Alright, let’s be honest. If you’re a freelancer in the USA, the phrase “health insurance” probably conjures up a mix of dread, confusion, and maybe a little bit of panic. It’s not like the good old days (or, well, the traditional employee days) when your employer just handled it. Now, it’s on you. And the biggest question looming over every self-employed individual’s head? The health insurance for freelancers USA cost.

I’ve seen countless freelancers, myself included, navigate this incredibly murky water. It feels like a secret club sometimes, doesn’t it? But here’s the thing: it doesn’t have to be. My goal today is to walk you through exactly how to find, understand, and yes, even potentially lower, your freelance health insurance costs. Consider me your knowledgeable friend, sitting across from you with a cup of coffee, ready to demystify the whole process.

Decoding the Freelance Health Insurance Maze | Why It’s Different

First off, let’s acknowledge why this is such a unique challenge. When you’re self-employed, you’re essentially your own HR department. This means no company benefits package, no employer contributions chipping away at your premiums. You’re buying your coverage on the individual market, which operates under a different set of rules and, often, a different price tag.

The implications? Well, it means you need to be proactive. You can’t just assume coverage will magically appear. And frankly, going without health insurance in the U.S. is a gamble I wouldn’t wish on my worst enemy. One unexpected medical emergency could wipe out your savings, your business, and your peace of mind. So, understanding your options for self-employed health insurance options isn’t just a good idea; it’s absolutely crucial for your financial and personal well-being.

Your Options, Demystified | Where to Look for Coverage

Okay, deep breath. There are legitimate avenues for getting coverage. It’s not a lost cause. The key is knowing where to look and what each option entails.

1. The ACA Marketplace (Healthcare.gov)

This is often the first and best stop for many freelancers. The Affordable Care Act (ACA) created state and federal marketplaces where individuals can compare and purchase health insurance plans. The huge advantage here? Subsidies. Depending on your income, you might qualify for tax credits that significantly reduce your monthly premiums. These aren’t just for low-income individuals; many middle-income freelancers find they qualify.

