Let’s be honest, navigating the American healthcare system can feel like trying to solve a Rubik’s Cube blindfolded. It’s complex, it’s expensive, and sometimes, it feels downright impossible to find affordable, comprehensive coverage. In this maze, short term health insurance USA often pops up as a tempting, budget-friendly alternative. But here’s the thing: while it might seem like a lifesaver for some, it’s also a potential minefield for others. I’ve seen countless people jump into these plans without fully understanding the nuances, only to face unexpected medical costs down the line. That’s why we need to talk about the deeper “why” behind these plans, moving beyond just the surface-level pros and cons. What are the hidden implications? What’s the context you’re missing?

The allure of these plans, often called limited duration health plans or temporary health insurance , is undeniable. They promise quick enrollment and significantly lower premiums compared to traditional plans. But do they deliver when you truly need them? Let’s peel back the layers and uncover the real story behind short-term health insurance in the United States.

The Allure of Short-Term Health Insurance | A Deep Dive into “Why” It’s Popular

So, why do these plans even exist, and why are they so popular? The answer, largely, boils down to cost and circumstance. Imagine you’re in a transitional period: you just started a new job but haven’t qualified for benefits yet, you’re a recent college graduate figuring out your next steps, or perhaps you’re a gig worker whose income fluctuates wildly. In these scenarios, a full-fledged Affordable Care Act (ACA) compliant plan can feel like an astronomical expense. This is where short-term plans step in, offering a seemingly perfect solution for those temporary coverage gaps .

The market for short-term health insurance exploded, particularly after changes in federal regulations allowed these plans to offer coverage for longer durations. This shift made them a more viable, albeit controversial, alternative to traditional insurance. The “why” here is simple: people need something to protect againstunexpected medical costs, and when ACA plans feel out of reach, a cheaper, quicker option becomes incredibly attractive. It’s about filling a void, even if that void isn’t filled completely or perfectly.

Unpacking the “Pros” | Where Short-Term Plans Truly Shine

Let’s not dismiss them entirely. There are indeed situations where short-term plans can be incredibly useful. Here’s where they genuinely shine:

- Affordability: This is, without a doubt, the biggest draw. Premiums for short-term plans can be significantly lower than those for ACA-compliant plans. If budget is your absolute top priority and you’re relatively healthy, this can be a major advantage.

- Quick Enrollment & Flexibility: Unlike ACA plans with their specific open enrollment periods, you can typically apply for and start a short-term plan almost immediately. They also offer flexible terms, from a few months up to a year or even longer in some states, allowing you to tailor the duration to your specific needs. This makes them ideal for temporary situations, like bridging a gap between jobs.

- Customizable Coverage (to a point): You often have more control over what your plan covers and what it doesn’t. While this sounds good, it’s a double-edged sword, as we’ll discuss. For some, being able to opt out of certain benefits they don’t anticipate needing can further reduce costs.

- Access to Private Networks: Many short-term plans utilize large, established provider networks, giving you access to a wide range of doctors and hospitals. This can be a relief if you’re used to a particular healthcare system.

I’ve seen people use these plans effectively when they’re young, healthy, and just need a safety net for a few months. For instance, a recent graduate traveling before starting a permanent job might find a cost-effective health insurance solution here, primarily to cover true medical emergencies . It’s about understanding the specific, limited scope of their utility.

The “Cons” You Can’t Afford to Ignore | Navigating the Hidden Pitfalls

Now, for the part no one wants to talk about but absolutely needs to hear. The “cons” of short-term health insurance are not just minor inconveniences; they can be financially devastating. This is the truth no one tells you upfront, the hidden catch that can turn a budget-friendly solution into a nightmare.

- Limited Coverage: This is the most critical point. Short-term plans are designed for catastrophic events, not comprehensive care. They often exclude coverage for essential health benefits mandated by the ACA, such as maternity care, mental health services, prescription drugs, and preventive care. You might find yourself paying out-of-pocket for routine check-ups or crucial medications.

- Pre-Existing Conditions: This is a massive red flag. Short-term plans are notorious for not covering pre-existing conditions. If you have any health issues that existed before you purchased the plan, even if you weren’t aware of them, treatment for those conditions will likely not be covered. This includes chronic illnesses, past injuries, or even a recent diagnosis. This single factor can lead to astronomical bills.

