestimate the true cost of not having adequate professional indemnity insurance UK . It’s a classic case of ‘penny wise, pound foolish.’ If you’re a freelancer, a consultant, or a small business owner, a single professional error, an oversight, or even an allegation of negligence can trigger a claim that could financially cripple you. We’re talking about legal fees, compensation, and the immeasurable damage to your professional reputation.

Imagine this: a client alleges your advice led to significant financial loss. Without proper professional liability insurance , you’re looking at potentially tens of thousands of pounds in legal defence costs alone, even if you’re completely innocent. Add to that the stress, the time away from your actual work, and the potential for a public dispute, and suddenly that slightly higher premium doesn’t look so bad, does it? TheAssociation of British Insurersoften highlights the critical role insurance plays in protecting businesses.

This is where the ‘why’ truly comes into play. You’re not just buying a piece of paper; you’re buying a robust financial shield. It allows you to operate with confidence, knowing that if an honest mistake or an unfair accusation arises, you have expert legal and financial backing. It’s an investment in your business’s longevity, much like ensuring yourcar insurance renewalis up to date, or having comprehensivehome insuranceto protect your assets.

Navigating the Market | How to Get Competitive PI Insurance UK Quotes

So, you’re convinced you need it (and you absolutely do!). Now, how do you go about finding the right policy without overpaying? It’s not about finding the absolute cheapest number, but the best value for your specific needs. Getting accurate PI insurance UK quotes requires a bit of homework, but it’s time well spent.

1. Be Transparent and Thorough: When providing information to brokers or insurers, be completely honest and provide as much detail as possible about your services, clients, and processes. Misrepresentation, even accidental, can invalidate your policy when you need it most. This includes your estimated turnover and any previous claims. Accuracy is king here.

2. Consider a Specialist Broker: While direct insurers are an option, a good broker who specialises in business insurance UK , especially professional indemnity, can be invaluable. They have access to multiple insurers, understand the nuances of different policies, and can often negotiate better terms than you could on your own. They can help you compare different policies, not just on price, but on coverage specifics.

3. Compare Like-for-Like: Don’t just look at the premium. Compare the coverage limits , the excess, the exclusions, and any additional benefits. A slightly higher premium for broader coverage or lower excess might be a better deal in the long run. It’s a common mistake I see people make: comparing only the top-line number without reading the small print.

4. Review Annually: Your business changes, and so does the insurance market. Don’t just auto-renew. Take the time each year to review your policy and get fresh indemnity insurance quotes . You might find a better deal or realise your current coverage is no longer adequate.

Tailoring Your Coverage | Special Considerations for Small Businesses and Freelancers

If you’re a small business professional indemnity seeker or a freelancer professional indemnity UK , your needs are often unique. You might not have a huge corporate structure, but your personal liability is often more exposed. Many freelancers, for instance, are required by contracts to hold a certain level of PI cover. It’s not just a good idea; it’s often a contractual necessity.

For freelancers, especially, the lines between personal and professional can blur. A claim against your business can feel like a direct attack on you personally. Therefore, choosing the right coverage limits that reflect the scale and potential impact of your work is paramount. Don’t just pick the lowest option; consider the worst-case scenario. What if a project goes wrong and costs your client hundreds of thousands? Could your current policy cover that?

Furthermore, ensure your policy covers all the services you offer. If you’ve expanded your offerings since you first took out your policy, you might need to update your coverage. It’s all about ensuring your policy evolves with your business. That’s the smart way to approach freelancer insurance UK .

Ultimately, while the professional indemnity insurance UK cost is a significant consideration, it should never be the only consideration. Think of it as an essential investment in your professional future, a safety net that allows you to take calculated risks and grow your business without constant fear of the unknown. It’s about protecting what you’ve built, and that, my friend, is truly priceless.

Frequently Asked Questions About Professional Indemnity Insurance UK Cost

What is the average professional indemnity premium in the UK?

The average professional indemnity premium varies significantly based on your profession, turnover, and chosen coverage limits. For a low-risk freelancer, it might start from around £150-£300 per year, while high-risk professions or larger firms could pay thousands. It’s essential to get tailored indemnity insurance quotes for an accurate figure.

Can I get professional indemnity insurance UK if I work from home?

Absolutely. Your working location (home office, co-working space, client site) typically has little direct impact on your professional indemnity insurance UK cost . The key factors remain your profession, services, and turnover, not where you physically perform the work. Many insurers cater specifically to home-based businesses and freelancers.

How do coverage limits affect the cost of professional indemnity?

Higher coverage limits (the maximum amount your policy will pay out per claim or in total for the year) will directly increase the cost of professional indemnity . Insurers charge more for taking on greater potential financial risk. It’s crucial to select limits that adequately reflect the potential financial impact of a claim against your specific services.

Is professional liability insurance the same as professional indemnity insurance?

Yes, in the UK, professional liability insurance is generally another term for professional indemnity insurance . Both cover financial losses incurred by third parties due to professional negligence, errors, or omissions in your advice or services. Different countries might use these terms with subtle distinctions, but for the UK, they are largely interchangeable.