Alright, let’s grab a cuppa and talk about something that most small business owners in the UK probably don’t spend enough time thinking about: professional liability insurance. I know, I know, insurance isn’t exactly the most thrilling topic. But here’s the thing: in today’s fast-paced, often litigious world, this isn’t just another checkbox on your business to-do list. It’s a foundational piece of your security, a silent guardian that protects your hard-earned reputation and finances. What fascinates me is how many brilliant entrepreneurs, especially those running asmall business, genuinely underestimate the ‘why’ behind this particular cover. It’s not just about what you do, but the advice you give, the services you render, and the expertise you share.

We’re going to dive deep into why this specific type of insurance isn’t merely a ‘nice-to-have’ but an absolute necessity for anyone offering professional services or advice in the UK. We’ll look beyond the jargon and uncover the real-world implications, the hidden contexts, and the potential pitfalls that could derail your business if you’re not properly protected.

Beyond the Basics: What Exactly Is Professional Liability Insurance?

So, you’ve heard the term, maybe even seen it pop up when you’re looking for generalbusiness insurance. But what does professional liability insurance (PLI) actually do? At its core, it’s designed to protect professionals from claims of negligence, errors, or omissions in the services they provide. Think of it this way: if a client alleges that your advice, design, or service caused them financial loss, PLI steps in to cover legal defence costs and any damages awarded.

This is where it gets interesting. Many confuse it with public liability insurance, which covers claims for injury or property damage to third parties (like a client tripping in your office). PLI, often referred to as professional indemnity insurance UK, is different. It’s about the quality of your professional service or advice. For instance, if you’re an IT consultant and a piece of software you recommended causes a client’s system to crash, leading to significant downtime and financial loss, that’s where PLI would come into play. It’s a shield against the consequences of human error, misjudgment, or even just miscommunication, which, let’s be honest, can happen to the best of us.

The Hidden Risks | Why Your Expertise Can Be Your Biggest Vulnerability

You’re an expert in your field, right? That’s why clients come to you. But paradoxically, your expertise can also be your biggest source of vulnerability. Every piece of advice, every design, every strategic plan you deliver carries an inherent risk. What if a client misunderstands your recommendation? What if a small detail is overlooked in a complex project? These aren’t just theoretical scenarios; they lead to real-world problems and, potentially, a professional negligence claim.

I initially thought this was straightforward, but then I realized the depth of the exposure. Consider a marketing agency that promises a certain ROI, but due to unforeseen market shifts, the client doesn’t achieve it. Or an architect whose design, while technically sound, is later deemed impractical by the client, causing project delays and cost overruns. These situations can quickly escalate into costly contractual disputes and legal battles that can cripple asmall business. This is why robust small business risk management isn’t just about protecting physical assets; it’s about safeguarding your intellectual capital and the trust clients place in you.

It’s Not Just for Lawyers | Who Really Needs This Cover in the UK?

When you hear ‘professional liability insurance’, your mind might immediately jump to doctors, lawyers, or accountants. And yes, they absolutely need it. But the scope for PLI is far, far broader in the modern UK economy. If your business provides advice, consultancy, design, or services based on your knowledge and skills, you’re likely exposed. This includes, but isn’t limited to:

- IT consultants & web developers

- Marketing & PR agencies

- Business coaches & trainers

- Architects & engineers

- Graphic designers & photographers

- Freelancers across various sectors

- Estate agents & financial advisors

The common thread? A ‘duty of care’ to your clients. You’re expected to perform to a certain professional standard. If you fall short, or are perceived to have fallen short, the consequences can be severe. Even if the claim is baseless, the legal costs to defend yourself can be astronomical. And that, my friends, is a burden no small business should have to bear alone.

Navigating the Maze | Finding the Right Professional Liability Insurance

So, you’re convinced. You understand the ‘why’. Now comes the ‘how’. Finding the right professional liability insurance for small business UK can feel a bit like navigating a maze, but it doesn’t have to be. My advice? Don’t go it alone. Working with experienced insurance brokers UK who understand your specific industry and its risks is invaluable. They can help you tailor a policy that fits your unique needs, rather than a generic, off-the-shelf solution.

