Let’s be honest, talking about life insurance payout options isn’t exactly a thrilling topic for most people. It conjures images of complex paperwork, jargon, and a future we’d rather not dwell on. But here’s the thing: understanding how your life insurance policy pays out – especially in the USA – is one of the most critical financial decisions you or your loved ones will ever face. It’s not just about getting money; it’s about how that money arrives and how it can best serve your beneficiaries when they need it most. And trust me, getting this wrong can have significant, long-lasting consequences.

Think of it this way: you’ve invested in a safety net, a promise to protect your family. But what if that net has holes, or if the way it’s deployed isn’t what you expected? That’s why I want to guide you through the maze of life insurance payout options explained USA , making it clear, actionable, and frankly, a bit less intimidating. We’ll explore the common choices, the nuances, and even the often-overlooked tax implications, so you can make informed decisions. Because when it comes to securing your legacy, knowledge truly is power.

Understanding the Big Picture | Why Payout Choices Matter

When a policyholder passes away, the primary goal of life insurance is to provide a financial cushion for their beneficiaries. This payment, often called the death benefit , is designed to replace lost income, cover final expenses, pay off debts, or fund future needs like education. But the journey from policy to payout isn’t always a straight line. The choices made during policy setup, or even by the beneficiary later on, can dramatically alter the financial landscape for those left behind.

What fascinates me is how many people meticulously choose their coverage amount but then gloss over the actual life insurance settlement options . It’s like buying a fantastic car but forgetting to decide if you want to drive it or have it towed. The method ofdeath benefit distributioncan impact everything from your family’s immediate liquidity to their long-term financial stability and even their tax burden. A common mistake I see people make is assuming a single, straightforward payout is the only way. While it’s the most common, it’s far from the only, or even always the best, option. It’s about tailoring the payout to the unique needs and financial literacy of your beneficiary .

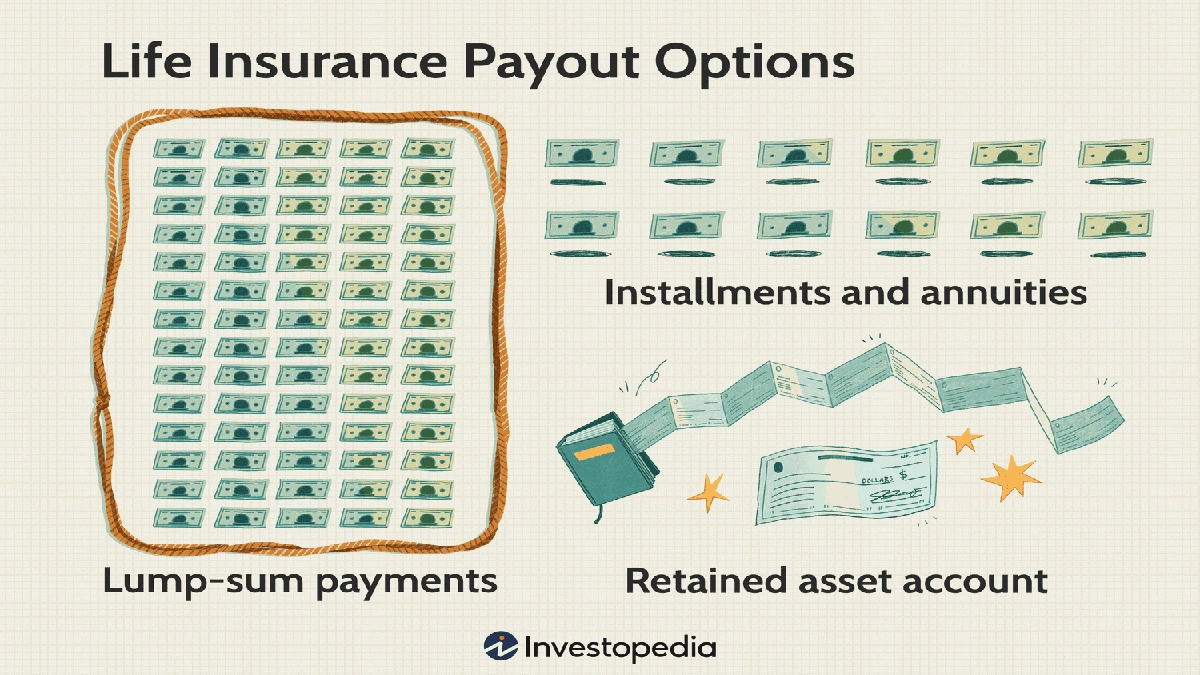

Your Core Choices | The Main Life Insurance Payout Options

Alright, let’s dive into the practical side of things – the actual mechanisms by which that crucial death benefit can be delivered. Understanding these is key to making the right choice for your family’s future.

Lump Sum Payout

This is probably what most people imagine when they think about a life insurance payout. A lump sum means the entire death benefit is paid out to the beneficiary in one single payment. It’s straightforward, immediate (once approved, of course), and gives the beneficiary complete control over the funds. For some, this is ideal. It allows them to pay off a mortgage, cover immediate expenses, or invest the money as they see fit. However, for a beneficiary who isn’t financially savvy, or who is grieving and vulnerable, a large sum of money can be overwhelming. It could lead to poor investment decisions or quick depletion of funds, which is the last thing you want after a loss. It’s a powerful tool, but like any powerful tool, it requires careful handling.

