Let’s be honest, thinking about life insurance isn’t exactly a thrilling Saturday night activity. It often feels like a necessary evil, a complex maze of jargon and numbers, all while carrying the underlying weight of ‘what if?’. And then there’s the cost – that nagging concern that protecting your loved ones might just be another financial burden you can’t quite squeeze into the budget. But here’s the thing: securing low cost life insurance UK monthly plans doesn’t have to be a headache or a drain. In fact, with the right approach, it’s entirely achievable.

I’ve seen countless people navigate this landscape, often making common mistakes that lead to overpaying or getting a policy that doesn’t quite fit. My goal today is to cut through the noise, offering you a practical, step-by-step guide to finding anaffordable life insurance UKpolicy that truly protects without breaking the bank. Think of me as your personal guide, helping you demystify the process so you can get back to what matters: living your life with peace of mind.

Why “Low Cost” Doesn’t Mean “Low Value” | Understanding the UK Market

When you hear “low cost,” it’s easy to picture something flimsy or inadequate, right? But in the world of UK life insurance, a budget-friendly policy can still offer robust protection. The key isn’t to find the cheapest possible option, but the best value for your specific circumstances. What really influences the cost? Well, it’s a blend of factors unique to you and the policy you choose.

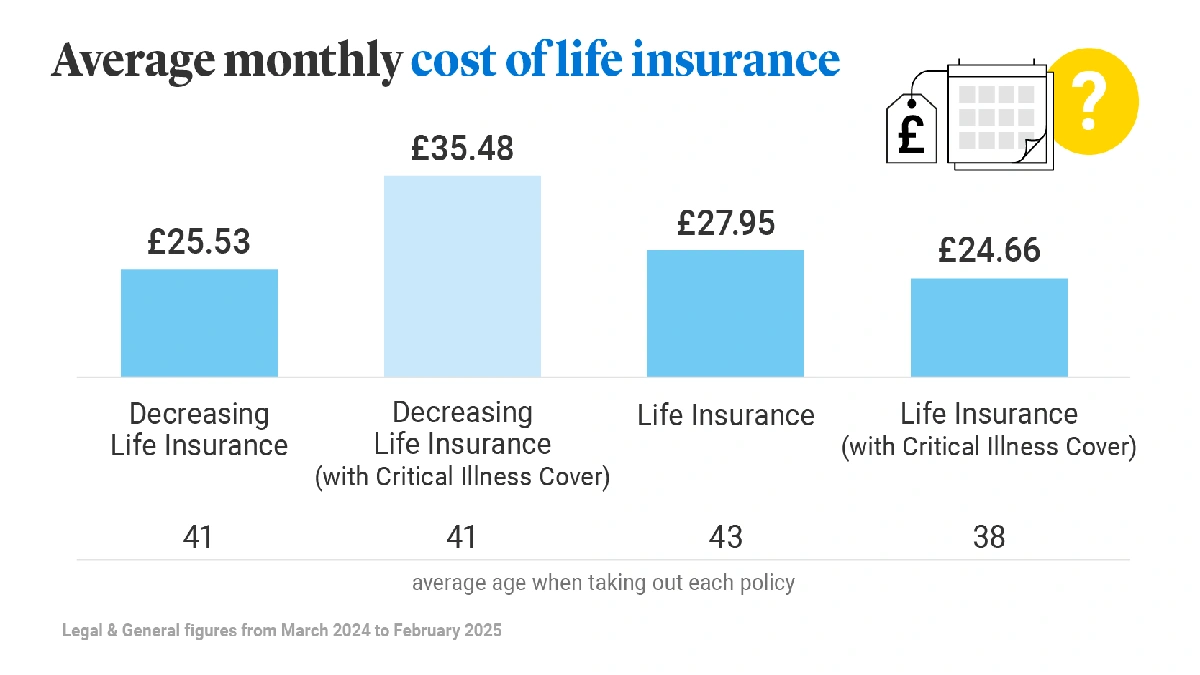

For instance, the type of policy plays a huge role. Are you looking forterm life insurance plans, which covers you for a set period, say 20 or 30 years? Or perhaps a whole life policy that covers you for your entire life? Generally speaking, term life insurance tends to be more budget-friendly because it has an end date. This is where many people start their journey for cheap monthly life insurance . But even within term policies, there are variations like ‘level term’ (payout stays the same) and ‘decreasing term’ (payout reduces over time, often used for mortgages). Understanding these nuances is the first step to making an informed decision, not just grabbing the first quote you see.

The Step-by-Step Guide to Finding Your Ideal Monthly Plan

Alright, let’s get down to brass tacks. How do you actually find these elusive low cost life insurance UK monthly plans ? It’s not magic; it’s methodology. Here’s how I’d approach it:

Step 1 | Assess Your Needs (Be Brutally Honest)

Before you even think about gettinginsurance options, sit down and consider what you’re trying to protect. Who depends on your income? Do you have a mortgage, loans, or other debts? What about future expenses like children’s university fees or funeral costs? A common mistake I see people make is either over-insuring (paying for more cover than they genuinely need) or under-insuring (leaving their family vulnerable). Be realistic about the lump sum your dependents would require to maintain their lifestyle and cover essential costs if you were no longer around. This sum assured will directly impact your premiums.

Step 2 | Compare, Compare, Compare!