- Not ACA Compliant: This means they don’t meet the minimum essential coverage requirements of the Affordable Care Act. While the federal penalty for not having ACA-compliant insurance has been eliminated, these plans still don’t offer the same protections. This is a fundamental difference you must understand.

- Coverage Caps and Deductibles: Many plans come with annual or lifetime coverage limits, which can be surprisingly low. If you face a serious illness or injury, you could quickly hit these caps, leaving you responsible for the rest. High deductibles and out-of-pocket maximums are also common, meaning you pay a lot before the insurance even kicks in.

- Underwriting: Unlike ACA plans, which are guaranteed issue, short-term plans are medically underwritten. This means the insurer can deny you coverage based on your health history or charge you higher premiums. They can also rescind your policy if they discover something they deem a pre-existing condition after you’ve filed a claim. This is a stark contrast to the consumer protections offered by the ACA.

I initially thought these plans were a straightforward, albeit basic, option, but then I realized the depth of their limitations, especially regarding pre-existing conditions. It’s not just about what they don’t cover; it’s about the potential for unexpected exclusions that can truly blindside you. It reminds me of the complexities involved in finding robust coverage, whether it’s for personal health or even something likebusiness insurance online, where the fine print makes all the difference.

Who is Short-Term Health Insurance Really For? (And Who Should Steer Clear)

Given the significant pros and cons, it’s crucial to understand if you actually fit the profile for a short-term plan. Let me rephrase that for clarity: these plans are a niche solution, not a general one.

You might consider short-term health insurance if you are:

- In a temporary gap: Between jobs, waiting for employer benefits to start, or recently off your parents’ plan (and too old for it now).

- Young and exceptionally healthy: With no known pre-existing conditions and a low likelihood of needing extensive medical care.

- Seeking catastrophic coverage only: You understand and accept that this plan is primarily for severe accidents or sudden, acute illnesses, not routine care.

- On a very tight budget: And traditional ACA plans (even with subsidies) are genuinely out of reach, making some coverage better than none.

However, you should absolutely steer clear if you are:

- Managing a pre-existing condition: Even a seemingly minor one.

- Pregnant or planning to become pregnant: Maternity care is almost universally excluded.

- Need prescription drug coverage: Many plans offer minimal or no coverage.

- Seeking mental health or substance abuse services: These are often not covered.

- Eligible for ACA subsidies: If you qualify for financial assistance on the marketplace, an ACA plan will likely offer far superior coverage for a similar (or even lower) net cost.

This isn’t just about saving money; it’s about making a responsible decision for your health and financial future. Sometimes, what seems like a great deal for your wallet now can cost you exponentially more later. It’s a bit like choosing the rightbest car insurance policy– the cheapest option upfront isn’t always the best fit for your long-term needs and potential risks.

Beyond the Basics | Making an Informed Decision

So, what’s the takeaway? Short-term health insurance, with its promise of quick, affordable coverage, can be a tempting option. But it’s a decision that demands careful consideration, not just a quick glance at the premium. The one thing you absolutely must double-check is the fine print regarding exclusions, especially around pre-existing conditions and essential health benefits. Don’t just look at the monthly cost; consider the potential cost of a major medical event if your plan doesn’t cover it.

Always compare short-term plans with ACA-compliant options available onHealthcare.govor your state’s marketplace. See if you qualify for subsidies that could make a comprehensive plan surprisingly affordable. And remember, there are other health insurance alternatives like Medicaid (if eligible) or even faith-based sharing ministries, though those come with their own set of considerations.

My advice? Don’t let the immediate savings blind you to the potential long-term risks. Understand why these plans are structured the way they are, and how those structures might impact you. It’s about empowering yourself with knowledge so you can make a choice that truly serves your best interests, not just your immediate budget.

Frequently Asked Questions About Short Term Health Insurance

What exactly is short-term health insurance?

Short-term health insurance is a type of medical coverage designed to bridge temporary gaps in health coverage. These are often referred to as limited duration plans because they offer coverage for a specific, shorter period, typically from a few months up to a year, though some states allow longer.