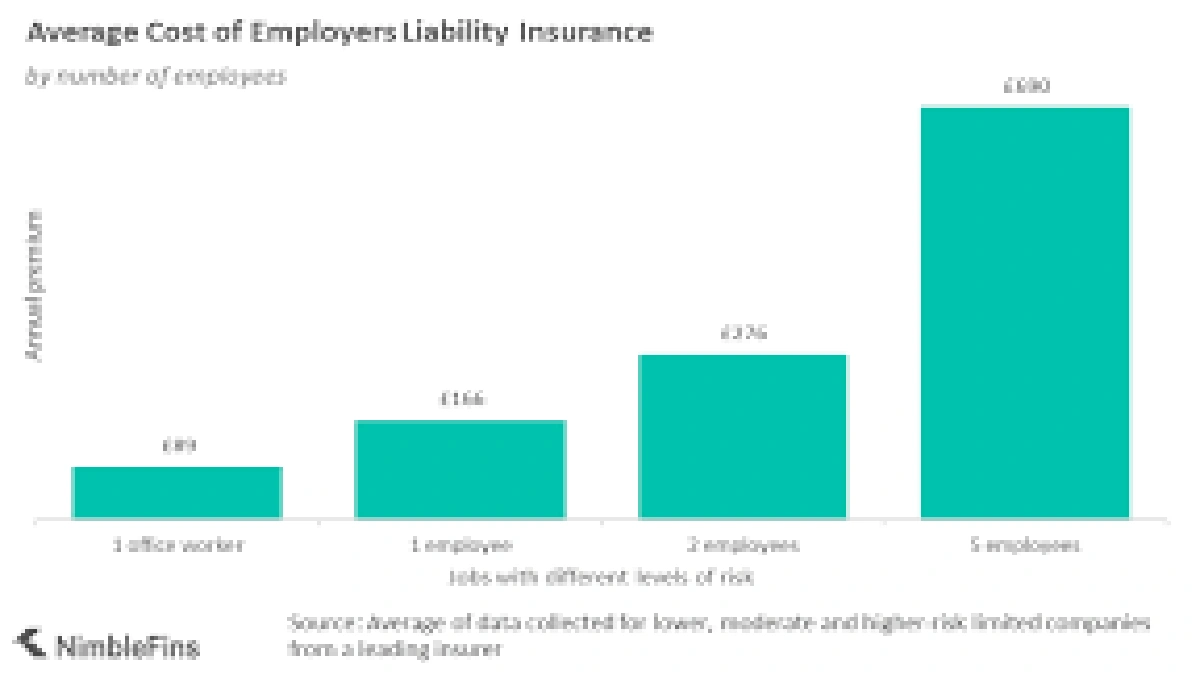

The cost of professional liability insurance isn’t fixed; it varies based on several factors: your industry, the size of your business, your annual turnover, the level of cover you need, and your claims history. A tech consultant might pay a different premium than a marketing consultant, simply because their risk profiles are different. When you’re comparing policies, look beyond just the price. Check the policy limits, exclusions, and deductibles. Does it cover past work? What about defence costs even if you’re found not liable? These details matter.

And speaking of insurance, it reminds me of a conversation I had recently about how different markets have different needs. Like how someone might search for thebest car insurance company India, a UK small business owner needs to be just as diligent when it comes to their professional cover. It’s about finding the right fit for your specific context.

The Trust Factor | Building Your Business with Confidence

Beyond the legal and financial protection, there’s another powerful benefit to having professional indemnity insurance: trust. When you can confidently tell prospective clients that you’re fully insured, it sends a strong message. It signals professionalism, responsibility, and a commitment to protecting their interests as much as your own. In competitive markets, this can be a significant differentiator, helping you secure larger contracts and build stronger, long-term client relationships. It’s not just business protection; it’s a strategic asset.

Ultimately, investing in professional liability insurance for small business UK isn’t an expense; it’s an investment in your peace of mind, your reputation, and the longevity of your venture. It allows you to focus on what you do best – serving your clients with excellence – knowing that you have a robust safety net in place should the unexpected occur. Don’t leave your hard work vulnerable to unforeseen claims. Understand the ‘why’, get the ‘how’ right, and build your business on a foundation of confidence.

Your Burning Questions About Professional Liability Insurance, Answered

Is professional indemnity the same as professional liability?

Yes, in the UK, “professional indemnity insurance” (PI) is the common term used for what is often called “professional liability insurance” in other parts of the world, like the US. They cover the same core risks: claims of negligence, errors, or omissions in professional services.

How much does professional liability insurance cost for a small business?

The cost varies significantly based on your profession, turnover, the level of cover required, and your claims history. For a small business, premiums can range from a few hundred to several thousand pounds annually. Getting a tailored quote from an insurance broker is the best way to get an accurate figure.

What isn’t covered by professional liability insurance?

PLI typically doesn’t cover claims for physical injury or property damage (that’s public liability), intentional wrongdoing, criminal acts, breach of contract unless it results from a professional error, or fines/penalties imposed by regulatory bodies.

Do I legally have to have this insurance in the UK?

While there isn’t a general legal requirement for all businesses to have professional liability insurance in the UK, many professional bodies (e.g., for solicitors, accountants, architects) mandate it for their members. Furthermore, many clients, especially larger ones, will require you to have it as a condition of contract.

Can I get professional liability insurance for my small business online?

Yes, many insurers and brokers offer online quotes and policies for professional indemnity insurance UK. However, for more complex businesses or specific risks, speaking directly with a broker can ensure you get the most appropriate and comprehensive cover.