Alright, let’s talk turkey about something that often feels like a necessary evil for any ambitious LLC owner in the USA: general liability insurance for LLC USA cost . Here’s the thing – it’s not just another line item on your budget. It’s a shield, a safety net, and honestly, a testament to how seriously you take your business. And what fascinates me is how many entrepreneurs look at the price tag and miss the deeper story behind it.

We’re not just going to scratch the surface here. We’re going to dig into the ‘why.’ Why does one LLC pay significantly more or less than another? Why is understanding the nuances of your policy more crucial than simply finding the cheapest option? Because when you truly grasp what drives these costs, you’re not just buying insurance; you’re investing in peace of mind and the long-term resilience of your business. Let me rephrase that for clarity: you’re buying the ability to sleep at night, knowing a slip-and-fall or an unexpected lawsuit won’t derail your dream. That, my friend, is invaluable.

Beyond the Sticker Price | What Really Drives Your General Liability Premium?

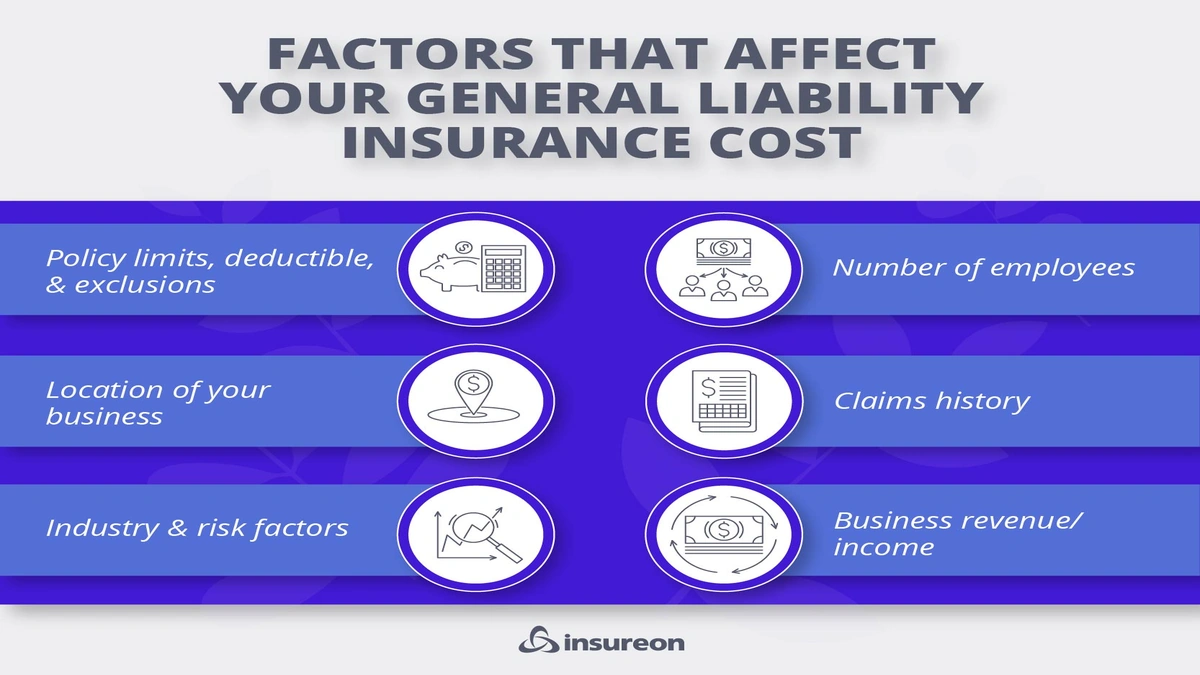

When you first start looking for small business insurance rates , it’s easy to get overwhelmed. You see numbers flying around, and it can feel a bit like throwing darts in the dark. But the cost of your commercial general liability policy isn’t some arbitrary figure dreamt up by an actuary with too much coffee. Oh no. It’s a calculated risk assessment, and several key factors play a starring role.

First off, your industry . This is huge. A graphic designer working from a home office, for instance, faces vastly different risks than a roofing contractor. The potential for bodily injury or property damage claims varies wildly. So, if you’re in a high-risk industry – think construction, food service, or anything involving heavy machinery or public interaction – expect your premiums to reflect that elevated risk. It’s just common sense, right?

Then there’s your location . Operating in a bustling city center with high foot traffic might mean more exposure to potential incidents than running a remote consulting firm in a quiet rural area. State regulations, local claim trends, and even the cost of living in your area can subtly, or not so subtly, influence the `factors affecting insurance cost`.

Your business size and revenue also matter. A solo entrepreneur typically has a lower risk profile than a company with 50 employees and millions in annual revenue. More employees mean more opportunities for accidents, and higher revenue might attract higher liability claims. And let’s not forget your claims history . If your LLC has a history of past claims, insurers will naturally view you as a higher risk, which, you guessed it, translates to higher premiums. It’s like your driving record, but for your business.