This might sound obvious, but it’s astonishing how many people take the first quote they get. The UK market for life insurance is incredibly competitive, with a wide range of providers. This is where you can really find those life insurance quotes UK that offer value. Don’t just go to one insurer; use comparison websites, speak to independent financial advisors, and even check direct with providers. Each platform might have different deals or access to different panels of insurers. It’s a bit like shopping for flights – you wouldn’t just check one airline, would you?

Step 3 | Understand Policy Terms (The Devil’s in the Detail)

Once you have a few promising quotes, dig into the details. What’s the policy length? What are the exclusions? Does it offer any flexibility if your circumstances change? For instance, some policies allow you to increase your cover without further medical underwriting after significant life events like marriage or childbirth. Knowing these small print details can save you a lot of hassle and money down the line. It’s not just about the monthly premium; it’s about the comprehensive package.

Decoding the Price Tag | Factors That Drive Your Premiums Down (or Up!)

Ever wondered why your friend’s premium is so different from yours, even if you’re roughly the same age? It’s all about risk assessment. Insurers are essentially betting on how long you’ll live, and various factors influence those odds. Understanding these can help you potentially lower your costs or at least comprehend why your premium is what it is.

- Age: This is probably the biggest one. The younger you are when you take out a policy, the cheaper it generally is. It’s simple maths for insurers – less time for something to go wrong.

- Health: Your medical history is scrutinised. Conditions like diabetes, high blood pressure, or a history of heart disease will likely increase your premiums. Being a non-smoker is a massive advantage here, as smoking significantly elevates your risk profile and, consequently, your understanding life insurance premiums.

- Lifestyle: Your occupation can play a role, especially if it’s considered high-risk (think construction workers vs. office workers). Hobbies, too, can influence costs if they involve extreme sports or dangerous activities.

- Policy Duration & Sum Assured: As mentioned, shorter terms are cheaper. Also, the less money you want your family to receive (the sum assured), the lower your monthly payment will be. It’s a balance between adequate protection and affordability.

While you can’t turn back time to be younger, you can make lifestyle changes. Quitting smoking, managing health conditions, and maintaining a healthy weight can all positively impact your future premiums. It’s a long game, but worth it for both your health and your wallet.

Beyond the Basics | Add-ons and What to Watch Out For

Many low cost life insurance UK monthly plans come with options to add extra layers of protection. While these can be incredibly valuable, they also add to the cost, so it’s crucial to evaluate if you truly need them. The most common add-ons include:

- Critical Illness Cover: This pays out a lump sum if you’re diagnosed with a specified serious illness (like cancer, heart attack, or stroke) during the policy term. For many, this critical illness cover UK is as important as life cover, as it provides financial support during a time when you might be unable to work.

- Income Protection: This pays you a regular income if you can’t work due to illness or injury. It’s different from critical illness cover, which is a lump sum, and life insurance, which pays out upon death.

My advice? Don’t just tick every box. Consider your existing sick pay benefits from work, your savings, and your family’s needs. Sometimes, a simpler, more focused policy on just life cover is the most effective way to secure cheap monthly life insurance without overspending. Always ask your potential provider about the ins and outs of these additions, ensuring you’re not paying for something you don’t truly need or already have covered elsewhere.

Your Burning Questions About Low-Cost Life Insurance UK Monthly Plans Answered

Is low cost life insurance UK monthly plans really reliable?

Absolutely. The reliability of a policy isn’t determined by its cost, but by the insurer’s financial stability and regulatory compliance. All UK life insurance providers are regulated by the Financial Conduct Authority (FCA) and covered by the Financial Services Compensation Scheme (FSCS). This means that even if an insurer were to go bust, your policy (up to a certain limit) would still be protected. The key is choosing a reputable provider, and there are many excellentbest life insurance providers UKoffering great value.

Can I get cover if I have pre-existing conditions?

Yes, often you can. It might be more expensive, and you may need to provide more medical information or undergo a medical exam. Insurers will assess the condition’s severity, how well it’s managed, and its potential impact on your life expectancy. It’s crucial to be completely honest about your medical history, as failing to do so could invalidate your policy.

What’s the difference between term and whole life insurance?

Term life insurance UK covers you for a specific period (e.g., 10, 20, 30 years) and pays out only if you die within that term. It’s generally more affordable. Whole life insurance covers you for your entire life and guarantees a payout whenever you die, making it typically more expensive.

How often should I review my policy?

I recommend reviewing your life insurance policy every few years, or whenever you experience a significant life event. This includes getting married, having children, buying a house, taking on new debt, or even seeing a significant change in your income. Your needs evolve, and your policy should, too.

What if I miss a payment on my cheap monthly life insurance?

Most insurers offer a grace period (typically 30 days) if you miss a payment. During this time, your cover usually remains active. However, if you don’t make the payment within the grace period, your policy could lapse, meaning you’d no longer be covered. It’s always best to contact your insurer immediately if you foresee payment difficulties.

Are there any hidden fees to watch out for?

Generally, with direct-to-consumer or broker-arranged policies, the quoted monthly premium is what you pay. However, some policies, especially those with an investment element (less common for basic term life), might have fees. Always read the Key Information Document (KID) or policy summary carefully to understand all charges. Transparency is key.

So, there you have it. Finding low cost life insurance UK monthly plans isn’t about cutting corners; it’s about being informed, strategic, and proactive. It’s about understanding your needs, comparing your options, and choosing a policy that offers genuine protection for the people who matter most, without putting an undue strain on your finances. With a little bit of effort and the right guidance, you can absolutely secure that peace of mind. Go on, take that first step!