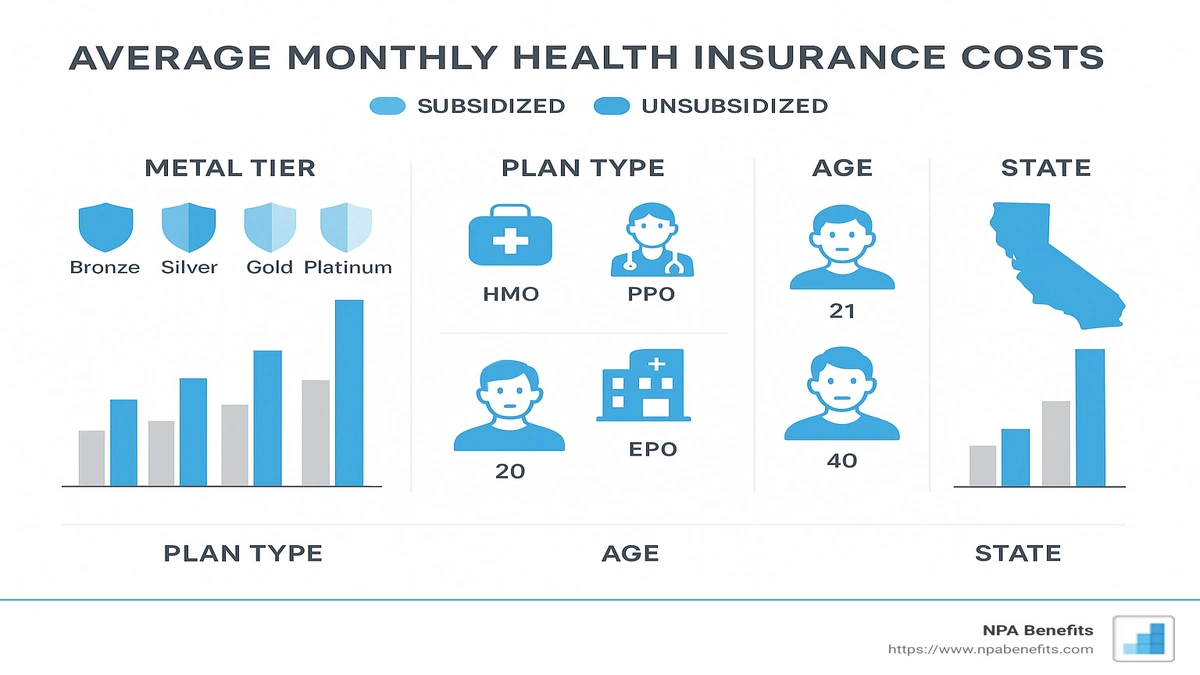

Plans are categorized into metal tiers (Bronze, Silver, Gold, Platinum) indicating the split between what you pay and what the plan pays. For instance, Silver plans often come with additional cost-sharing reductions if you qualify, making them incredibly attractive. Open enrollment typically happens in the fall, but certain life events (like moving, getting married, or losing other coverage) can trigger a special enrollment period.

2. Short-Term Health Insurance

This is where things get a bit trickier, and honestly, a bit riskier. Short-term health insurance plans are exactly what they sound like: temporary coverage, usually for a few months to a year. They’re cheaper, yes, but they don’t have to comply with ACA rules. This means they can deny coverage for pre-existing conditions, don’t cover essential health benefits (like maternity care or mental health), and have caps on how much they’ll pay out. I generally advise treating these as a last resort or for truly temporary gaps in coverage, not as a long-term solution. They’re a band-aid, not a cure.

3. Health Savings Accounts (HSAs)

While not an insurance plan itself, an HSA is a powerful tool that pairs with a high-deductible health plan (HDHP). If you choose an HDHP through the ACA marketplace or elsewhere, you can contribute pre-tax money to an HSA, let it grow tax-free, and withdraw it tax-free for qualified medical expenses. It’s a triple tax advantage! For freelancers, this is a fantastic way to save for future medical costs and lower your taxable income. I always tell people, if you’re healthy and can manage a higher deductible, an HSA is a game-changer for managing gig economy health benefits.

4. Professional Organizations & Freelance Unions

Some professional associations or unions offer group health insurance plans to their members. These can sometimes provide better rates or more comprehensive coverage than individual plans, but it’s not a universal solution. Always compare their offerings carefully with what you can find on the ACA marketplace.

5. Spousal/Partner Plans

If you’re married or have a domestic partner, checking if you can be added to their employer-sponsored plan is often the most cost-effective solution. The employer usually covers a significant portion of the premium, making it much more affordable than individual plans.

The Big Question | What Does Health Insurance for Freelancers USA Cost, Really?

Ah, the million-dollar question. The truth is, there’s no single answer. The health insurance for freelancers USA cost varies wildly based on several factors, and it’s essential to understand them:

- Age: Generally, the older you are, the higher your premiums.

- Location: Costs differ significantly by state, and even by county within a state, due to varying healthcare costs and competition among insurers.

- Plan Type: Bronze plans are cheapest but have the highest deductibles. Platinum plans are most expensive but cover the most.

- Deductible & Out-of-Pocket Max: A higher deductible usually means a lower monthly premium.

- Subsidies: This is huge. Income-based tax credits can drastically reduce your out-of-pocket premium. Many people are surprised to find they qualify.

Without subsidies, a typical individual plan could range from $300 to $700+ per month, depending on the factors above. But with subsidies, that number can drop dramatically, sometimes to less than $100 or even free for those with very low incomes. It’s why I always tell people to check the marketplace first. You can get a good estimate of your potential costs and subsidies atHealthcare.gov.

When thinking about your overall financial protection, don’t forget other crucial coverages. For instance, understandinghow much life insurance coverageyou might need is another vital piece of the personal finance puzzle, especially when you have dependents or business liabilities.

Smart Strategies to Lower Your Freelance Health Insurance Costs

Now that we know the lay of the land, let’s talk strategy. How can you make affordable health insurance for freelancers a reality?