Annuity Settlement Option

Instead of a single payment, an annuity settlement option turns the death benefit into a series of regular payments over a set period or for the beneficiary’s lifetime. This can be a fantastic choice for beneficiaries who might struggle with managing a large sum of money, or for those who need a guaranteed, steady income stream. There are various types:

- Fixed Period Option: Payments are made over a specific number of years (e.g., 10, 20 years).

- Life Income Option: Payments are made for the remainder of the beneficiary’s life, regardless of how long they live. This provides incredible peace of mind but typically offers no remaining value upon their death.

Choosing an annuity can provide financial stability, helping your loved ones budget and avoid making rash decisions during a difficult time. It’s a way of ensuring the funds last, providing a steady hand when you’re no longer there to guide them.

Interest Income Option & Retained Asset Accounts

This option is a bit more nuanced. With an interest income option , the insurance company holds the death benefit and pays the beneficiary regular interest on the principal. The principal amount remains with the insurer until the beneficiary decides to withdraw it, either partially or in full. A common form of this is a retained asset account . The insurer often sets up a special checking account for the beneficiary, from which they can write checks or withdraw funds. The balance earns interest, often at a competitive rate.

This offers flexibility: immediate access to interest income while preserving the principal. It can be a good bridge solution, allowing beneficiaries time to grieve and plan without immediate pressure to manage a large sum. However, the interest rates offered might not always keep pace with market returns, and there can be fees associated with these accounts. It’s important to understand the terms carefully.

Other Specialized Options

Beyond these core choices, some policies might offer more tailored installment plans or other unique beneficiary options life insurance . These could include specific installment payments for certain events (like college tuition) or a combination of the above. Always review your policy documents or speak with your insurer to understand the full range of life insurance payout USA choices available to you.

Navigating the Tax Maze | What to Know About Your Payout

Here’s where things can get a little tricky, but it’s absolutely vital to understand: the tax implications life insurance payout . Generally speaking, the death benefit itself, when paid to a named beneficiary, is typically received income tax-free in the USA. This is a huge advantage of life insurance and a significant reason why it’s such a powerful financial planning tool.

However, there are exceptions and nuances. For instance, if the payout is structured as an interest income option or an annuity settlement option , the interest earned on the retained principal or the investment gains within the annuity payments can be taxable. If the policy was transferred for value (sold to someone else for a fee), or if it’s part of a business arrangement, the tax situation can become more complex. Also, while generally income tax-free, the death benefit might be subject to estate taxes if the policyholder’s estate exceeds certain federal or state thresholds. This is why consulting with a qualified financial advisor or tax professional is always a smart move, especially for larger policies or complex estate plans. Don’t leave this to chance!

Making the Right Call | How to Choose Your Payout Option

So, with all these options, how do you make the best choice for your particular situation? It boils down to understanding your beneficiaries and their needs. I initially thought this was straightforward, but then I realized the depth of the decision. Here’s how to think aboutmaking the right call:

- Assess Your Beneficiaries’ Financial Savvy: Are they experienced investors, or would a large sum overwhelm them? For someone less experienced, an annuity or interest income option might be safer.

- Consider Their Immediate and Long-Term Needs: Do they need a large sum immediately to pay off a mortgage or cover significant debts? Or is a steady income stream more crucial for ongoing living expenses?

- Factor in Investment Goals: If your beneficiary is a skilled investor, a lump sum might allow them to achieve higher returns than an insurer’s interest rate. If not, the guaranteed payments of an annuity might be preferable.

- Review Your Policy and Discuss with an Advisor: Don’t guess. Talk to your insurance agent or a financial planner. They can help you understand the specific settlement options available with your policy and how they align with your family’s financial plan. It’s similar to how you’d compare different financial products – thorough research and expert advice are invaluable.

- Periodically Re-evaluate: Life changes. What was right for your family five years ago might not be right today. Review your beneficiary options and payout instructions every few years, especially after major life events like marriage, divorce, or the birth of a child.

Remember, the goal of how life insurance works is to provide peace of mind and financial security. By thoughtfully considering these payout options, you’re not just buying a policy; you’re crafting a safety net that’s perfectly suited to catch your loved ones, no matter what life throws their way.

FAQs | Quick Answers to Your Payout Questions

What is the most common life insurance payout option in the USA?

The most common option is typically a single lump sum payout, where the entire death benefit is paid to the beneficiary at once.

Can a beneficiary change the payout option after the policyholder dies?

Yes, in many cases, if the policyholder didn’t specify a particular payout option, the beneficiary can choose from the available life insurance payout options offered by the insurer at the time of claim.

Are life insurance payouts taxable in the USA?

Generally, the death benefit from a life insurance policy is received income tax-free by the beneficiary. However, any interest earned on the payout (e.g., from an interest income option or retained asset account) may be taxable.

How long does it typically take to receive a life insurance payout?

While it varies, most claims are processed within 30-60 days after all required documentation is submitted. Complex cases or investigations can take longer.

What if the beneficiary is a minor?

If a minor is named as a beneficiary, a guardian or trustee must typically be appointed to manage the funds on their behalf until they reach legal adulthood. This is why setting up a trust can be a valuable strategy.

What’s the difference between a lump sum and an annuity for a beneficiary?

A lump sum provides the entire death benefit at once, giving the beneficiary immediate control. An annuity settlement option provides regular, periodic payments over a set time or for life, offering a steady income stream but less immediate control over the principal.

Ultimately, the power of life insurance isn’t just in its existence, but in its thoughtful design. By truly understanding the various life insurance payout options explained USA , you empower your beneficiaries to navigate their financial future with confidence, even in your absence. Don’t just buy a policy; design its impact. That’s the real legacy you leave behind.