Does short-term health insurance cover pre-existing conditions?

Generally, no. This is one of the most significant drawbacks. Short-term plans are typically not required to cover pre-existing conditions , meaning if you had a health issue before your policy started, any related medical care might not be covered, leading to high out-of-pocket costs.

Is short-term health insurance ACA compliant?

No, short-term health insurance plans are not ACA compliant plans . This means they do not offer the same essential health benefits or consumer protections mandated by the Affordable Care Act, such as coverage for maternity care, mental health, or preventive services, and they can deny coverage based on health history.

When would short-term health insurance be a good option?

Short-term health insurance might be a suitable option for individuals who are young, healthy, and experiencing a temporary gap in coverage, such as between jobs, waiting for new employer benefits to begin, or after graduating college. It’s primarily for unexpected medical emergencies rather than comprehensive care.

Can I renew my short-term health insurance policy?

While some short-term policies can be renewed, or you can purchase a new policy after your current one expires, it’s important to be aware that each renewal or new policy typically treats any conditions developed during the previous term as new pre-existing conditions, which would then not be covered. This can create significant coverage gaps .

Are there alternatives to short-term health insurance for temporary coverage?

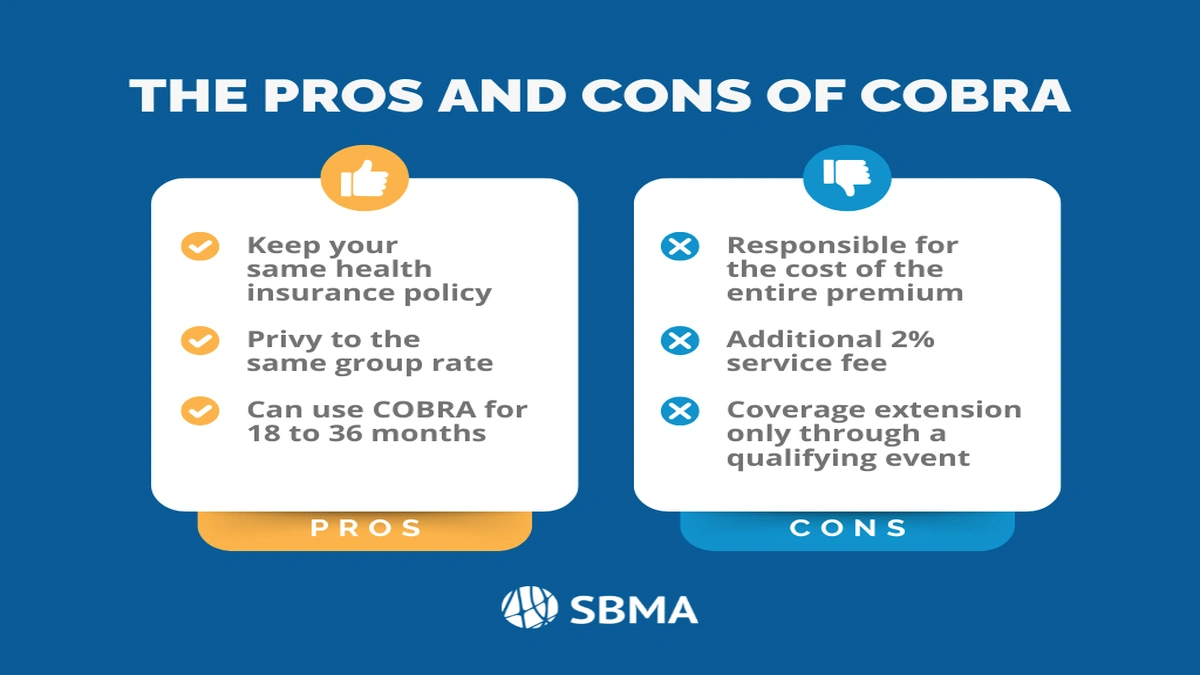

Yes, there are several health insurance alternatives . You might qualify for a Special Enrollment Period for an ACA plan if you have a qualifying life event (like losing job-based coverage). Medicaid, COBRA, or even health care sharing ministries are other options, each with its own eligibility requirements and coverage specifics.