The “Must-Haves” vs. “Nice-to-Haves” | Understanding Your Coverage

So, you know what a commercial general liability policy broadly covers: bodily injury, property damage, advertising injury, and personal injury. But what does that really mean for your LLC? It means if a client slips on a wet floor in your office, or if your employee accidentally damages a client’s property, your general liability steps in. It also covers things like libel or slander claims that might arise from your advertising.

Now, when it comes to the `minimum coverage for LLC` in the USA, here’s a crucial point: unlike auto insurance, general liability isn’t universally mandated by federal or state law for all businesses. However, many clients, landlords, or licensing boards will require you to carry it. And frankly, even if they didn’t, it’s a non-negotiable for smart business owners. The question isn’t whether you need it, but how much. This is where `coverage limits` come into play.

Most policies come with per-occurrence limits (the maximum an insurer will pay for a single incident) and aggregate limits (the maximum they’ll pay over the policy period). Choosing these limits is a delicate balance. Too low, and you could be exposed if a major lawsuit hits. Too high, and you might be paying for more than you realistically need, especially if you’re a small operation. A common mistake I see people make is defaulting to the lowest possible limits without truly assessing their unique risk exposure. Don’t be that person. Think about the worst-case scenario for your specific business and insure accordingly.

Getting the Best Deal | Navigating Business Liability Insurance Quotes

Finding the right business liability insurance quotes isn’t about just clicking the first link on Google. It’s about diligence and understanding. The `average cost of general liability` for an LLC can range anywhere from a few hundred dollars to several thousand annually, but averages can be misleading. Your specific situation will dictate your true cost.

My advice? Don’t just get one quote. Get several. And don’t just look at the price. Compare the coverage limits, deductibles, exclusions, and endorsements. What one policy covers, another might not, even if the premium looks similar. This is where an independent insurance agent becomes your secret weapon. Unlike captive agents who work for a single company, independent agents can shop around with multiple carriers to find you the best blend of coverage and cost. They understand the intricacies of different policies and can often spot gaps or overlaps you might miss.

Also, make sure your business description is accurate when getting quotes. Misrepresenting your operations, even unintentionally, could lead to claims being denied down the line. Honesty is always the best policy, pun intended. Consider bundling policies, too. Often, combining your general liability with, say, professional liability orcommercial liability insurance for small businesscan result in significant discounts.

Protecting More Than Just Your Business | The Value of Peace of Mind

At the end of the day, general liability insurance for your LLC isn’t just a legal or contractual obligation; it’s a strategic investment in your future. It’s about building a resilient business that can weather unexpected storms. Think of it this way: you invest in good equipment, marketing, and talent. Why wouldn’t you invest in protecting all of that from unforeseen risks?

Let’s be honest, the legal landscape in the USA can be complex and litigious. A single lawsuit, even if frivolous, can drain your resources, time, and emotional energy. Having the right general liability coverage means you have a partner – your insurance company – to help navigate those choppy waters. They’ll cover legal defense costs, settlements, or judgments, up to your policy limits. That’s a huge burden lifted from your shoulders.

For those looking for an extra layer of protection, especially as their business grows, exploring `umbrella insurance for LLC` might be a smart move. It kicks in when your primary liability limits are exhausted, offering an additional safety net. It’s like a backup for your backup, and sometimes, that extra peace of mind is worth every penny. Just like consideringbest home insurance policy Indiafor your personal assets, business insurance is about safeguarding your professional life.

So, while the initial thought of `general liability insurance for LLC USA cost` might seem like an expense, I urge you to reframe it. It’s an essential tool for business longevity, a safeguard for your assets, and ultimately, an investment in your ability to focus on what you do best: growing your LLC.

Frequently Asked Questions About LLC General Liability Insurance

How much does general liability insurance for an LLC cost on average?

The average cost can vary widely, from around $300 to $1,500 per year for a basic policy. However, this is heavily influenced by factors like your industry, location, business size, and chosen coverage limits. High-risk businesses will typically pay more.

What factors significantly impact general liability insurance premiums for LLCs?

Key factors include your industry’s inherent risk level, your business’s physical location, annual revenue, number of employees, past claims history, and the specific coverage limits and deductibles you select for your policy.

Is general liability insurance mandatory for LLCs in the USA?

No, general liability insurance is not universally mandated by federal or state law for all LLCs in the USA. However, it’s often required by landlords, clients, or for certain professional licenses. Even when not legally required, it’s highly recommended for risk protection.

Can I get a cheaper policy by reducing my coverage limits?

Yes, reducing your coverage limits will typically lower your premium. However, this also means you’ll have less financial protection in the event of a claim, potentially leaving your LLC vulnerable to significant out-of-pocket expenses if a lawsuit exceeds your policy limits.

What’s the difference between general liability and professional liability?

General liability insurance covers claims of bodily injury, property damage, and advertising injury. Professional liability insurance (also known as E&O) covers claims of negligence, errors, or omissions in your professional services. Many businesses, especially service-based LLCs, need both.