- Maximize Those Subsidies: Seriously, don’t skip this step. Even if you think your income is too high, check. Your Adjusted Gross Income (AGI) is what counts, and business deductions can often lower that number.

- Choose the Right Metal Tier: If you’re generally healthy and can cover a higher deductible, a Bronze or Silver plan (especially with cost-sharing reductions) might be your best bet for managing freelance health insurance costs. If you have chronic conditions and expect to use your insurance often, a Gold or Platinum plan might save you money in the long run.

- Utilize HSAs: As mentioned, these are fantastic. The tax benefits alone make them worth considering if you’re on an HDHP. It’s a smart way to build a medical emergency fund.

- Shop Around Annually: Plans and prices change every year. What was the best deal last year might not be this year. Always re-evaluate your options during open enrollment.

- Consider Tax Deductions: If you’re self-employed and not eligible for employer-sponsored health coverage (either your own or your spouse’s), you can often deduct the premiums you pay for health insurance from your gross income. This is a huge, often overlooked, benefit!

Navigating Open Enrollment and Special Situations

The annual open enrollment period (usually November 1st to December 15th for coverage starting January 1st) is your primary window to enroll in or change an ACA marketplace plan. Mark it on your calendar, set reminders, do whatever you need to do to not miss it.

But what if you miss open enrollment or have a change mid-year? That’s where special enrollment periods (SEPs) come in. Life events such as:

- Getting married or divorced

- Having a baby or adopting a child

- Moving to a new area

- Losing other health coverage (e.g., leaving a W2 job)

- A significant change in income

…can all trigger an SEP, allowing you to enroll outside the standard window. Always checkHealthcare.gov’s SEP guidelinesif you experience one of these events. And remember, just as you’d research thebest health insurance for familyif you had dependents, the same diligence applies to your individual plan.

Ultimately, finding the right health insurance for freelancers USA cost isn’t about finding the cheapest option; it’s about finding the best value that fits your needs and budget. It requires a bit of research, a dash of understanding, and a willingness to explore your options. But once you’ve got it sorted, that feeling of security? Priceless. So, take control, understand your choices, and protect your most valuable asset: yourself.

Frequently Asked Questions About Freelance Health Insurance

How much is health insurance for freelancers USA cost on average?

On average, without subsidies, individual health insurance premiums can range from $300 to $700+ per month. However, many freelancers qualify for significant tax credits through the ACA marketplace, which can drastically reduce these costs, sometimes to under $100 or even free, depending on income and location.

Can I get subsidies for self-employed health insurance?

Yes, absolutely! Many self-employed individuals qualify for premium tax credits (subsidies) through the Affordable Care Act (ACA) marketplace. Eligibility is based on your household income relative to the federal poverty level. It’s crucial to apply through Healthcare.gov to see if you qualify.

What are the best health insurance options for freelancers?

The best options generally include plans from the ACA marketplace (which offer subsidies), potentially group plans through professional organizations, or joining a spouse’s employer plan. Short-term health insurance is usually not recommended as a primary, long-term solution due to its limited coverage.

Is short-term health insurance a good idea for freelancers?

Generally, no, not for long-term primary coverage. While cheaper, short-term plans don’t cover essential health benefits, can deny coverage for pre-existing conditions, and have benefit caps. They are best used only for very temporary gaps in coverage, like a few months between jobs, rather than as a substitute for comprehensive insurance.

How do HSAs work with freelance health plans?

Health Savings Accounts (HSAs) are tax-advantaged savings accounts that pair with a high-deductible health plan (HDHP). Freelancers with an HDHP can contribute pre-tax money to an HSA, let it grow tax-free, and withdraw it tax-free for qualified medical expenses. It’s a powerful tool for managing healthcare costs and saving for the future.

Where can I find affordable health insurance for freelancers?

The primary place to find truly affordable health insurance for freelancers is the ACA marketplace at Healthcare.gov. This is where you can compare plans and apply for income-based subsidies that can significantly lower your monthly premiums. You can also explore professional organizations or consider joining a spouse’s plan if applicable.